Wearable Healthcare Device Market (2022 - 2032)

WEARABLE HEALTHCARE DEVICES MARKET SIZE & SHARE BY PRODUCT TYPE (TRACKERS, SMARTWATCHES, PATCHES, SMART CLOTHING, OTHERS), BY GRADE (CONSUMER, CLINICAL), BY DISTRIBUTION CHANNEL (PHARMACIES, ONLINE, HYPERMARKET), BY DEVICE TYPE (DIAGNOSTIC & MONITORING DEVICES, THERAPEUTIC DEVICES) APPLICATION (GENERAL HEALTH, REMOTE PATIENT MONITORING, HOME HEALTHCARE) AND BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: M&H5003-0502 | Number of Pages: 240 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: AUGUST 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

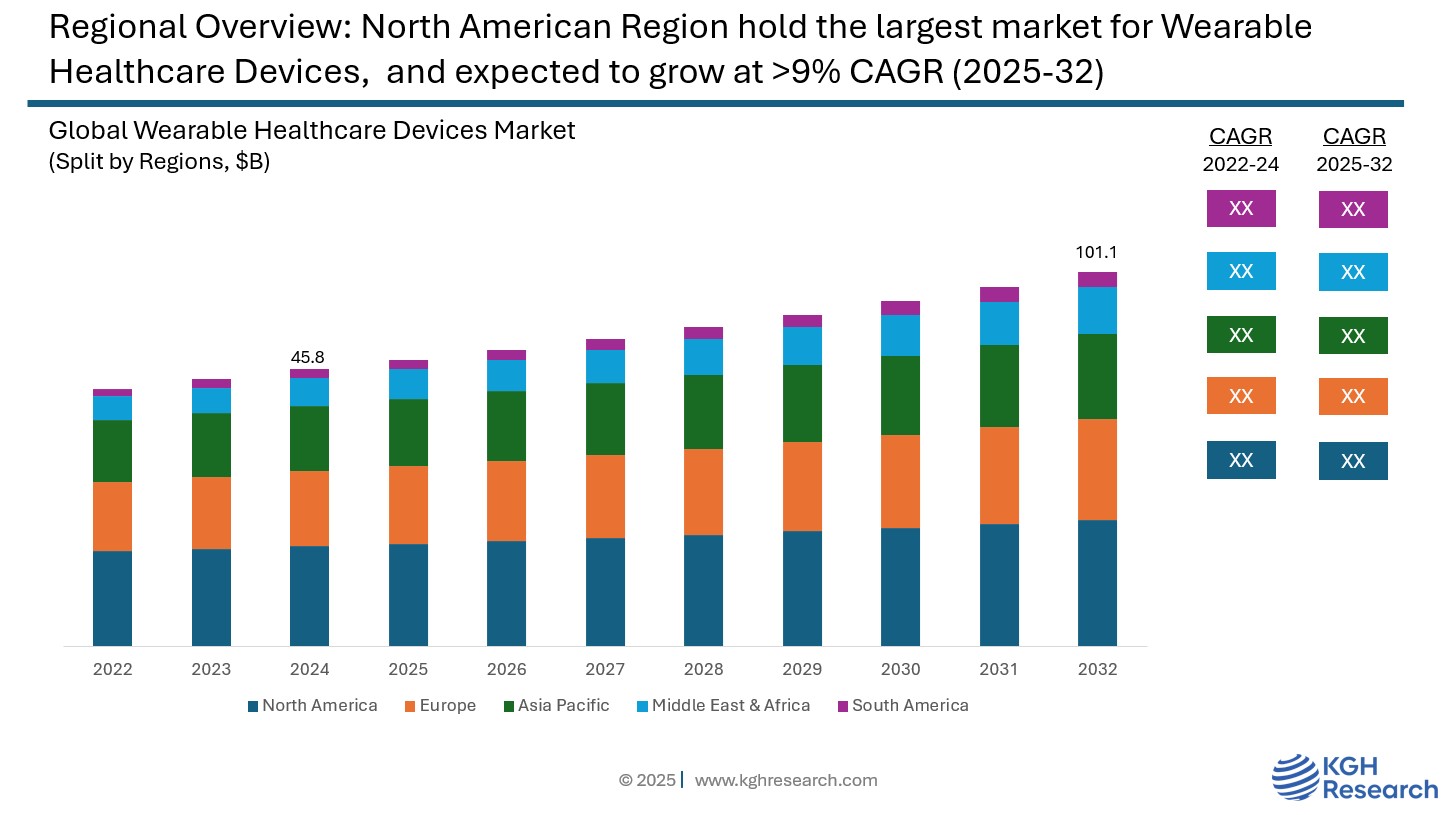

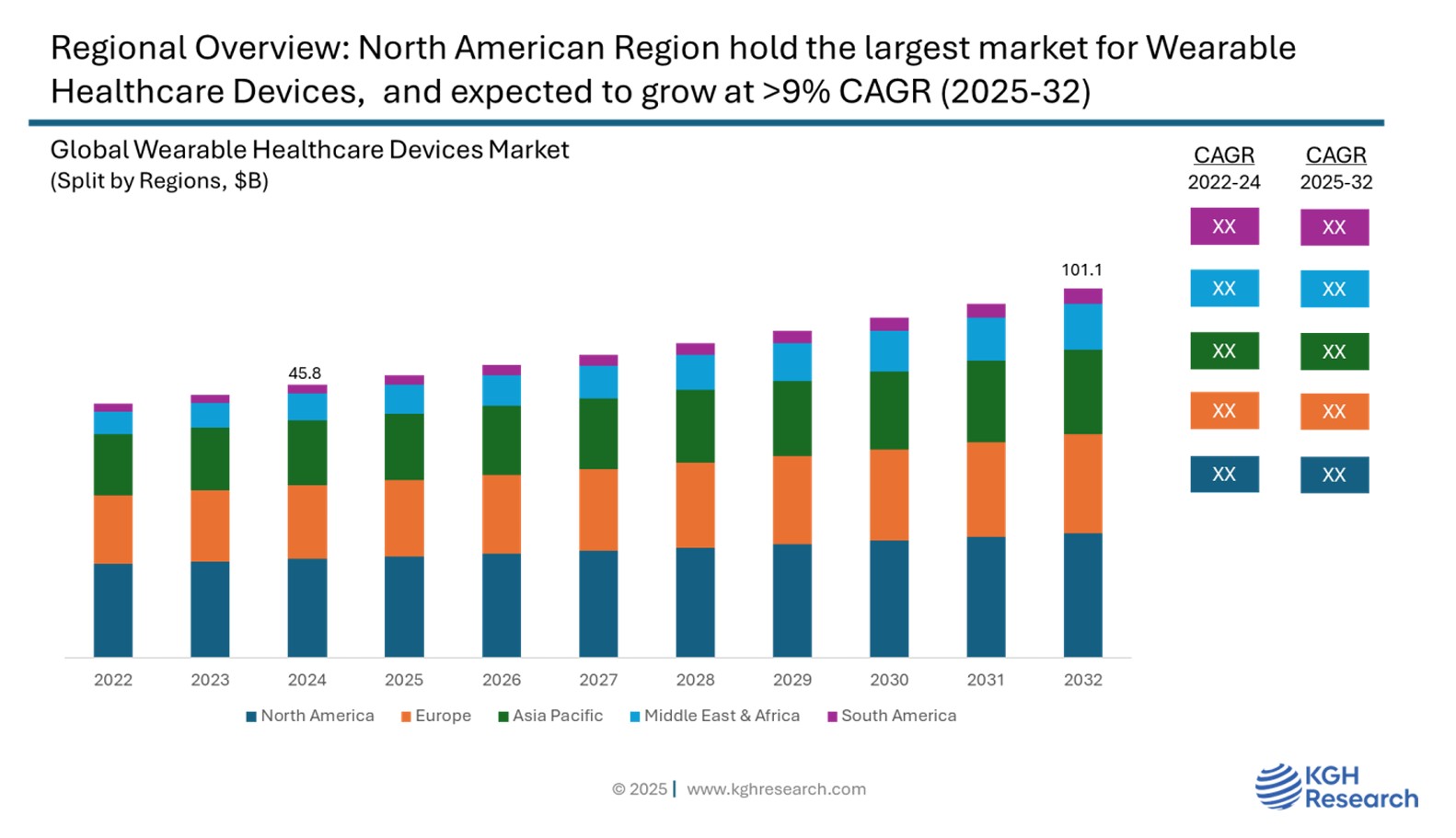

Market Overview: The global wearable healthcare devices market was valued at approximately USD 45.8 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 10.4% from 2025 to 2032 to become a US $100 billion opportunity by 2032. The market is fueled by several important trends, as chronic conditions like diabetes, heart disease, and obesity become more common, there’s a greater need for continuous health monitoring. People are also becoming more proactive about their personal health and fitness, which is driving interest in wearable technology. The integration of advanced technologies, such as artificial intelligence, IoTs, and cloud connectivity enables continuous data tracking, early diagnosis, and remote patient monitoring, which are highly valuable in healthcare landscape. Moreover, the ageing global population