Electric Motor for EV (2022 - 2032)

ELECTRIC MOTORS FOR ELECTRIC VEHICLES MARKET SIZE & SHARE BY CURRENT TYPE (AC, DC), BY MOTOR TYPE (PERMANENT MAGNET MOTORS, AC INDUCTION MOTOR, WRMS, AXIAL FLUX MOTORS, SRM, IN-WHEEL MOTORS, BLDC) BY VEHICLE TYPE (BATTERY EV, HYBRID EV, PLUG IN HYBRID EV, FUEL CELL EV), BY OUTPUT POWER (UP TO 75 KW, 75 KW TO 150 KW, ABOVE 150 KW), BY EV CATEGORY (PASSENGER CARS, LCV, HCV, ELECTRIC SCOOTER & BIKE, OTHERS), BY ASSEMBLY (WHEEL HUB, POWERTRAIN) AND BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: E&P4011-0709 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2019 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: JULY 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

Market Overview: The global electric motor for electric vehicles market was valued at approximately USD XX billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of >15% from 2025 to 2032 to reach USD XX billion by 2032. The global electric motors market for electric vehicles (EVs) is growing rapidly, and this growth comes from a mix of environmental, technological, and economic reasons. Governments are setting stricter rules to cut carbon emissions. They also support these efforts with subsidies, tax incentives, and zero-emission targets. These factors are pushing the quick adoption of EVs around the world. The falling prices of batteries and the growth of Electric Vehicle (EV) charging stations are making electric vehicles easier to get and use for consumers. Major car manufacturers are also putting a lot of funds into EV production. This is creating a huge increase in the need for high-performance electric motors.

MARKET DYNAMIC

GROWTH DRIVERS:

- Surge in electric vehicle (EV) adoption

- Strict emission regulations and government incentives

- Lower battery prices reduce EV costs, indirectly driving demand for electric motors

- DRIVER 4

NEW GROWTH OPPORTUNITIES:

- Growth in emerging markets

- Development of rare-earth-free motors

- Two- and three-wheeler electrification

- OPPORTUNITY 4

MARKET RESTRAINTS:

- High initial cost of EVs

- Complex design & control requirements

- Thermal management challenges

GROWTH HURDLES:

- Intense market competition

- Trade tensions, especially around rare-earth materials, can disrupt supply chains and pricing

- Global economic downturns, inflation, or reduced consumer spending can temporarily stall EV sales and motor demand

