Anti Drone Market (2022 - 2032)

ANTI DRONE MARKET SIZE & SHARE BY SYSTEM TYPE (ELECTRONIC, LASER, KINETIC, HYBRID), BY APLICATION (DETECTION & DISRUPTION, DETECTION), BY RANGE (5KM), BY PLATFORM (GROUND BASED, UAV BASED, HANDHELD), BY COMPONENT (HARDWARE, SOFTWARE), BY END USE (MILITARY & DÉFENSE, HOMELAND SECURITY, COMMERCIAL), BY FREQUENCY BAND, AND BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: A&D1002-0301 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: JULY 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

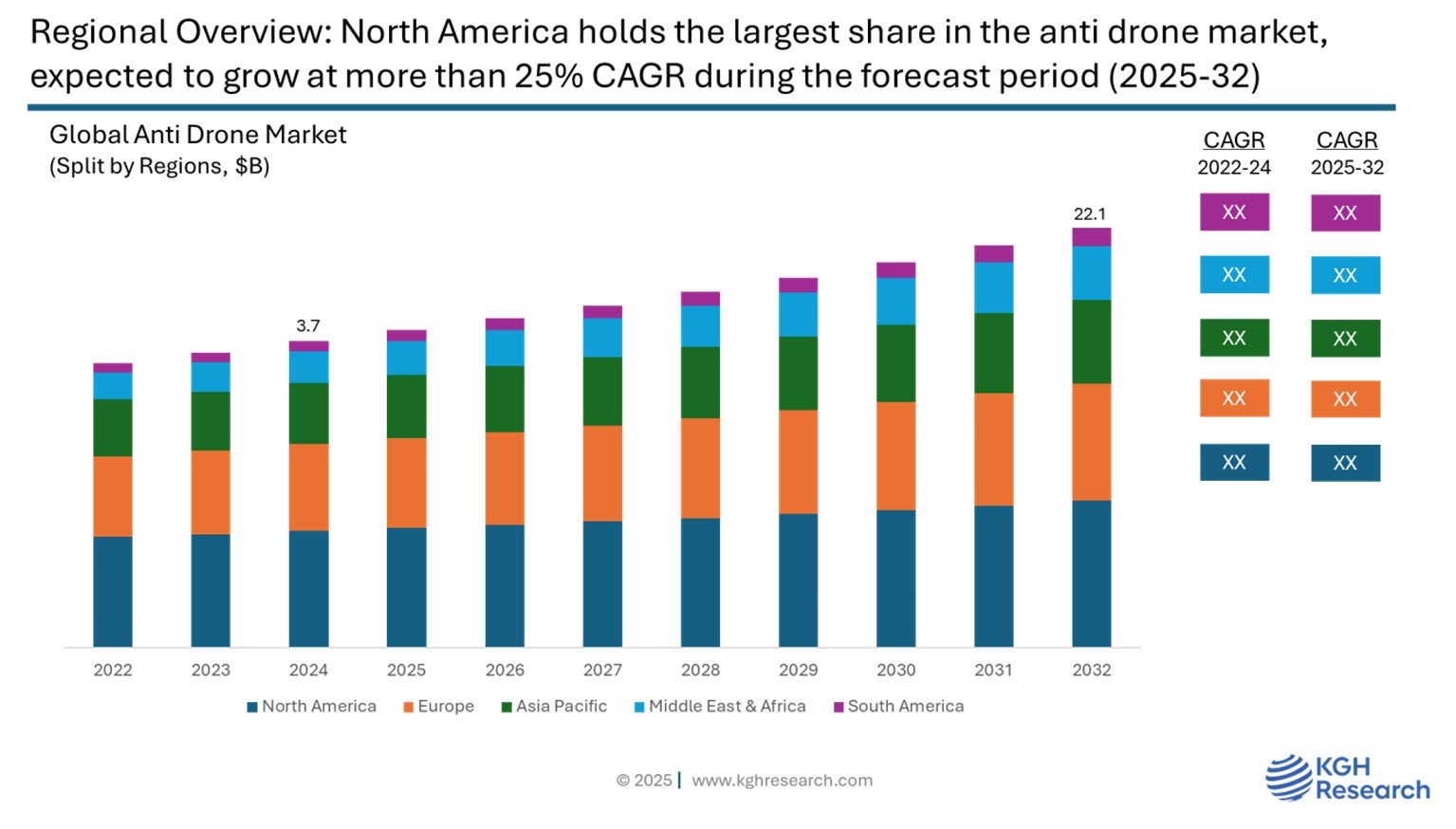

Market Overview: The global anti drone market was valued at approximately USD 3.7 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of >25% from 2025 to 2032 to become US $22 billion opportunity by 2032. The market is primarily driven by the growing threat from unauthorized and harmful use of drones for cross-border terrorism, violation of military and commercial airspaces. As drones become easier and cheaper to obtain and operate, their misuse for surveillance, smuggling, espionage, and even potential terror threats has increased. This has led governments and defense organizations around the world to invest heavily in improved counter-drone technologies for border security, airport protection, and critical infrastructure defense.