and rising medical costs are prompting healthcare providers and individuals to shift toward preventive care and home-based monitoring solutions, further fuelling market growth. Governments and insurers are also increasingly supporting digital health initiatives, including the use of wearables, to reduce hospital admissions and improve long-term patient outcomes.

MARKET DYNAMIC

GROWTH DRIVERS:

- Rising prevalence of chronic diseases is pushing demand for continuous health monitoring

- Consumers are becoming more health-conscious, driving adoption of fitness trackers and smartwatches.

- Rise in remote patient monitoring & telehealth

- Government policies promoting digital healthcare and wellness monitoring are boosting the market

- Growing ageing population worldwide increases the need for health-monitoring solutions.

NEW GROWTH OPPORTUNITIES:

- Integration with AI and Big Data Analytics

- Expanding Telemedicine Ecosystem

- Rapid urbanization and rising income levels in Asia-Pacific, Latin America, and Africa open new growth avenues

- Chronic disease management programs

- Workplace wellness & insurance incentives

MARKET RESTRAINTS:

- Advanced wearable healthcare devices can be expensive

- Handling sensitive health data raises privacy risks, which may deter some users

- Limited clinical validation

- Short battery life and sensor accuracy issues in some devices hinder long-term use.

GROWTH HURDLES:

- Stringent regulatory approvals and compliance issues may delay product launches