- Limited charging infrastructure in developing regions

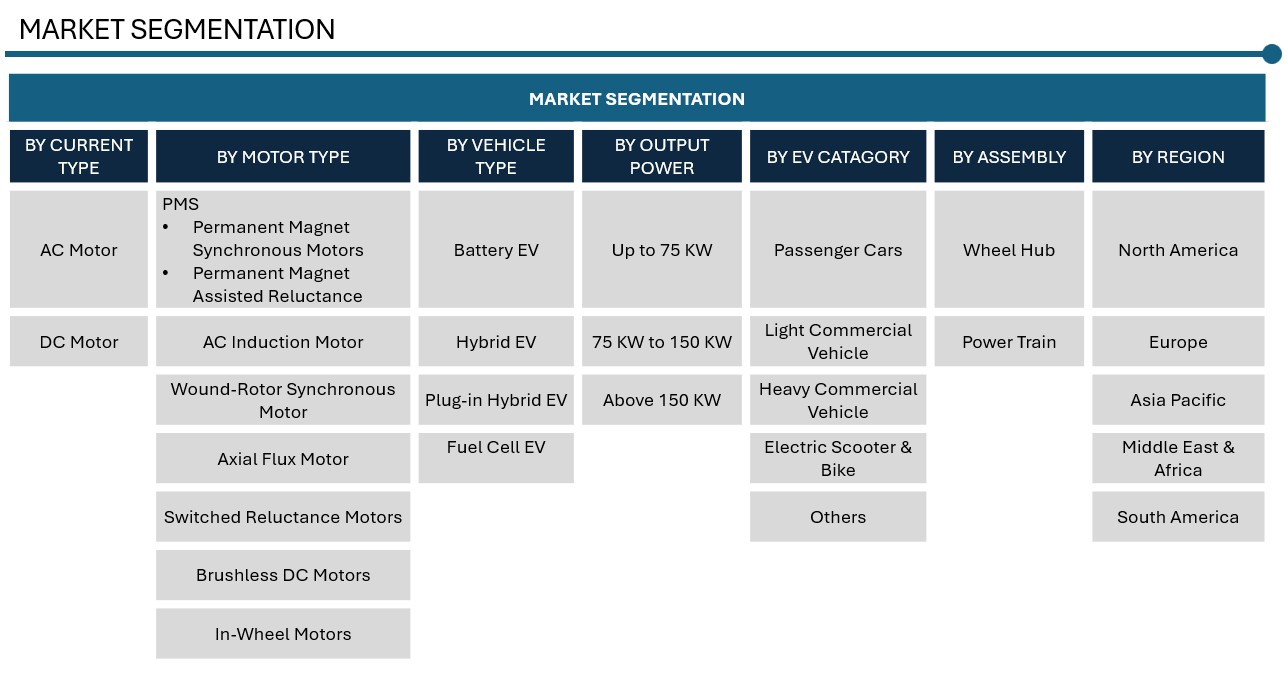

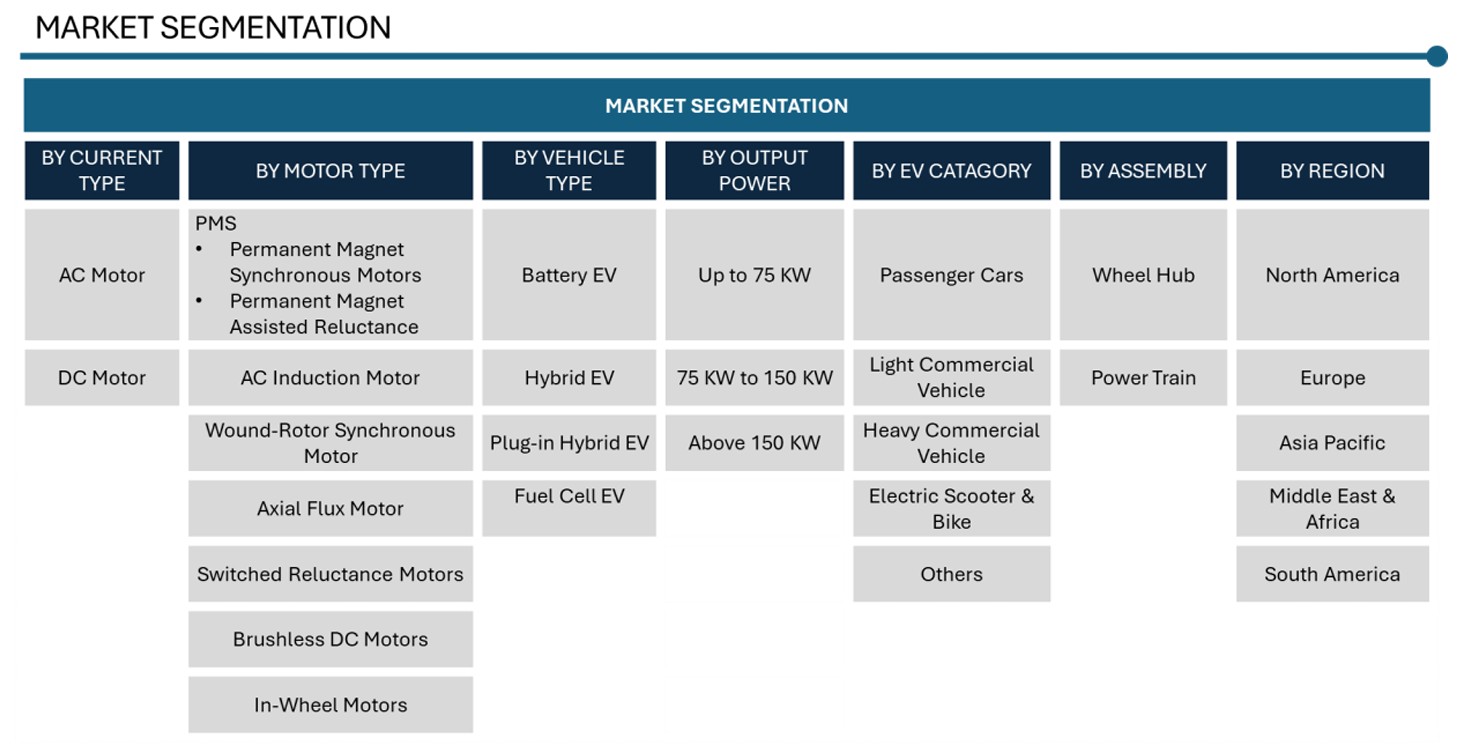

Motor Type: Market Insights

The electric motors market for electric vehicles is divided by motor type into several main categories, each with unique features and uses. Permanent Magnet Motors are the most common in EVs constituting more than 70% share of the total market they offer high efficiency, compact size, and strong torque. This category includes Permanent Magnet Synchronous Motors (PMSMs), which are often found in popular electric vehicles like the Nissan Leaf and various Tesla models. AC Induction Motors are also common; they are known for their durability and lower cost. These motors were used in most of the Tesla vehicles. Wound-Rotor Synchronous Motors provide precise control of magnetic fields and are suitable for high-performance EVs. However, due to their complexity and higher cost, they are less widely used. Axial Flux Motors are becoming more popular because of their thin, lightweight design and high torque density, making them ideal for tight spaces and performance-focused applications. Switched Reluctance Motors are simpler and cheaper to make but face issues with noise and control complexity. Nevertheless, improvements in power electronics are enhancing their potential in EVs. In-Wheel Motors are an innovative option that places the motor directly in the wheel hub. This design allows for better handling and flexibility, especially in compact urban vehicles and