Data Center (2022 - 2035)

DATA CENTER MARKET SIZE & SHARE BY INFRASTRUCTURE TYPE (NETWORK & IT EQUIPMENT, COOLING INFRASTRUCTURE, POWER INFRASTRUCTURE, AND OTHER CRITICAL INFRASTRUCTURE), BY DATA CENTER TYPE (HYPERSCALER, COLOCATION, AND ENTERPRISE), BY WORKLOAD (AI BASED, NON-AI BASED, AND CRYPTOCURRENCY MINING), BY SOLUTION & SERVICES, BY END USE, BY HARDWARE, SOFTWARE, AND SERVICE, BY INSTALLATION (FIRST FIT AND REPLACEMENT / REFRESH), AND BY REGIONS & KEY COUNTRIES – FORECAST TO 2035

| Report Code: ICT7001-0601 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: JULY 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

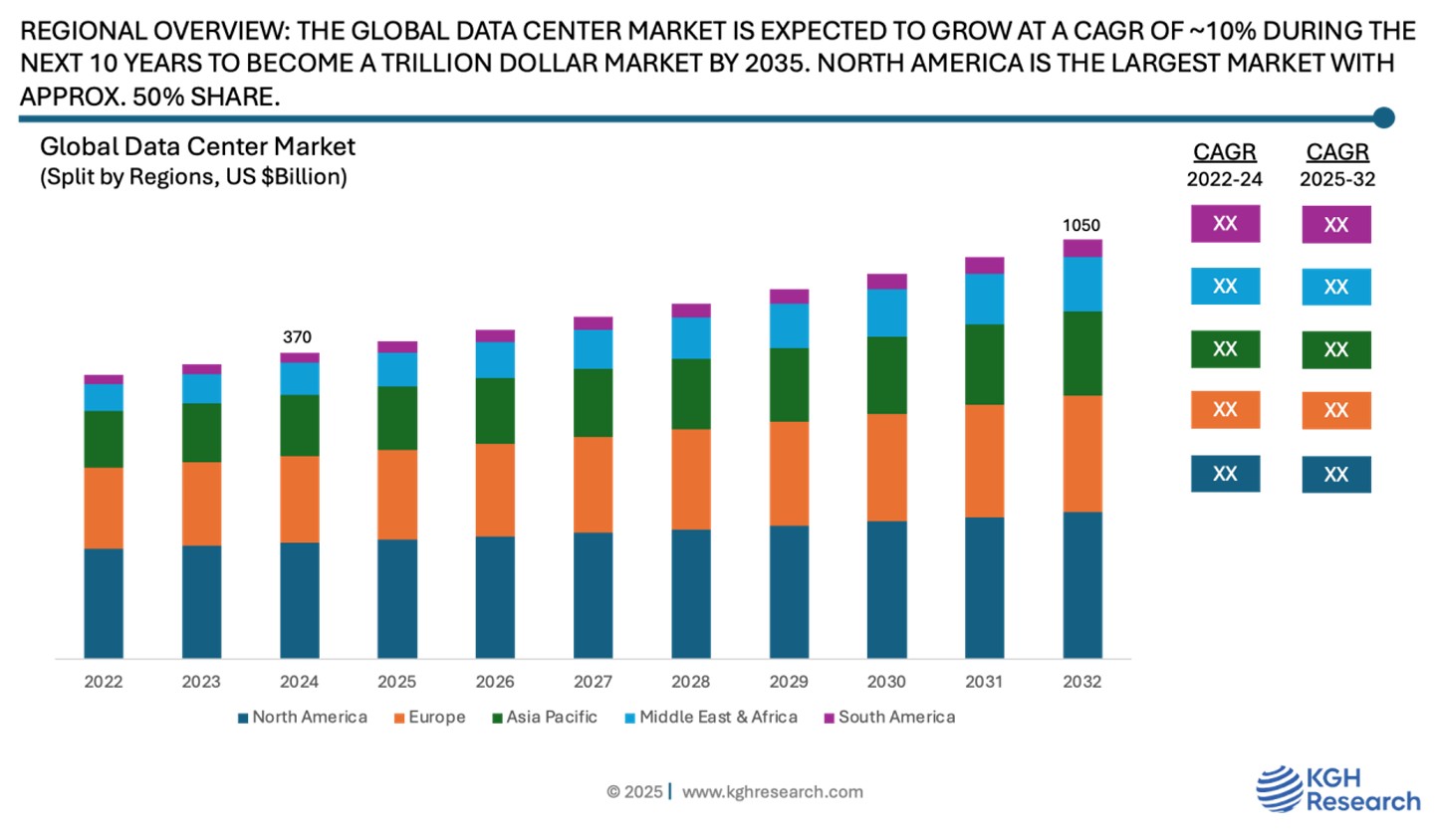

Market Overview: The global data center (infrastructure) market is estimated at US $370 Billion (incl. replacement/refresh spending) in 2024, and this market is expected to grow at a CAGR (2025 – 2035) of approx. 10% to become a trillion-dollar market opportunity by 2035 The growth is attributed to two prime drivers, that are increasing deployments of compute heavy AI based mega data centers, globally and increasing data center installation worldwide.

MARKET DYNAMIC

GROWTH DRIVERS:

- The global data center market is expected to grow at a CAGR of ~10% (2024-35) years, driving huge investment on Data Center infrastructure

- Increasing adoption of Generative & Specialized AI is driving huge investments on infrastructure in the AI based mega data center

- Driver 3: Refer Report

- Driver 4: Refer Report

- Driver 5: Refer Report

NEW GROWTH OPPORTUNITIES:

- The specialized chips and dense architectures at the heart of AI data centers likely to remain the key driver for the market growth during the forecast period

- Increasing rack density to meet the demand for compute heavy workloads driving demand for expensive, but highly reliable liquid cooling solutions

- Waste heat energy recovery from data center in district heating, power generation, and agriculture to add new revenue stream for infrastructure providers & DC owners & Operators

- Growth Opportunities 4: Refer Report

MARKET RESTRAINTS:

- With growing data center installation around the world, the energy demand is growing exponentially. Huge investment is needed in the energy generation industry to keep up with the pace of data center growth

- Market Restrainer 2: Refer Report

- Market Restrainer 3: Refer Report

GROWTH HURDLES:

- Regulatory pressure to reduce excessive heat generation, water usage, and green-house gas emission from data center and ancillary industries supporting data centers putting immense pressure on data center owners & operators and infrastructure providers, globally

