Agricultural Lubricant Market (2022 - 2032)

AGRICULTURAL LUBRICANT MARKET SIZE & SHARE BY CATAGORY (SYNTHETIC OIL, MINERAL OIL, BIO-BASED LUBES), BY PRODUCT TYPE (ENGINE OIL, UNIVERSAL TRACTOR TRANSMISSION OIL, GREASES, COOLANT & OTHERS), BY SALES CHANNEL (OEM & OE SERVICE NETWORK AND AFTERMARKET), BY PRODUCT RANGE (BASE, MID-RANGE, PREMIUM), BRANDING (LUBRICANT COMPANY OWNED BRAND, TRACTOR OEMs - CO-BRANDED) BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: C&M3004-0201 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: JULY 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

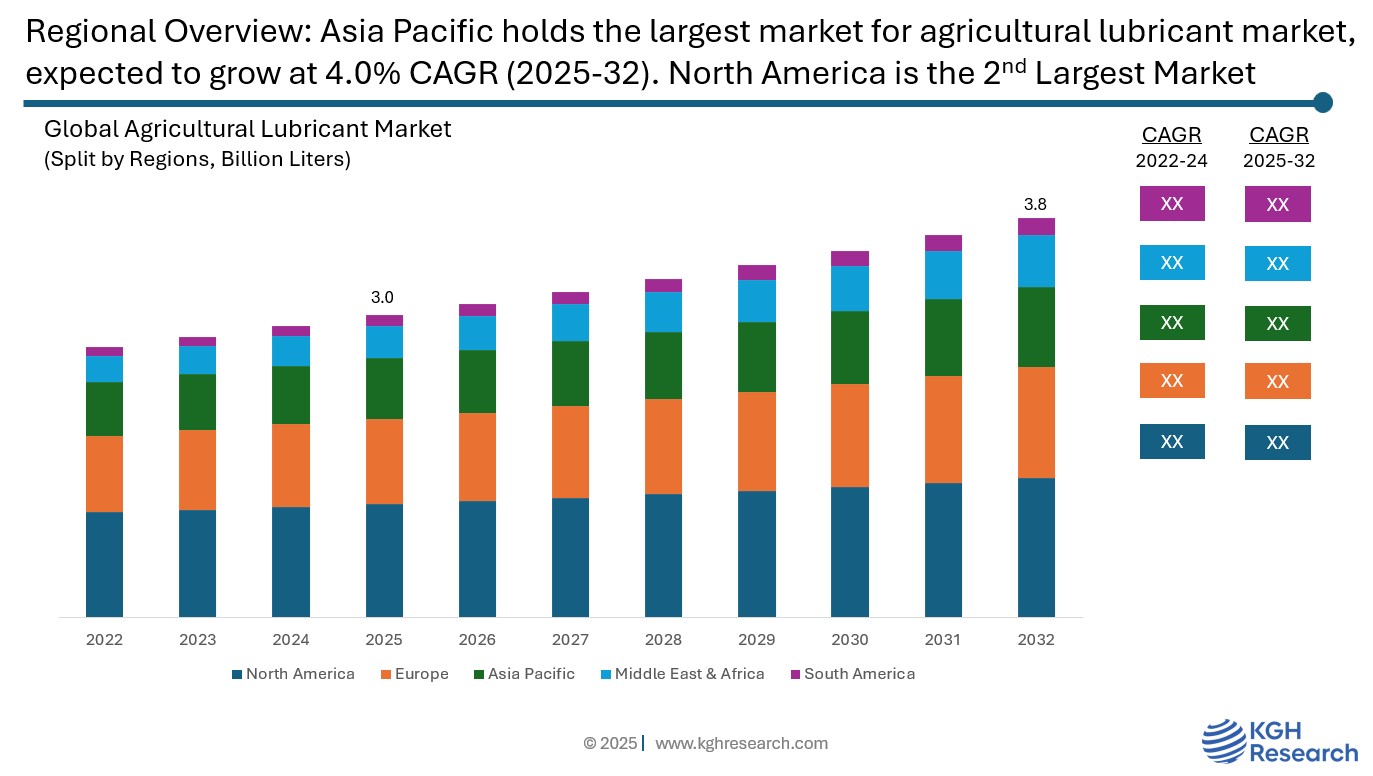

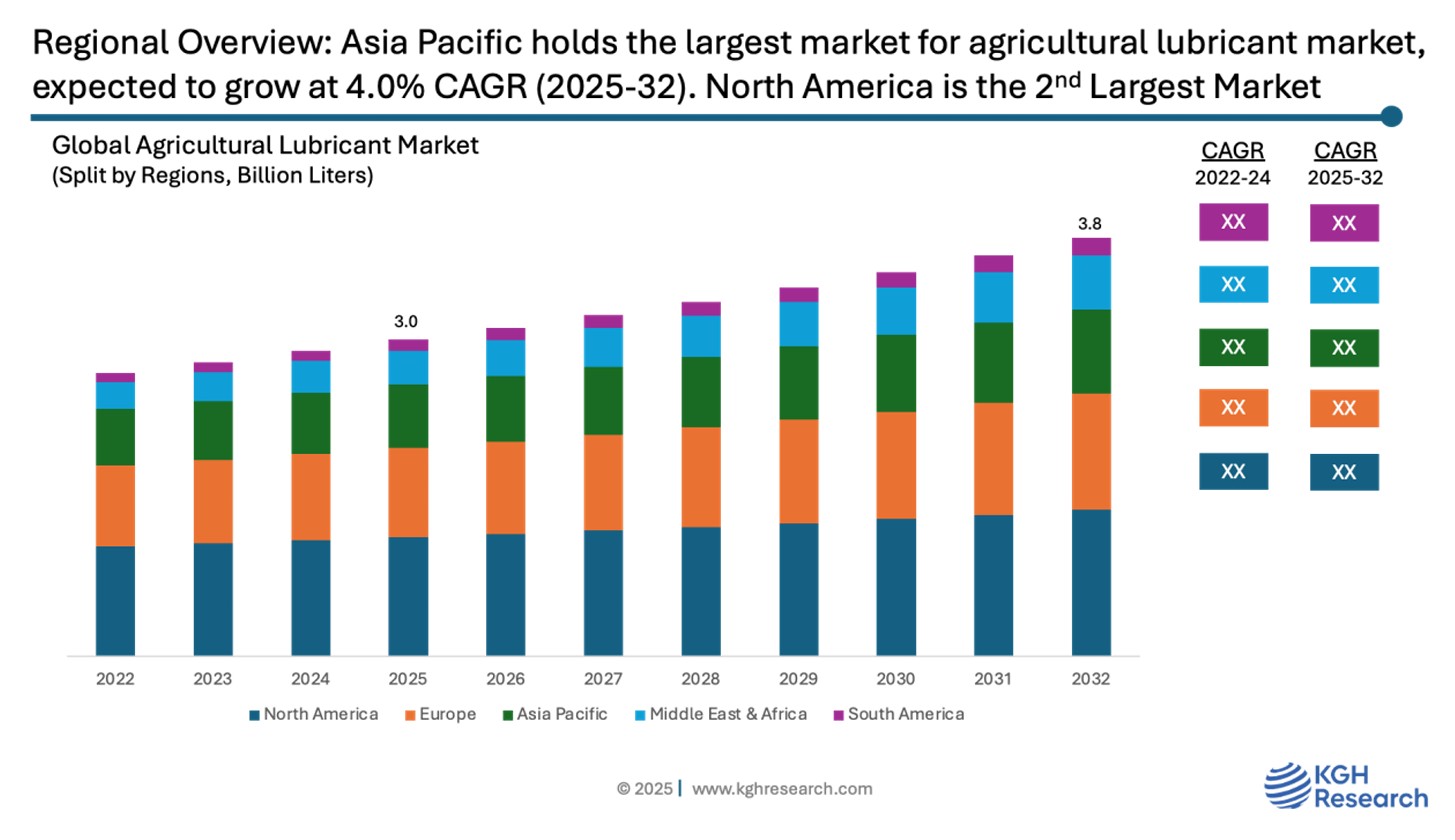

Market Overview: The global agricultural lubricant market is expected to achieve a market size of approximately 3.0 Billion liters in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 3.5% from 2025 to 2032 to reach 3.8 Billion liters by 2032. The market is being driven by the rapid mechanization of farming especially in emerging economies and huge agricultural tractor parc size are the two major drivers for the growth of the agricultural lubricants market. Increasing demand for high-performance lubricants to keep tractors, harvesters, and other machineries operational under extreme weather conditions; growing adoption of precision agriculture technologies, such as GPS-guided equipment and autonomous tractors, further increases need for specialized lubricants; rising food demand and government subsidies for equipment purchases boost market uptake; and mounting environmental regulations encourage the development and use of eco-friendly, biodegradable, and bio-based lubricants.

MARKET DYNAMIC

GROWTH DRIVERS:

- The growing mechanization rate in the global agriculture market, mainly in developing economies

- Growing demand for agriculture produce to cater the demand for increasing world population

- Huge tractor parc size, globally.

- Increasing trend towards organized and commercial large scale farming

- Growing demand for high HP tractors with large sump sizes to further boost the demand for agricultural lubricants.

- Driver 6

NEW GROWTH OPPORTUNITIES:

- Rising demand for bio-based and eco-friendly lubricants

- Demand for lubricants with extended drain interval and its ability to keep the equipment operational under extreme weather condition

- Autonomous tractors

- Opportunity 4

- Opportunity 5

MARKET RESTRAINTS:

- Volatility in crude oil prices

- Environmental risks & disposal issues with conventional lubricants

- Growing adoption of Electric Tractors, mainly in smaller size tractors.

GROWTH HURDLES:

- Compliance with varied regional regulations

- High R&D costs involved in developing eco-friendly and bio-based lubricants

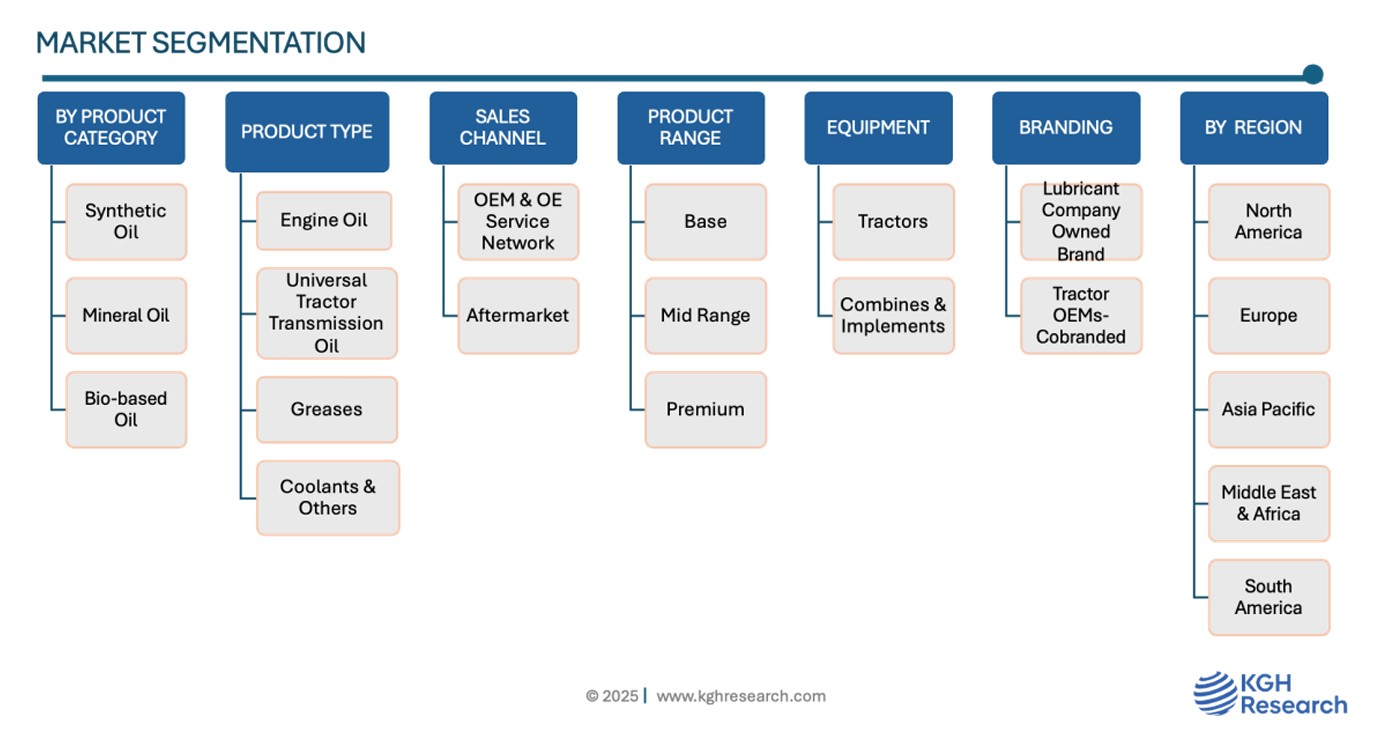

Product Category: Market Insights

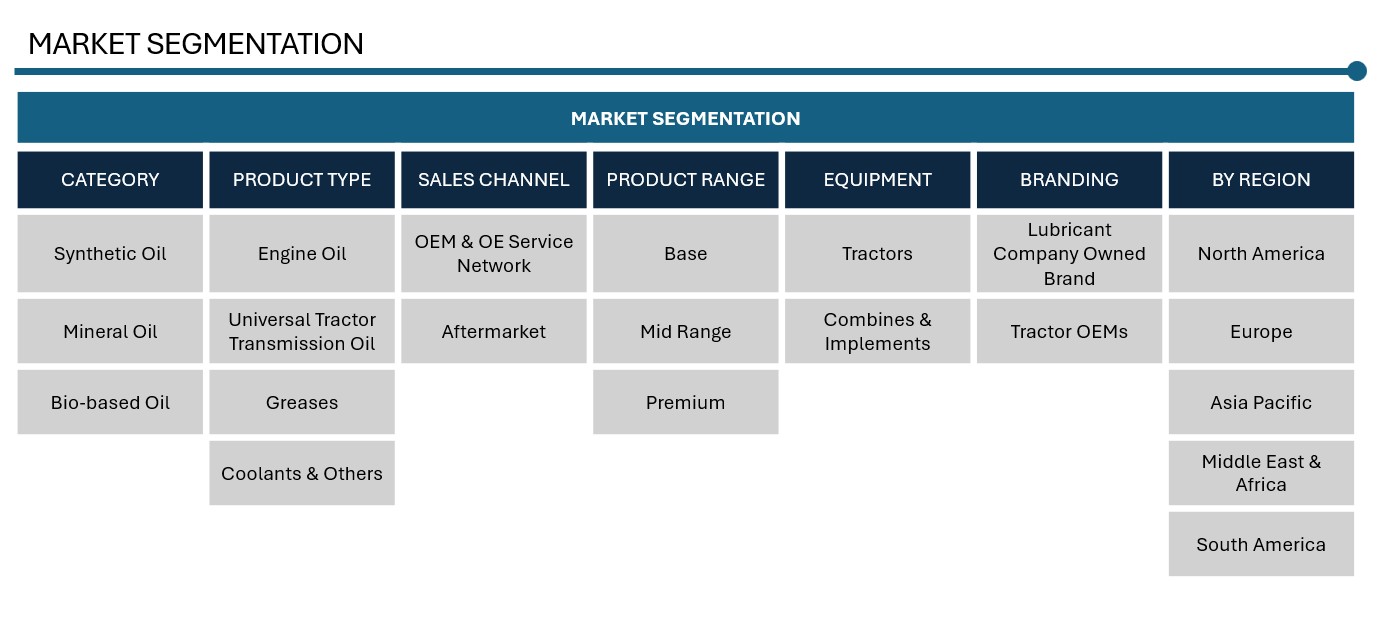

By product category, the agricultural lubricant market is mainly categorized into the mineral oil-based lubricants, synthetic oil-based lubricants, and bio-based lubricants. The mineral oil-based lubricant segment holds the largest share of the global agricultural lubricant market. This dominance is mainly due to their low cost, wide availability, and proven reliability in traditional farming machinery like transmissions, hydraulic systems, and gearboxes. Synthetic lubricant is gaining rapid adoption driven by high drain interval, exceptional performance under extreme weather conditions, and better performance compared to mineral oil-based lubricants. Bio-based lubricants likely to grow at much faster rate compared to other two types of fluids.