- Competition & market saturation

- Lack of standardization

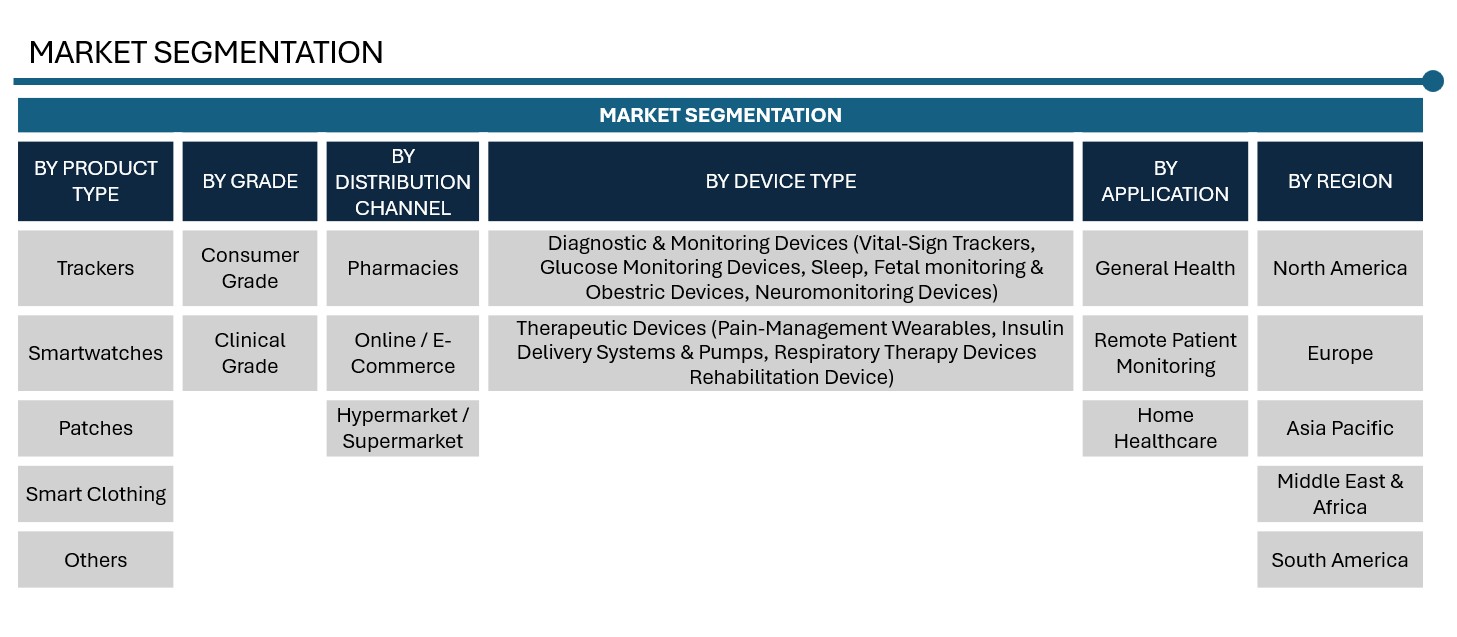

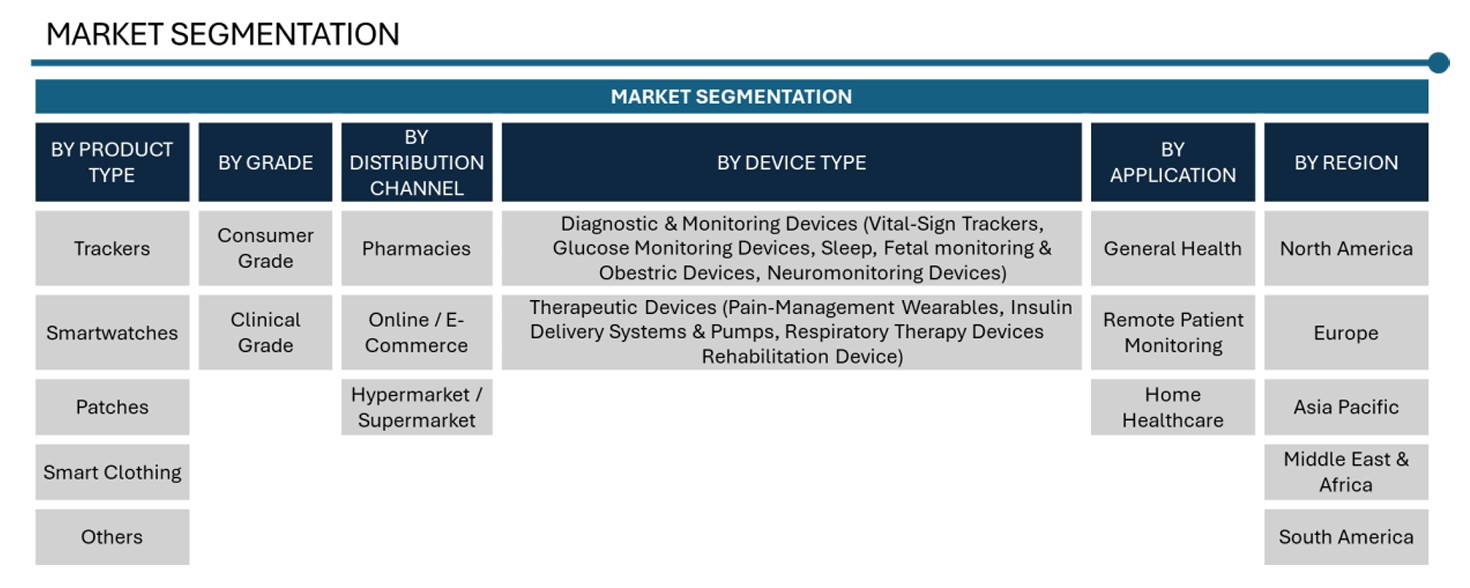

Product Type: Market Insights

Smartwatches are the single most dominant and fastest growing market segment in wearable healthcare devices for 2024 – 2025. Smartwatches dominate the market largely because they combine a wide array of health monitoring capabilities, such as tracking heart rate, ECG, blood oxygen, sleep quality, and daily activity with convenient lifestyle functions like receiving notifications and calls. This versatility has made them indispensable for both individuals focused on their personal wellness and professionals seeking clinical-grade monitoring solutions. They outpace trackers, patches, and smart clothing, owing to multifunctionality, ecosystem integration, continual innovation, and broad adoption in both consumer and medical contexts. The market for patches and smart clothing is rapidly evolving, with high innovation potential and expected future growth as these technologies mature and clinical acceptance widens.