- Growth Hurdle 2: Refer Report

- Growth Hurdle 3: Refer Report

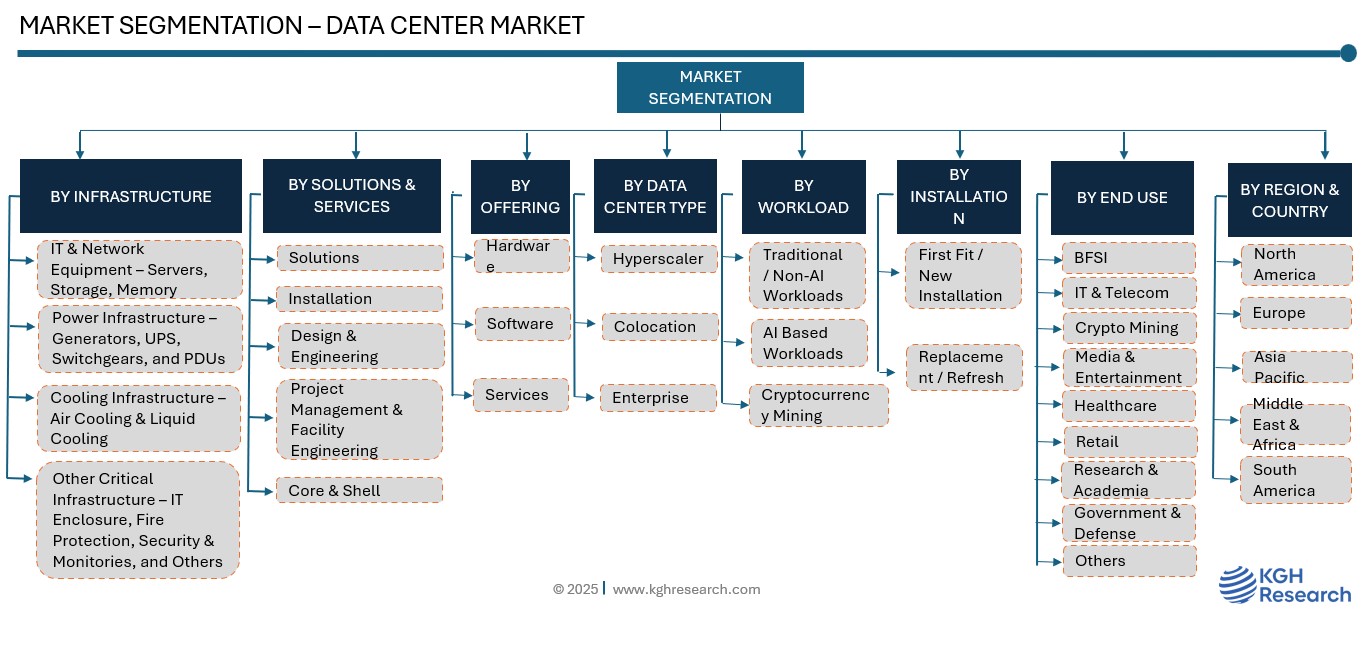

By Infrastructure Type: Market Insights

By Infrastructure: An average spent (CAPEX) on establishing a data center with 1 MW of IT load could typically cost in between US $20 to $25 Million incl. Network & IT Equipment.

Network & IT Equipment includes Servers, Networking, and Storage equipment accounted for more than 70% share of the global data center infrastructure CAPEX market, with a spent of over US $260 Bn in 2024 and to remain the fastest-growing segment. The market is mainly driving by increasing investment on compute heavy AI enabled advanced and expensive GPUs and CPUs within DC and a major portion of the market is replacement / refresh network and IT equipment. Data centre networks and IT equipment are the backbone of modern digital infrastructure, supporting everything from cloud computing to AI applications. The growing demand for data-driven services, cloud migration, AI, and IoT connectivity are key growth drivers, fuelling the need for high-speed, scalable networks and robust IT hardware. Advances in software-defined networking (SDN), edge computing, and energy-efficient technologies are also accelerating this growth. As data volumes soar, data centres require cutting-edge CPUs & GPUs, high-density servers, storage solutions, and advanced networking equipment to ensure speed, reliability, and scalability. This evolving landscape demands continuous innovation to meet the ever-increasing performance driving huge investment on computational heavy, highly advanced, and expensive next generation GPUs, CPUs, and supporting infrastructure.

The global data center power infrastructure market was valued at US $15 Bn. Data centre power equipment, including PDUs (Power Distribution Units), switchgears, generators, and UPS (Uninterruptible Power Supplies), are critical for ensuring reliable, efficient, and uninterrupted power delivery. The rapid growth of cloud computing, big data analytics, and AI-driven applications are key growth drivers, increasing the demand for resilient power solutions to support 24/7 operations. Additionally, the push for energy efficiency and sustainability has led to innovations in advanced UPS systems and smart PDUs that optimize power usage. The rise of edge computing and hyperscale data centres further drives the need for scalable, high-capacity power equipment capable of handling dynamic workloads while minimizing downtime and energy costs. A typical investment on power infrastructure could cost in between US $1.5 to $2.5 Million per MW IT Load within a data centre

Cooling Infrastructure: With the emergence of generative & specialized AI and machine learning place substantial demands on computing resources. This requires specialized high-density semiconductors like GPUs, which in turn generate a lot of heat, driving higher rack densities necessitating more advanced cooling infrastructure in data centers, driving investment in advanced liquid cooling direct to chip and immersion cooling technologies. Liquid cooling offers superior thermal management, lower energy consumption, and the ability to support high-density deployments, making it a key technology for future-proofing data center operations in an era of exponential data growth.