Product Type: Market Insights

The global agricultural lubricant market is segmented into four main product types: engine oil, universal tractor transmission oil (UTTO), greases, and coolants & others. Engine oil holds a significant share as it is essential for reducing wear and tear in tractor engines. UTTO is specifically designed for tractors and similar equipment, offering lubrication for transmissions, hydraulic systems, and wet brakes, ensuring optimal performance and durability. Greases are used in various moving parts of farm equipment to provide long-lasting protection under harsh operating conditions. The coolants & others category include products that help regulate engine temperature and protect against corrosion, contributing to the overall efficiency and longevity of agricultural equipment.

Equipment: Market Insights

By equipment, the agricultural lubricant market is segmented into tractors and combines & implements. Tractors represent the largest share due to their widespread use in a variety of farming operations, requiring regular maintenance and lubrication to ensure efficient performance and long service life coupled with huge operational parc size of tractors, globally. Combines and implements, which include harvesters, plows, seeders, and other attachments, also significantly contribute to lubricant demand, as they operate under tough conditions and require specialized lubrication to reduce wear, prevent breakdowns, and enhance productivity in the field.

Product Range: Market Insights

By product range, the agricultural lubricant market is segmented into base, mid-range, and premium. Base-grade lubricants are cost-effective and cater to standard lubrication needs for older or less demanding machinery. Mid-range lubricants offer a balance between performance and affordability, providing better protection and efficiency for commonly used agricultural equipment. Premium lubricants are high-performance products designed for modern, high-load machinery, offering superior protection, longer service intervals, and enhanced operational efficiency under extreme conditions, making them ideal for intensive agricultural operations.

Sales Channel: Market Insights

By sales channel. Aftermarket segment accounted for the more than 3/4th share of the global agricultural lubricant market, followed by OEM (1st Fill) & OE Service Network. The Right to Repair Act, gaining momentum across multiple U.S. states, has profound implications for the agricultural machinery ecosystem. This legislation mandates that original equipment manufacturers (OEMs) must provide farmers and independent repair shops access to essential diagnostic tools, software, and technical documentation. Historically, OEMs have restricted access to these resources, forcing farmers to rely exclusively on authorized service centers for even minor repairs, leading to downtime and higher costs.

Impact on Lubricants Market

The Right to Repair movement is democratizing maintenance. Farmers and local mechanics are now more empowered to service equipment themselves, leading to a rise in demand for high-quality, user-friendly lubricants and greases that can be easily procured and applied outside of OEM service channels. This shift opens new retail and aftermarket distribution opportunities for lubricant suppliers. It’s also pushing brands to enhance labelling, compatibility information, and packaging to cater to a broader, non-specialist user base.

Branding: Market Insights

By branding, the agricultural lubricant market is segmented into lubricant company-owned brands and tractor OEMs (Original Equipment Manufacturers)-Co-Branded Lubricants. Lubricant company-owned brands are produced and marketed by specialized lubricant manufacturers and are widely available across various distribution channels, often recognized for their technical expertise and broad product portfolios and accounted for the largest share of the market. Tractor OEMs Co-Branded Lubricants are often marketed through OE Service & Dealership Networks as a tailored lubricants specifically for their machinery, ensuring compatibility and optimal performance. These Tractors OEM co-branded lubricants are typically recommended in maintenance manuals and are preferred by users looking to maintain warranty compliance and equipment reliability.

Regional: Market Insights

Asia Pacific dominates the global agricultural lubricant market due to a combination of large-scale agricultural activity, rapid mechanization, and increasing investments in farm infrastructure. Countries such as India and China, which are among the world’s largest agricultural producers, significantly contribute to the region’s agricultural lubricant demand through their extensive use of tractors, harvesters, tillers, and other equipment. As these nations continue to shift from traditional farming practices to modern, machinery-driven methods, the need for high-quality lubricants to maintain operational efficiency and reduce equipment downtime has surged.