advanced mobility concepts. Brushless DC motors (BLDC) in the electric vehicle are widely adopted for their high efficiency, excellent torque-to-weight ratio, and low maintenance requirements. Unlike conventional brushed motors, BLDC motors use electronic commutation, which minimizes wear and extends lifespan, making them ideal for EV applications. These motors are material of choice in two-wheelers, three-wheelers, and light electric vehicles due to their compact size and energy efficiency. Additionally, their ability to deliver precise speed and torque control enhances vehicle performance and driving experience. Leading EV manufacturers integrate BLDC motors in powertrains, electric scooters, e-bikes, and auxiliary functions such as HVAC systems and power steering.

Current Type: Market Insights

By motor type, the electric motor market for electric vehicles (EVs) is divided into AC motors and DC motors. AC motors, including induction motors, permanent magnet synchronous motors (PMSM), and switched reluctance motors, lead the market because of their high efficiency, great performance, and fit for high-speed and long-range EV uses. These motors are commonly found in passenger cars, commercial EVs, and performance vehicles. In contrast, DC motors, mainly brushless DC (BLDC) motors, are popular in low-speed electric vehicles like electric scooters, bikes, and three-wheelers, especially in budget-conscious markets. Their simple design, ease of control, and affordability make them suitable for lightweight EV applications.