Trackers and fitness bands hold a second largest share of the wearable healthcare devices market, especially for entry-level health monitoring due to their affordability and straightforward design. Their popularity is pronounced in emerging regions where cost-effectiveness is essential. In contrast, patches and smart clothing, though currently representing a small portion of the market, are experiencing rapid growth. Patches are particularly valued in clinical environments for continuous monitoring, while smart clothing leverages embedded sensors for advanced health data collection; both are expected to expand significantly as technological validation and user trust increase. Meanwhile, smart rings and hearables offer discreet, round-the-clock tracking of sophisticated metrics like sleep and heart rate variability, and although their market presence is still limited, projections indicate substantial growth in the coming years.

Grade: Market Insights

The global wearable healthcare devices market is segmented into consumer-grade and clinical-grade devices based on their intended use and regulatory classification. Consumer-grade devices held the largest market share primarily because of their broad accessibility, affordable pricing, and growing demand for self-health management. People are increasingly using these devices to track their fitness, prevent health issues, and maintain a healthier lifestyle without the need for medical supervision. Moreover, the post-pandemic shift toward preventive health and wellness has significantly increased their adoption. Tech companies like Apple, Fitbit, and others continue to drive this segment with constant innovation and user-friendly designs, further fuelling market dominance.

Application: Market Insights

By application, the general health segment holds the dominant share of the global wearable healthcare devices market. This dominance is largely driven by the growing public awareness around maintaining a healthy lifestyle and the increasing adoption of fitness-focused wearables. Devices that track daily activity levels, heart rate, sleep patterns, calorie absorption and expenditure, and stress levels have become mainstream tools for individuals aiming to improve or maintain their overall well-being. The integration of these wearables with mobile apps and cloud-based platforms allows users to monitor their health trends over time, further enhancing user engagement. As a result, the general health segment continues to lead the market in terms of both consumer interest and revenue contribution.

Distribution Channel: Market Insights

In terms of distribution channels, Pharmacies are the leading segment in the global wearable healthcare devices market. Whether it’s a retail chain or a hospital-linked outlet, pharmacies are seen as reliable and convenient places for people to buy health-related products. Their ability to provide in-person guidance, suggest suitable devices, and sometimes even offer insurance-supported purchases makes them a popular choice for consumers looking to invest in wearable healthcare technology. The online sales channel currently accounts for the second largest market and is rapidly growing.

Device Type: Market Insights

By device type, the wearable healthcare devices market is categorized into diagnostic & monitoring devices and therapeutic devices. Diagnostic and monitoring devices are used to track a person’s health status and detect any changes or issues. These include devices like fitness trackers, heart rate monitors, blood pressure monitors, glucose monitors, and wearable ECGs. They help in continuously monitoring vital signs and identifying potential health problems early. Therapeutic devices are designed to actively help in treating medical conditions. These include devices like wearable insulin pumps, pain management devices, and rehabilitation wearables that support movement or therapy. They play a direct role in managing or improving a patient’s health condition.

Regional: Market Insights

North America accounts for the largest share of the global wearable healthcare devices market, with the United States acting as the primary growth engine. This dominance is supported by several factors, starting with the region’s advanced digital and healthcare infrastructure. The U.S. has seen a rapid adoption of wearable technologies for health and wellness, driven by a tech-savvy and health-conscious population. Consumers increasingly rely on smartwatches, fitness trackers, wearable ECG monitors, and glucose monitors to manage personal health, track fitness metrics, and support chronic disease management. The high prevalence of chronic conditions such as diabetes, hypertension, heart disease, and obesity in the U.S. is a major driver for the adoption of diagnostic and therapeutic wearables. These devices help patients monitor vital signs in real time and enable physicians to make data-driven clinical decisions remotely. Post-pandemic, there has also been a significant rise in demand for remote patient monitoring, telemedicine, and home-based care further accelerating the integration of wearable devices into everyday healthcare.

Government support and regulatory flexibility have also played a key role. The U.S. Food and Drug Administration (FDA) has fast-tracked the approval of various medical-grade wearables and continues to support innovation in this space. Moreover, expanding insurance reimbursement for remote monitoring services encourages both healthcare providers and patients to adopt these devices.