Optimizing energy efficiency in data center cooling is crucial for reducing operational costs and minimizing environmental impact of the data centers. Power Usage Effectiveness (PUE) serves as a key metric in this regard, calculated by dividing the total energy consumed by the data center facility by the energy used specifically by the IT equipment. A lower PUE value indicates a more energy-efficient data center, with an ideal PUE being 1.0, where all energy is used for IT equipment. Another important metric, particularly for sustainability, is Water Usage Effectiveness (WUE), which measures the efficiency of a data center’s water usage by comparing the annual water consumption to the energy consumed by the IT equipment.

cooling infrastructure was valued in between US $10 to $11 Billion in 2024, mainly driven by growing adoption of advanced liquid cooling technology.

By Solution: Market Insights

Solution segment accounted for roughly 70% share, followed by installation, design & engineering, project management & facility engineering, and core & shell with remaining share in 2024. Data center design, engineering, and construction are pivotal in creating efficient, scalable, and resilient facilities to meet the growing demands of the digital economy. The focus on sustainability and green building standards is pushing for innovative designs that minimize environmental impact. Advances in modular construction, prefabricated data center components, and smart building technologies are transforming how data centers are designed and built, enabling faster deployment, cost efficiency, and greater operational flexibility to adapt to evolving technological needs.

By Data Center Type: Market Insights

Colocation deployments in terms of GW of IT load was the highest in 2024 accounted for at least 50% share, while in terms of CAPEX in Hyperscaler accounted for approx. 40% share and is likely to grow faster than Colocation and Enterprise based data centers during the forecast period.

By Workload: Market Insights

AI based workloads within the data center are likely to grow at more than 25% CAGR, while the traditional data center installation to grow at 8% CAGR during the forecast period. An AI-enabled data centre can easily cost 2X more than a conventional one. In 2035, AI based data centers to account for more than 50% share of the global Data Centre deployment, worldwide.

By Offering: Market Insights

Hardware accounted for more than 50% share of the global data center infrastructure CAPEX, followed by Software and Services together accounted for the remaining share in 2024.

By End Use: Market Insights

BFSI, IT & Telecom, Media & Entertainment Research & Academia, and Cryptocurrency mining together accounted for 60% of all investment in the data center infrastructure market, globally. Medical & Healthcare end use application is also gaining traction.

By Installation: Market Insights

First Fit / New Installation accounted for approx. 60% Share of the market, while replacement / refresh spending accounted for approx. 40% share in 2024. Data center owners / operators, such as AWS, Google, META, Microsoft typically replaces the network & IT equipment in every 5 to 6 years, while power infrastructure replaces after 10 years.