Vehicle Type: Market Insights

By vehicle type, the electric motor market for electric vehicles is divided into passenger cars, light commercial vehicles (LCVs), heavy commercial vehicles (HCVs), electric scooters and bikes, and others like buses. Passenger cars make up the largest share because more consumers are choosing electric cars. There is also strong support from governments through subsidies and emission rules. LCVs and HCVs are increasingly using electric drivetrains for logistics and public transport. This shift is driven by the need for lower operating costs and cleaner urban mobility. The segment for electric scooters and bikes is growing quickly, especially in Asia-Pacific, thanks to their affordability, ease of use, and increasing fuel prices. The “other” category, which includes electric buses, is also gaining traction as cities worldwide move toward greener public transportation systems.

EV Category: Market Insights

By EV category, the electric motor market is divided into Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Fuel Cell Electric Vehicles (FCEVs). Battery Electric Vehicles (BEVs) lead the market because they operate without emissions, have a longer driving range, decrease battery costs, and more charging infrastructure worldwide. Hybrid Electric Vehicles (HEVs) still hold a significant share as a transitional option. They combine internal combustion engines with electric power to improve fuel efficiency. Plug-in Hybrid Electric Vehicles (PHEVs) allow for electric-only driving with a gasoline engine as a backup, which appeals to consumers concerned about range. Fuel Cell Electric Vehicles (FCEVs) are still developing but are attracting interest in long-range and heavy-duty uses, especially where quick refueling and extended range are important.

Assembly: Market Insights

By assembly, the electric motor market for electric vehicles is divided into wheel hub motors and powertrain motors. Powertrain motors lead the market because they are commonly used in most electric vehicles to drive the main axle with a central motor that is part of the drivetrain. These motors provide high efficiency and strong performance, making them ideal for both high-speed and heavy-load situations. In contrast, wheel hub motors, which are mounted directly in the wheels, are becoming more popular because of their compact design, better torque distribution, and ability to remove the need for traditional transmission parts. They are particularly suitable for lightweight electric vehicles and offer design flexibility. However, issues like heat dissipation and unsprang weight currently limit their widespread use.