Government support programs and subsidies aimed at promoting farm mechanization, such as India’s Sub-Mission on Agricultural Mechanization (SMAM) have also played a crucial role in driving the sales of agricultural machinery, thereby boosting lubricant consumption. Additionally, the growth of contract farming, increasing rural incomes, and the expansion of agri-business services in countries like Vietnam, Indonesia, and Thailand have further supported this trend.

The region is also witnessing a shift toward premium and synthetic lubricants, especially in developed economies such as Japan and South Korea, where farmers are adopting advanced machinery with more demanding lubrication needs. Moreover, the presence of major global and regional lubricant manufacturers, such as Indian Oil Corporation, Sinopec, and BP-Castrol, ensures a steady supply chain and increasing brand competition, which accelerates product innovation and accessibility. Overall, Asia Pacific’s favorable agriculture climatic conditions, rising food security needs, and proactive government policies make it the most dynamic and fastest-growing region in the global agricultural lubricant market.

Competition: Agricultural lubricant

The Agricultural lubricant market is highly competitive, with key players focusing on product innovation, product efficiency and performance improvement, sustainable product development, and strategic partnerships to strengthen their market position. Major companies include Exxon Mobil, Shell plc, BP plc, TotalEnergies SE, CEMEX, Fuchs, Chevron Corporation, Lukoil, Petronas, Sinopec, Idemitsu Kosan Co., Ltd, and many more. These players are investing in R&D to develop lubricants tailored for agriculture applications, driving ongoing competition and technological advancement in the market.

Exxon Mobil Corporation is one of the world’s leading producers and suppliers of agricultural lubricant, offering a comprehensive range of high-performance products designed to meet the demanding needs of modern farming equipment. Headquartered in Irving, Texas, ExxonMobil operates globally with a strong presence across key agricultural regions, including North America, Europe, Asia Pacific, and Latin America. The company’s agricultural lubricant portfolio includes engine oils, transmission fluids, greases, and hydraulic oils marketed under well-established brands such as Mobil Delvac™ and Mobilfluid™.

ExxonMobil’s products are engineered to enhance equipment performance, reduce maintenance costs, and extend machinery life by offering superior protection under extreme operating conditions often encountered in farming environments. With a strong emphasis on research and development, the company continually innovates its lubricant technologies to meet evolving regulatory standards and customer needs, including the growing demand for fuel efficiency and environmental sustainability. Through its extensive distribution network and collaborations with OEMs (Original Equipment Manufacturers), ExxonMobil ensures that its agricultural lubricant are readily available and compatible with a wide range of machinery. The company also provides value-added services such as oil analysis programs and technical support to help farmers optimize equipment reliability and productivity. With decades of industry expertise and a commitment to quality and innovation, ExxonMobil remains a trusted partner for agricultural professionals worldwide.

BP plc, headquartered in London, United Kingdom, is a prominent global energy company and a key player in the agricultural lubricant market. Through its well-known lubricant brand Castrol, BP offers a wide range of high-performance lubricants tailored specifically for agricultural machinery. These include engine oils, hydraulic fluids, transmission oils, and greases designed to ensure reliable performance and protection for tractors, harvesters, and other farm equipment operating under challenging conditions. Castrol’s agricultural lubricant are formulated to improve equipment efficiency, extend service life, and minimize downtime by providing excellent wear protection, corrosion resistance, and thermal stability. Products such as Castrol Agri MP Plus and Castrol Transmax Agri Trans are widely used by farmers and are engineered to meet or exceed the specifications of major agricultural OEMs. BP’s strong global distribution network, combined with its partnerships with machinery manufacturers and agricultural equipment dealers, ensures easy access to its lubricant solutions across major farming regions in Europe, Asia, and the Americas. The company also emphasizes sustainability by developing lubricants that support fuel economy and reduce environmental impact, aligning with global trends toward cleaner and more efficient farming practices. With a longstanding reputation for innovation, quality, and technical support, BP through its Castrol brand continues to play a vital role in advancing lubricant solutions that meet the evolving needs of the agricultural sector.