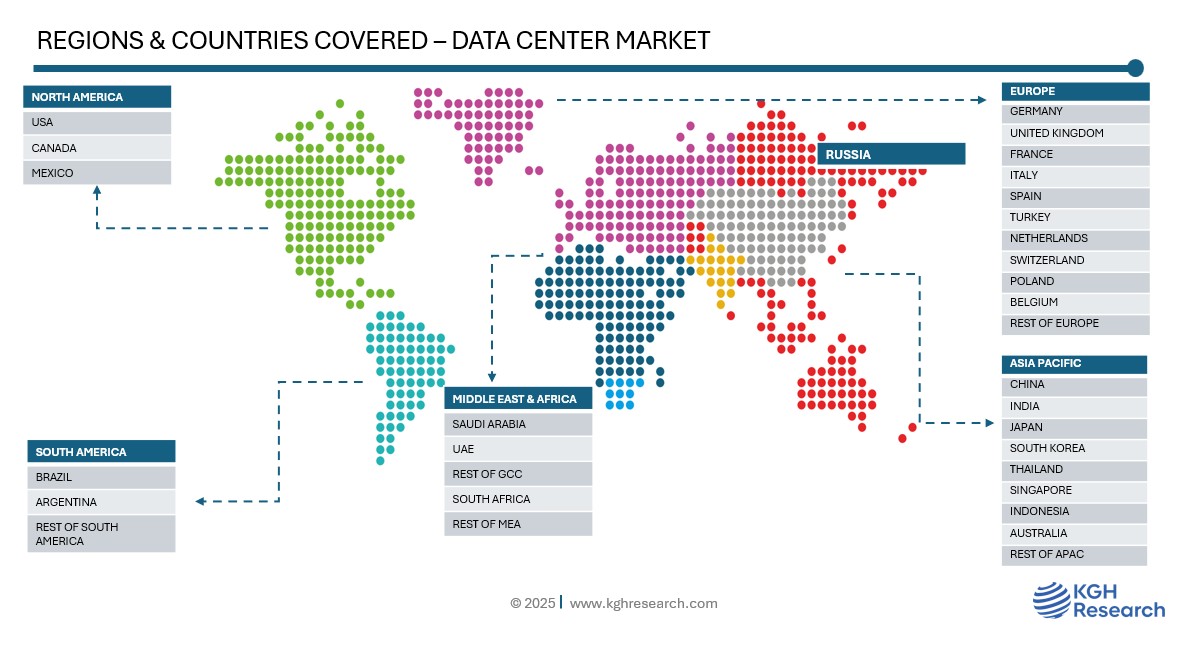

Regional: Market Insights

North America holds the dominant position with approx. 50% share of the global CAPEX on data center infrastructure, followed by APAC with 30% share, and EMEA & South America together with 20% share.

- USA is the world’s largest hub for active data centers with more than 5000 operational data center with a cumulative installed capacity of XX GW, followed by Germany with 500+ operational DC

- India is the fastest growing country in data center installation

- North America continues to lead the global data center market accounted for almost 50% share of the new installations, with the U.S. and Canada driving significant investments. The region is projected to maintain a compound annual growth rate (CAGR) of approx. 10% from 2025 to 2035. Major hyperscale operators like Amazon Web Services, Microsoft, and Google are expanding their infrastructure to meet the growing demand for cloud services and AI applications.

- Europe is expanding steadily, with a focus on energy efficiency and sustainability in data centre architecture. More money is being invested in colocation and modular data centres in nations like the UK, the Netherlands, and Germany. Data centre development is being influenced by the region’s emphasis on green technologies and adherence to strict data protection laws.

- Asia Pacific is also experiencing significant growth, and is likely to become the second largest region after North America in terms of cumulative installations during the forecast period. The data center boom in Asia Pacific is being fuelled by how fast the region is going digital. With more people online than anywhere else in the world, especially in countries like China, India, and across Southeast Asia, there’s a massive need for reliable, high-speed infrastructure. Cloud adoption is skyrocketing as businesses modernize, and tech giants like AWS, Google, and Alibaba are racing to build out their networks. At the same time, 5G is rolling out across places like Japan and South Korea, pushing the need for faster, more localized data processing—AI workloads, edge computing. Governments are also playing a big role, with initiatives like Digital India and smart city projects across the region making it easier for companies to invest and build. Even countries like Malaysia and Indonesia are stepping up, offering new opportunities as demand spreads beyond the traditional hubs like Singapore and Hong Kong.

- The Middle East & Africa is quickly becoming a hotspot for data center growth, thanks to a wave of digital transformation sweeping across the region. Countries like the UAE, Saudi Arabia, and South Africa are leading the charge, investing heavily in cloud infrastructure, smart cities, and AI technologies. Global tech giants and local players alike are setting up data centers to meet the rising demand for digital services, driven by everything from online banking and e-commerce to video streaming and government digitalization efforts. What’s fuelling this momentum even more is strong government backing—think Vision 2030 in Saudi Arabia and the UAE’s digital economy strategies—plus improved connectivity through new undersea cables and better fiber networks. As internet penetration grows and more businesses move to the cloud, the region is positioning itself as a serious player in the global data center landscape.

Competition: Data Center Market

- In Network & IT Equipment: In Server segment, OEM segment accounted for 60% share, while the ODM accounted for 40% share. Dell, HPE, SuperMicro, Lenovo, IBM, and H3C together accounted for approx. 40% share of the OEM segment, followed by others with 20% share.

- In the Networking equipment segment, Cisco, Huawei, and Arista together accounted for approx. 60% share.

- In the power infrastructure, in UPS market, top 5 namely, Schneider, Vertiv, Eaton, ABB, and Siemens together accounted for approx. 75% share, while in the Generators market, Caterpillar & Caterpillar together accounted for 70% share.

- In the thermal equipment, Vertiv & Johnson, Stulz, and Schneider are the world largest companies.

- The DC Engineering & Construction market is highly fragmented with top 5 to 7 companies together accounted for approx. 30% share.