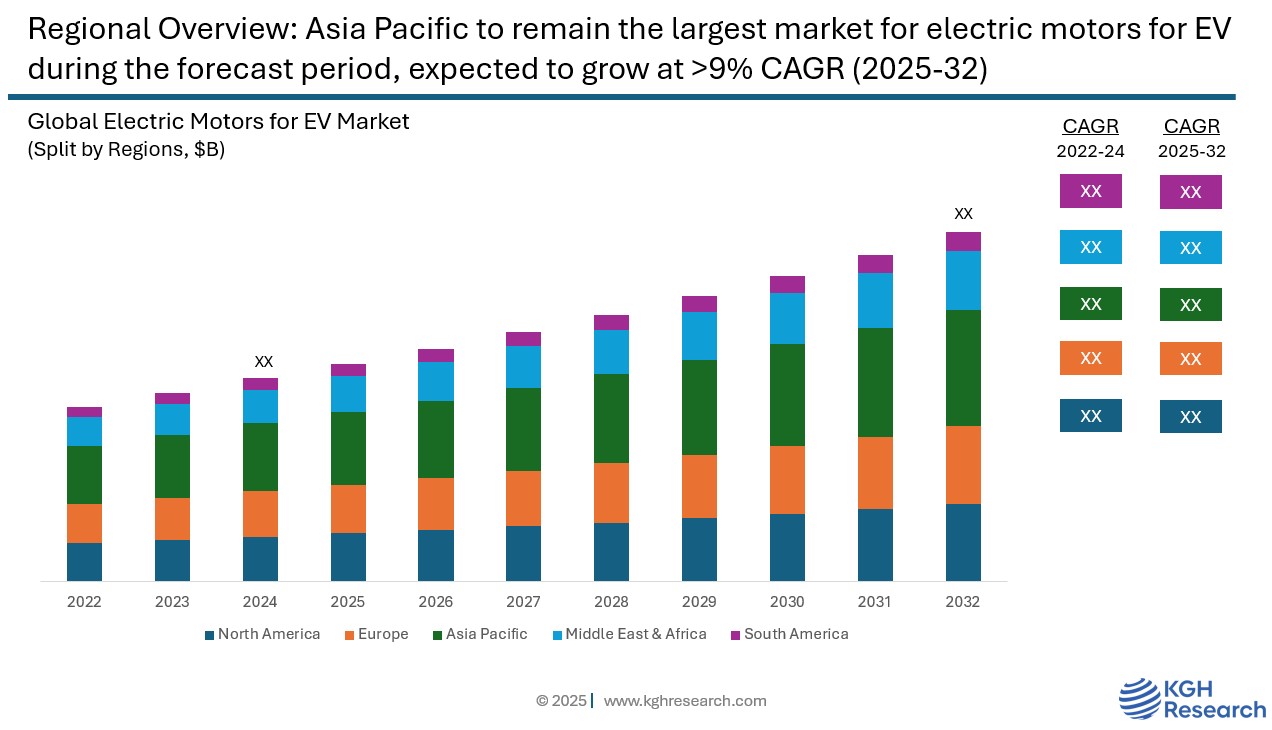

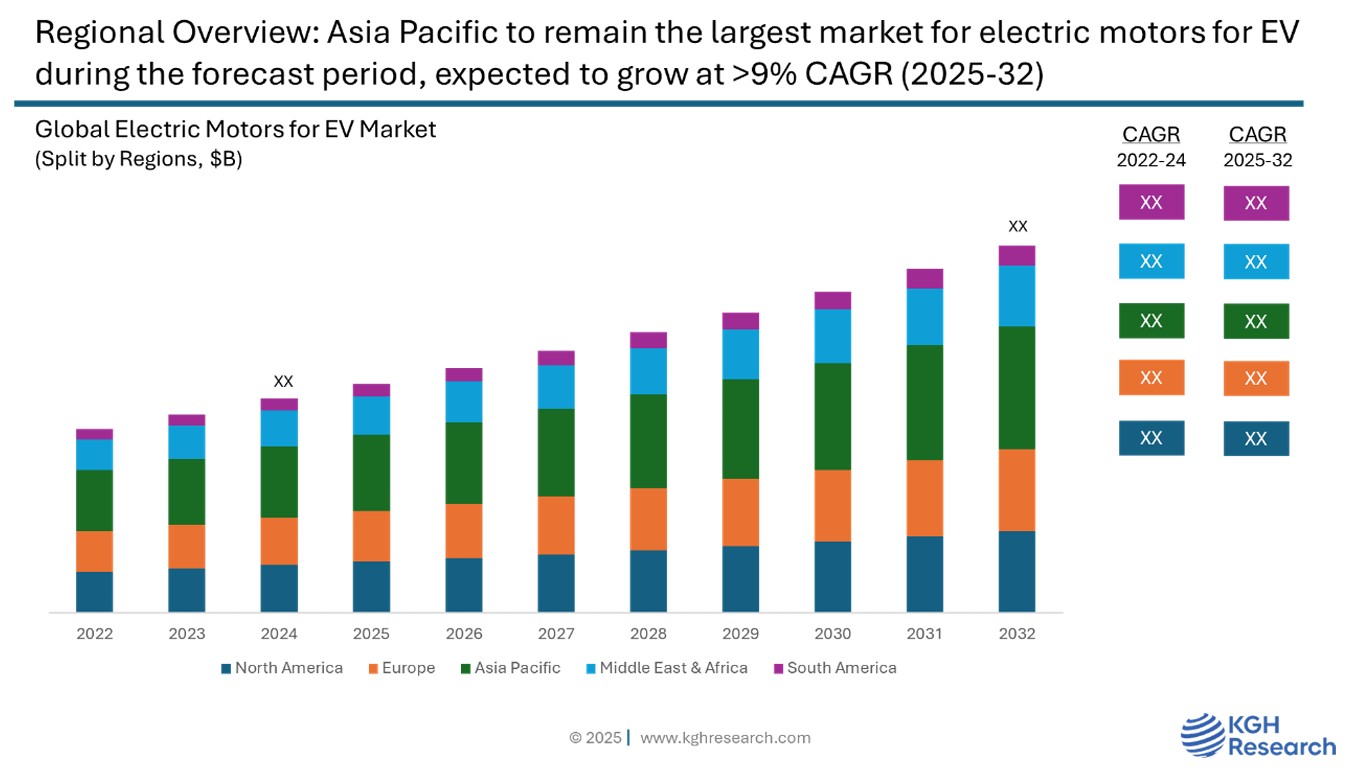

Regional: Market Insights

Asia Pacific currently leads the electric motor market for electric vehicles. This is due to high production capacity, strong policy support, and rapidly growing domestic demand. China stands at the forefront of this region and the entire world, holding the largest share of EV sales and electric motor manufacturing. The Chinese government has introduced strong policies like subsidies, tax incentives, and strict emission rules to speed up the shift to electric mobility. Additionally, major EV makers like BYD, NIO, and XPeng, along with electric motor companies like NIDEC and Wolong Electric, significantly strengthen the region’s market.

Japan and South Korea also have important roles. They are known for technological innovation and host leading automakers and suppliers such as Toyota, Honda, Hyundai, and LG. These countries invest heavily in research and development, especially in motor technologies, including permanent magnet synchronous motors and rare-earth-free options.

India, while still developing its electric passenger car market, has seen rapid growth in the two-wheeler and three-wheeler EV segments, which are more accessible to the public. Government programs like the FAME (Faster Adoption and Manufacturing of Hybrid and Electric Vehicles) scheme, along with state-level incentives and infrastructure improvements, are boosting local electric motor demand.

Furthermore, the region has a strong supply chain for essential components like magnets, copper windings, and electronic controllers, which supports cost-effective mass production. With increasing urbanization, rising fuel prices, and growing environmental concerns, Asia Pacific is likely to maintain its leadership in the global electric motor market for EVs in the coming years.

Competition: Electric Motors