In addition, the U.S. is home to major global players such as Apple Inc., Fitbit (owned by Google), Abbott Laboratories, Whoop, and Dexcom. These companies consistently invest in research and development, driving innovation in device accuracy, design, and usability. Strategic partnerships with healthcare systems, tech firms, and insurers further expand the reach and impact of wearable healthcare technologies. The United States leads the North American wearable healthcare devices market due to its robust healthcare ecosystem, high disease burden, advanced technology landscape, favorable regulatory framework, and strong presence of global market leaders. These combined factors make the region a hub for innovation and large-scale adoption of wearable health solutions.

Competition: Wearable Healthcare Devices

The Wearable Healthcare Devices market is highly competitive, with key players focusing on innovation, product efficiency, and strategic partnerships to strengthen their market position. Major companies Apple Inc., Koninklijke Philips N.V., Fitbit, Abbott, Dexcom, Whoop. These players are investing in R&D to develop advanced devices tailored for general health, remote patient monitoring, home healthcare applications, driving ongoing competition and technological advancement in the market.

Apple Inc., Koninklijke Philips N.V., Fitbit, Abbott, Dexcom, are among the leading companies active in the market.

Apple Inc. stands out as a key player in the global wearable healthcare devices market, thanks to its widely popular Apple Watch. The device combines sleek design with powerful health features like heart rate monitoring, ECG, blood oxygen tracking, sleep analysis, and fall detection. Its smooth integration with the iPhone and the broader Apple ecosystem enhances the overall user experience, helping Apple lead the consumer-focused segment of health wearables. The company’s strong emphasis on preventive health has appealed to a broad range of users from fitness lovers to those managing chronic health issues. By regularly updating its software and innovating its hardware, Apple has transformed the Apple Watch into more than just a smartwatch, it’s a trusted health companion. Through platforms like HealthKit and ResearchKit, Apple is also playing an active role in advancing digital health and personalized care, reinforcing its position as a frontrunner in wearable health technology.

Fitbit Inc., now part of Alphabet Inc., is a well-recognized name in the wearable healthcare devices market, known for creating easy-to-use and affordable fitness trackers. Its product lineup—including the Fitbit Charge, Versa, Inspire, and Sense series—tracks essential health metrics like heart rate, sleep quality, activity levels, stress, and blood oxygen levels. Fitbit has earned a strong following by helping users stay engaged with their health and wellness routines, making it a go-to brand for both casual users and fitness-focused individuals. The combination of user-friendly design, long battery life, and affordability has made its devices widely popular. Since joining Alphabet, Fitbit has deepened its integration with Android and Google’s health ecosystem, expanding its digital health capabilities. Its premium subscription service, Fitbit Premium, further enhances the user experience by offering personalized insights, coaching, and advanced health analytics, cementing Fitbit’s role as a leader in connected health and wellness.

Valeo SA, based in Paris, France, is a major global supplier for the automotive industry and plays an important role in the EV battery cooling plate market. The company focuses on sustainable mobility and vehicle electrification. Valeo has created effective thermal management systems that are vital for the performance and safety of electric vehicles. They provide high-efficiency, liquid-based cooling solutions that help manage battery temperature, improve charging efficiency, and extend the battery’s lifespan. These systems are designed to be compact, lightweight, and suitable for different EV battery setups, suiting changing vehicle designs. Valeo continues to invest in research and development and builds strategic partnerships with leading OEMs. This positions the company as a technology leader in the EV thermal systems sector. Operating in major global markets, Valeo stays at the leading edge of battery cooling technologies, supporting the quick shift to electric mobility.

MAHLE GmbH, based in Stuttgart, Germany, is a prominent global automotive supplier and a key player in the EV battery cooling plate market. With decades of experience in thermal management and powertrain systems, MAHLE has expanded its offerings to meet the rising demand for electric vehicles. The company develops and supplies battery cooling plates and thermal management solutions that ensure optimal battery performance, safety, and longevity. MAHLE’s cooling plates efficiently dissipate heat, even during high-load or fast-charging situations and are tailored for next-generation EV platforms. Its solutions emphasize lightweight materials, compact design, and high thermal conductivity to enhance overall vehicle efficiency. With a solid R&D foundation and strong partnerships with global OEMs, MAHLE continues to innovate in battery thermal management and strengthens its position as a trusted supplier in the worldwide EV components market.