DATA CENTER MARKET SNAPSHOT | |

Market size in 2025 | US$ 370 Billion |

Market forecast in 2032 | US$ 1050 Billion |

Compound Annual Growth Rate (2025-2032) | 10.0% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Major Drivers & Trends | Growing Data Center Market, Increasing Deployments of Generative AI and Specialized AI based Data Centers |

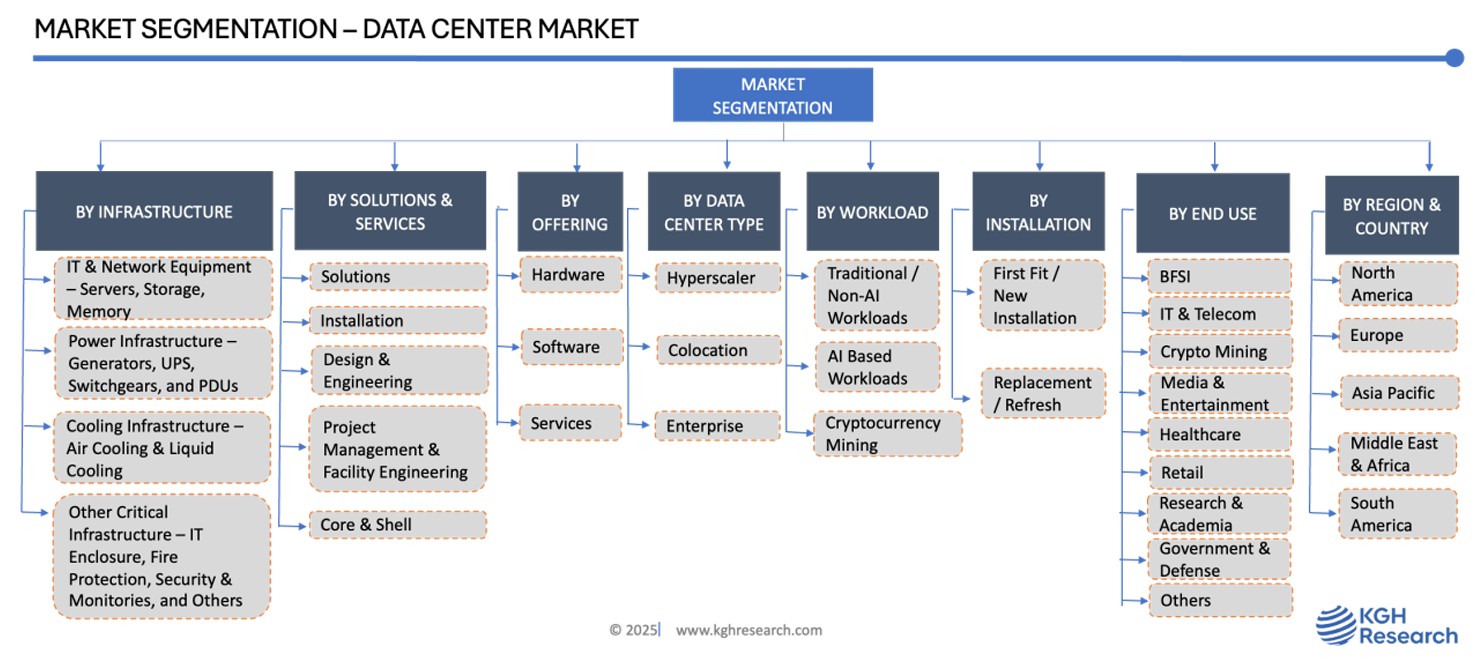

Segments Covered | By Infrastructure Type, By Data Center Type, by Component & Services, by Offering, by Workload, by Installation, by End Use, by Region & Countries |