The competitive landscape of the electric motors market for electric vehicles is dynamic and rapidly evolving due to the global shift toward clean mobility. Major car makers and component companies are investing a lot in electric motor technologies to improve vehicle efficiency, performance, and range. Leading companies like Nidec Corporation, Wolong Electric, Allied Motion, Inc., Robert Bosch, Hitachi, Yaskawa, Siemens, Johnson Electric, Ametek Inc., ABB Ltd. are leading the way. They provide various motor types, including permanent magnet synchronous motors (PMSM), brushless DC motors (BLDC), and induction motors designed for EV use. These companies focus on compact designs, lightweight materials, and high power-to-weight ratios to meet the needs of both passenger and commercial electric vehicles. The market also sees strategic partnerships, mergers, and acquisitions aimed at increasing production capacity and improving integration within the EV powertrain ecosystem. New companies and startups are entering the market, especially in Asia-Pacific and Europe. This increases competition and drives innovation. As governments around the world set stricter emissions standards and promote EV adoption, competition is likely to grow more intense, focusing on cost-effectiveness, motor control software, and energy optimization.

Nidec Corporation is one of the global leaders in the design, manufacture, and sale of electric motors and related components. Headquartered in Kyoto, Japan, Nidec has established itself as a key player in the industry, particularly in the small precision motors segment. The company’s diverse product portfolio includes motors for hard disk drives, automotive applications, home appliances, industrial equipment, and commercial use. Nidec is known for its innovative technologies and strong emphasis on energy efficiency, which has positioned it at the forefront of the shift toward electrification and automation across industries. With a global network of manufacturing and R&D facilities, Nidec continues to expand its presence and influence as a critical supplier in the electric motors for electric vehicle market worldwide.