AGRICULTURAL LUBRICANT MARKET SNAPSHOT | |

Market size in 2025 | 3.0 Billion Liters |

Market forecast in 2032 | 3.8 Billion Liters |

Compound Annual Growth Rate (2025-2032) | 3.5% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Major Drivers & Trends | Increasing mechanization rate, huge tractor parc size, globally, organized & commercial farming, sustainability trend, extended drain interval, growing demand for agricultural produce, growing awareness amongst farmers about the benefits of timely lube replacement in driving operational efficiency and profitability in developing economies. |

Segments Covered | Category, Product Type, Product Grade, Branding, Sales Channel, Product Range, and Region & Country |

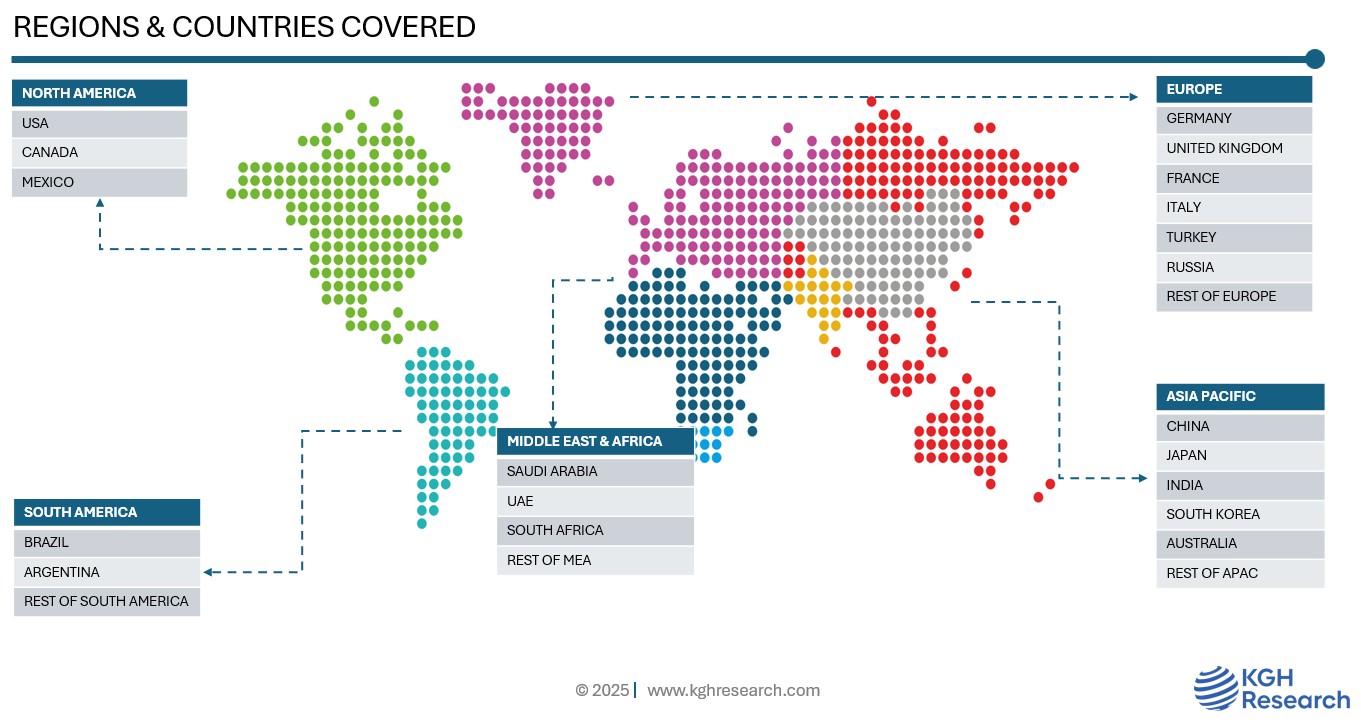

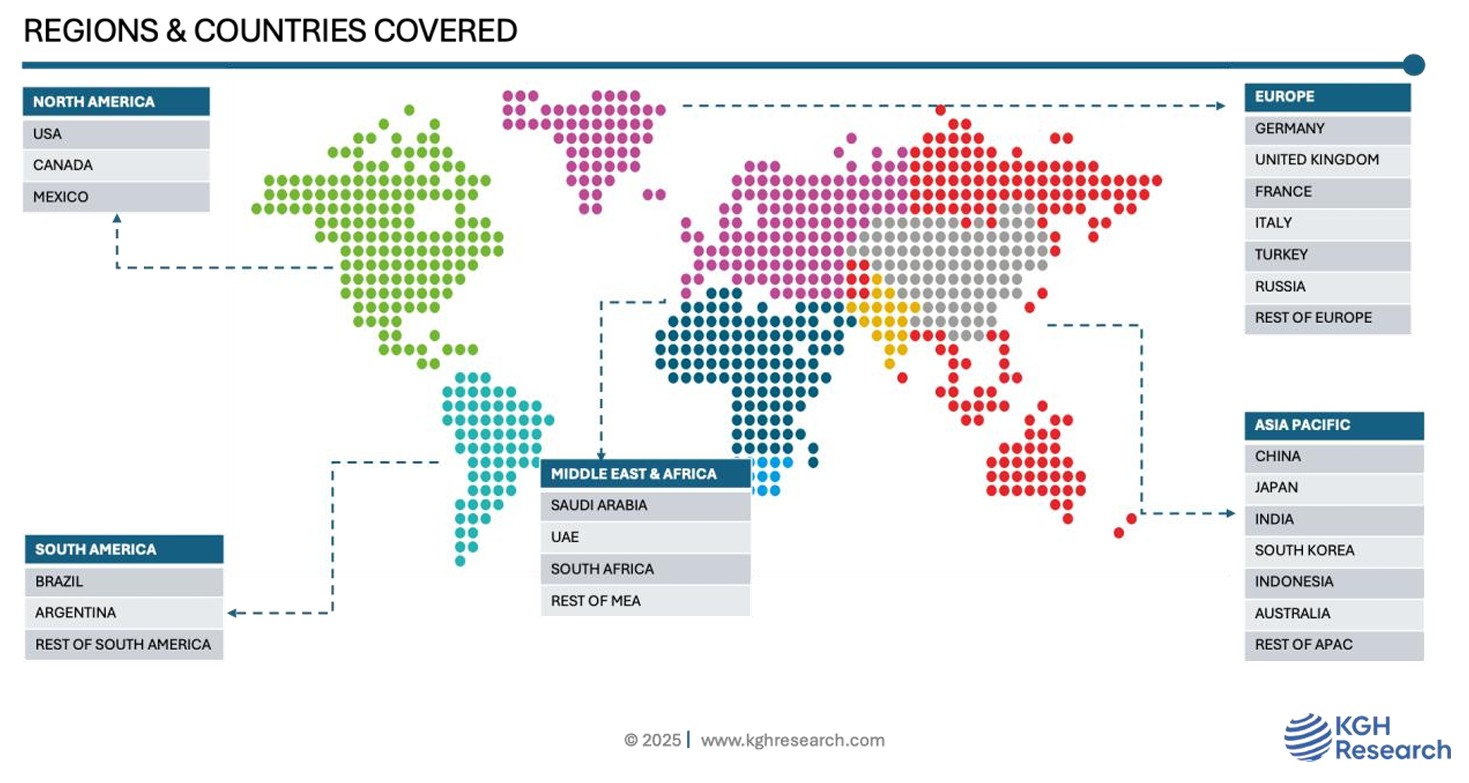

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, France, Turkey, Russia, France, Spain, China, India, Japan, Indonesia, South Korea, Australia, South Africa, UAE, Saudi Arabia, Brazil, Argentina |

Companies Profiled (25+) | CHEVRON CORPORATION, BP PLC, EXXON MOBIL CORPORATION, TOTAL ENERGIES, VALVOLINE, SINOPEC LUBRICANT COMPANY, BPCL, ENEOS, HPCL, FUCHS, REPSOL, IOCL, LUKOIL, PETRONAS, GULF OIL , CENEX, INTERNATIONAL LTD., RYMAX LUBRICANT, CLAAS, JOHN DEERE, NEW HOLLAND. IDEMITSU KOSAN CO., LTD., AND MANY MORE |