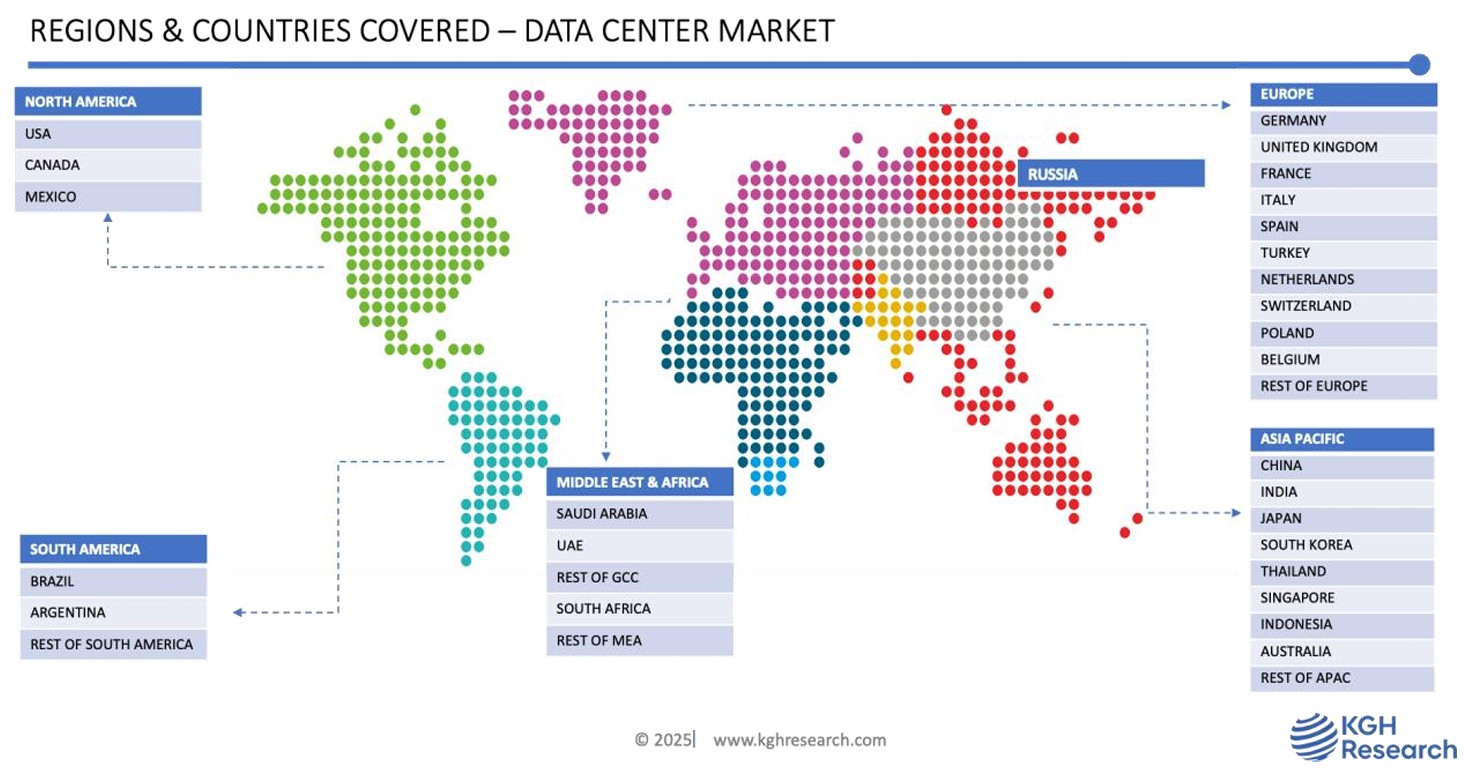

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, France, Turkey, Russia, Rest of Europe, China, India, Japan, Indonesia, South Korea, Indonesia, Rest of APAC, South Africa, UAE, Saudi Arabia, Brazil, Chile, Rest of South America |

Companies Profiled (40+) | Nvidia, Intel, AMD, Ampere, Huawei, Cisco, Arista, Lenovo, Dell, HPE, SuperMicro, IBM, H3C, IEIT Systems, Vertiv, Schneider Electric, Rolls Royce, Johnson Control, Trane, Diakin, Carrier, Modine, ZutaCore, Stulz, Accelcius, EBARA, ICETOPE, NVENT, SPX, Kelvion, Cummin, ABB, Legrand, Eaton, Caterpillar, Siemens. EPCs – Turner, Flour, Burns & Mcdonnell, HITT, Holder, Jacob, AECOM, WSP, and Many More |