WEARABLE HEALTHCARE DEVICES MARKET SNAPSHOT | |

Market size in 2024 | USD 45.8 Billion |

Market forecast in 2032 | USD 101.1 Billion |

Compound Annual Growth Rate (2025-2032) | 10.4% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Segments Covered | Product Type, Grade, Distribution Channel, Application, Device Type |

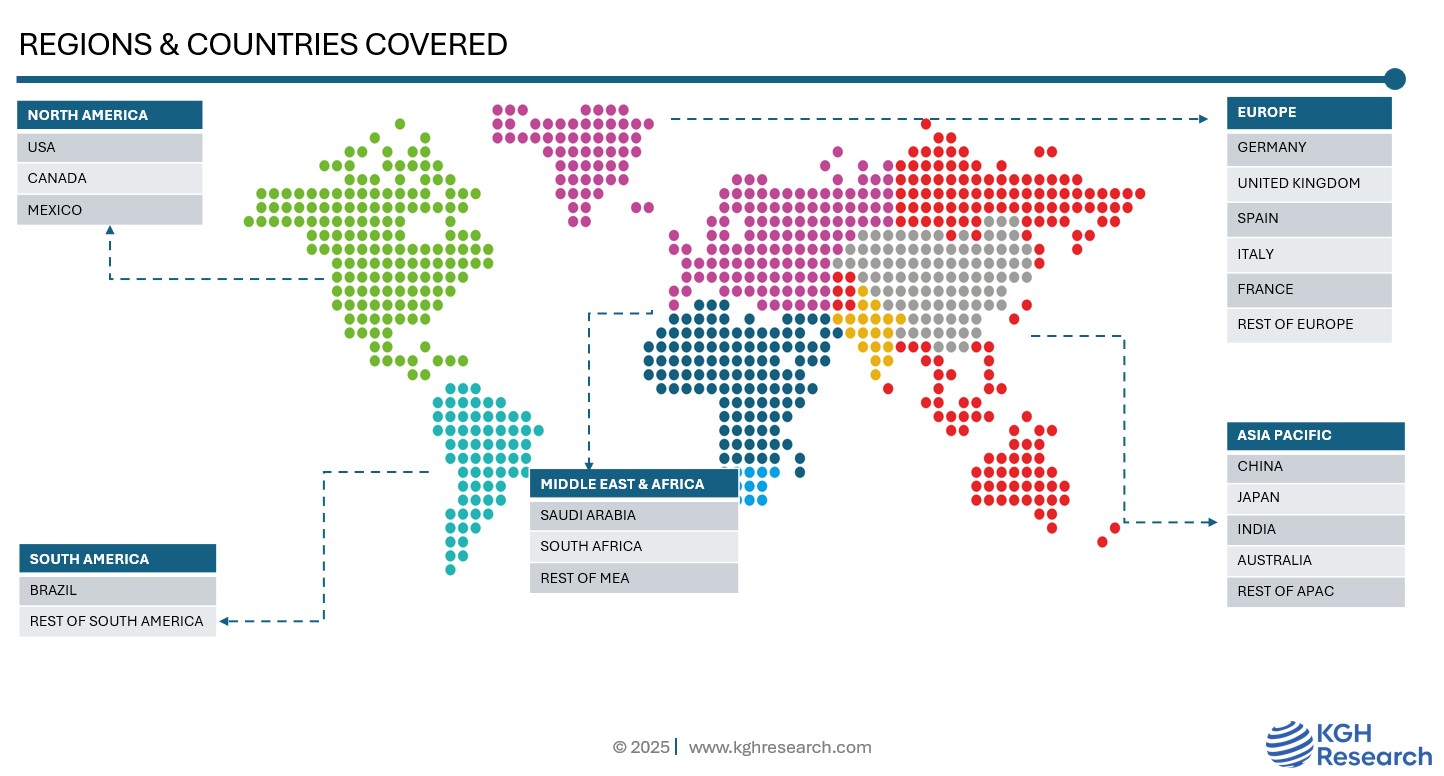

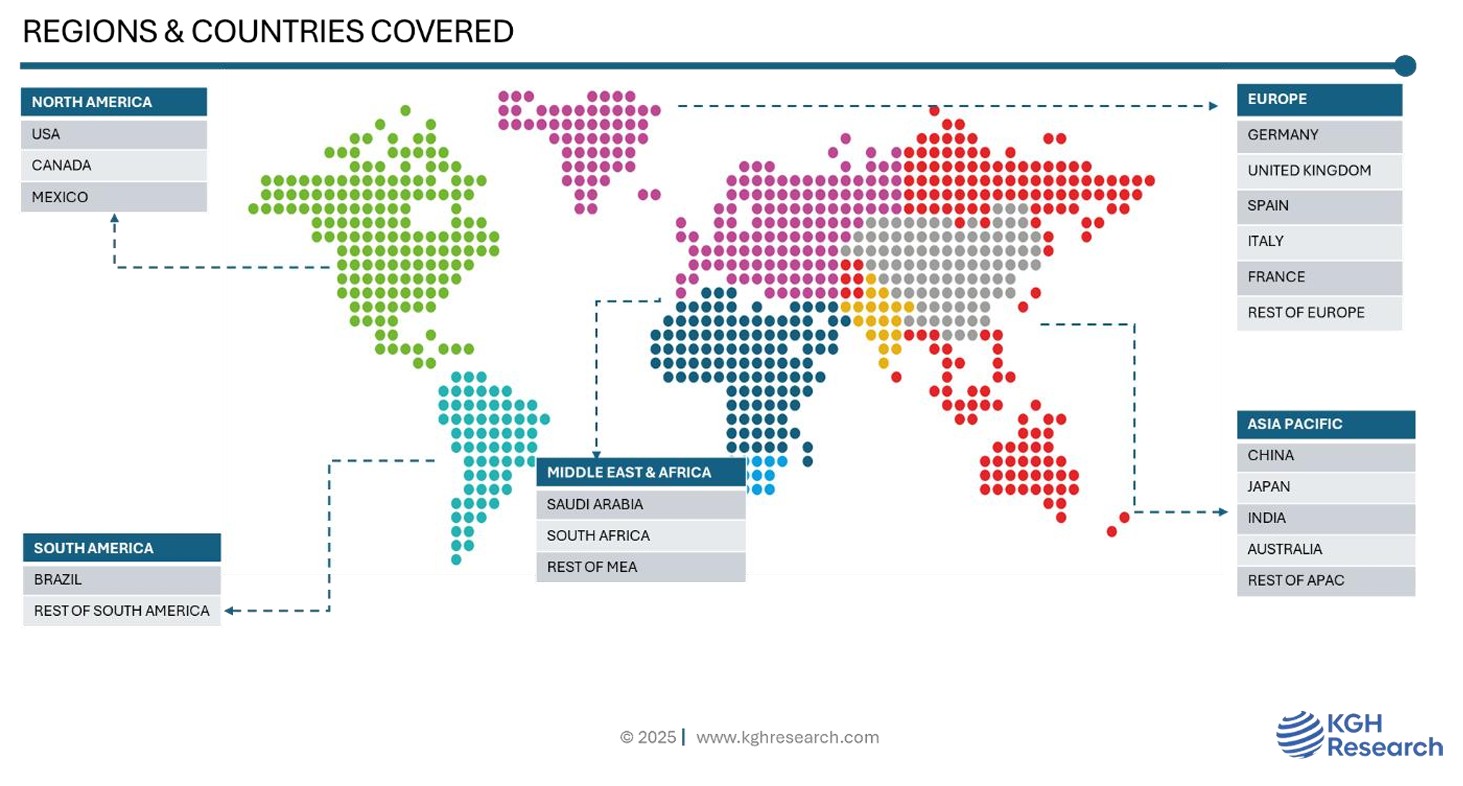

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, France, Spain, China, Japan, India, Australia, South Africa, Saudi Arabia, Brazil |

Companies Profiled (20+) | APPLE INC., FITBIT INC., GARMIN LTD., MEDTRONIC PLC, GE HEALTHCARE, BOSTON SCIENTIFIC CORPORATION, BIOBEAT, DEXCOM INC., WHOOP, ABBOTT LABORATORIES, KONINKLIJKE PHILIPS N.V., BIOTELEMETRY INC. (PHILIPS), IHEALTH LABS INC., GENTAG, INC., OXITONE MEDICAL, CONTEC MEDICAL, VITALCONNECT, SAMSUNG ELECTRONICS CO. LTD., OURA HEALTH LTD., WITHINGS, BIOTRICITY, TEN3T HEALTHCARE, NONIN MEDICAL, INC., EMPATICA, MASIMO, IRHYTHM TECHNOLOGIES. |