ELECTRIC MOTORS FOR ELECTRIC VEHICLE MARKET SNAPSHOT | |

Market size in 2024 | USD XX Billion |

Market forecast in 2032 | USD XX Billion |

Compound Annual Growth Rate (2025-2032) | >10.0% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Growth Drivers | Surge in electric vehicle (EV) adoption, Strict emission regulations and government incentives, Lower battery prices reduce EV costs, indirectly driving demand for electric motors |

Segments Covered | Motor Type, Current Type, Vehicle Type, EV Category, Assembly, Power Output, and Region |

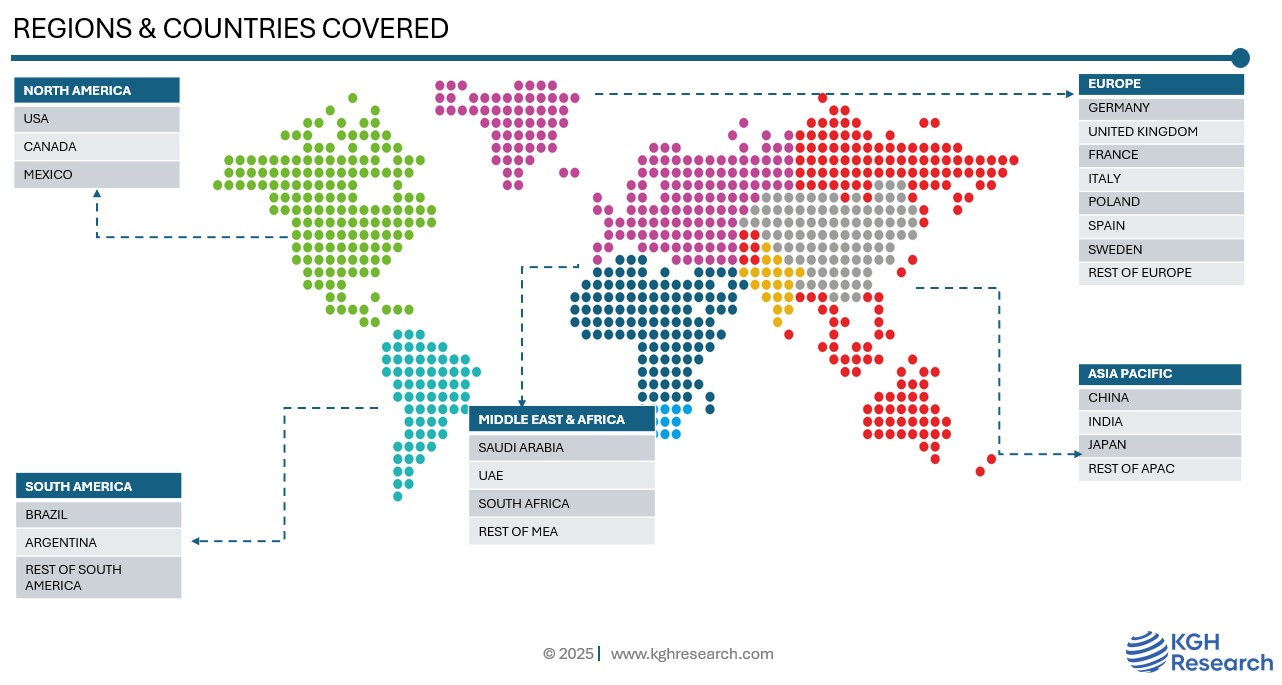

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, France, Poland, Sweden, UK, Spain, China, India, Japan, UAE, South Africa, Brazil, Argentina |

Companies Profiled | NIDEC, SIEMENS AG, ABB GROUP, BROSE FAHRZEUGTEILE SE & CO. KG, JOHNSON ELECTRIC, TOSHIBA CORPORATION, HITACHI, ALLIED MOTION, AMETEK INC., WOLONG ELECTRIC CORPORATION, ROBERT BOSCH GMBH, YASKAWA ELECTRIC CORPORATION, OTHERS. |