MARKET DYNAMIC

GROWTH DRIVERS:

- Increasing incidents of unauthorized drone intrusions over sensitive areas such as military bases, airports, and critical infrastructures, etc

- Heavy investment by government, defence and homeland security agencies to counter growing drone/UAV related threats

- Counter-terrorism & smuggling prevention

- Increased drone adoption

NEW GROWTH OPPORTUNITIES:

- Growing need for anti-drone systems in critical civilian infrastructure such as airports, stadiums, monuments of historical importance, public gatherings, and other proceeding

- Integration of AI/ML, multi-sensor arrays (Radar, RF, optical), and scalable ground-based platforms enhance effectiveness

- Rising demand in emerging economies

MARKET RESTRAINTS:

- High system costs

- Regulatory uncertainty

GROWTH HURDLES:

- Rapid advancement in drone stealth technology, swarm tactics, and AI navigation may outpace existing anti-drone systems.

- Cybersecurity risks

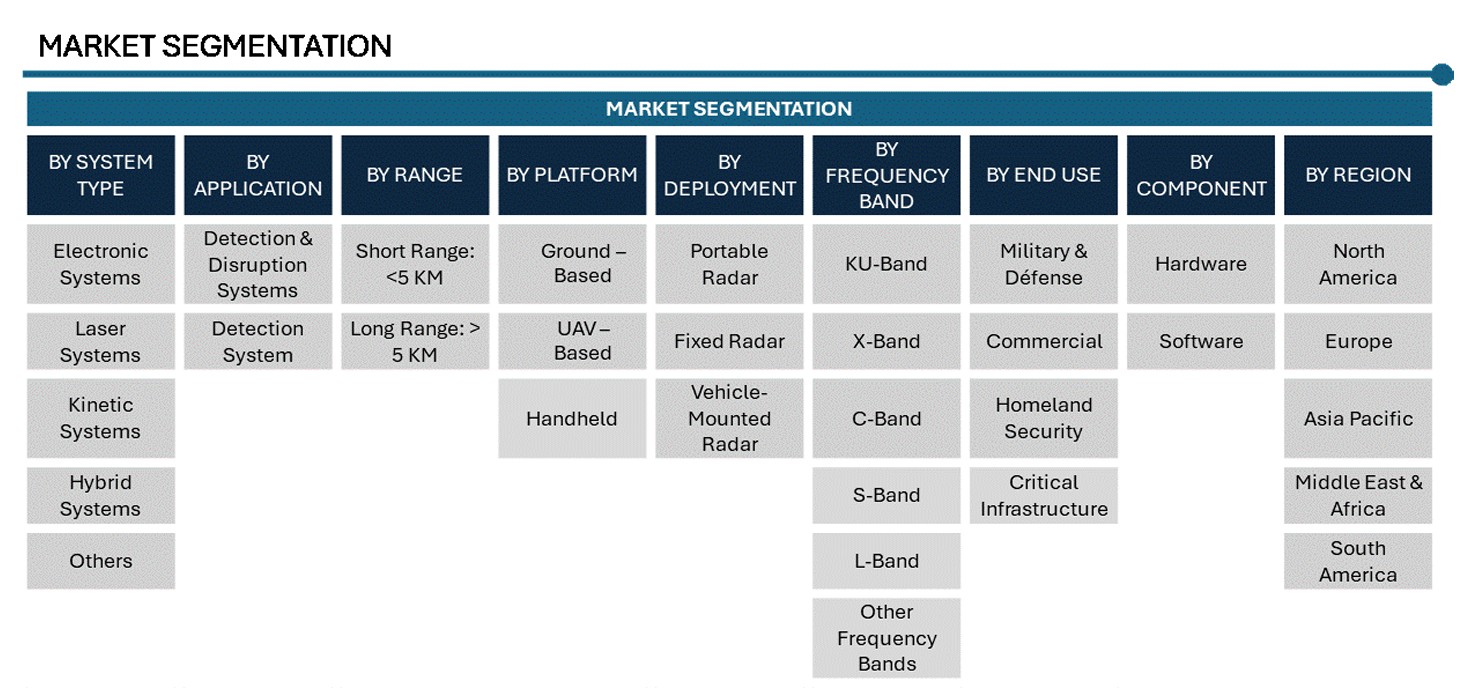

System Type: Market Insights

By system type, the global anti-drone market is divided into Electronic, Laser, Kinetic, and Hybrid systems. Electronic systems include technologies like radio frequency (RF) jammers, GNSS spoofers, and electromagnetic pulse devices that disable or disrupt drone communications and navigation without physical contact. Laser systems use directed energy weapons to destroy or disable drones’ mid-air with high precision. This makes them suitable for military use where permanent elimination is necessary. Kinetic systems involve physical methods for neutralizing drones, such as net guns, projectiles, or interceptor drones. They are often used in high-security zones or close-range situations. Hybrid systems combine two or more of these methods, like electronic disruption with kinetic interception, to create a layered defense strategy. Each system has distinct benefits based on the threat level, operating environment, and end-user needs. Currently, electronic and hybrid systems are seeing the highest adoption in defense and critical infrastructure sectors.

Application: Market Insights

By application, the global anti-drone market is segmented into detection systems and detection & disruption systems. Detection Systems are designed solely to identify, track, and monitor unauthorized drones using technologies such as radar, radio frequency analyzers, acoustic sensors, and electro-optical/infrared (EO/IR) cameras. These systems provide situational awareness and early warning but do not have the capability to neutralize or disable drones. Detection & Disruption Systems combine detection with active countermeasures to neutralize threats. These systems can disrupt drone operations through electronic jamming, GPS spoofing, or even kinetic and laser-based interdiction methods. Detection & disruption systems are preferred in high-security environments such as military bases, airports, and government facilities, where both monitoring and mitigation are critical. The growing need for comprehensive drone defense solutions is driving higher adoption of integrated detection and disruption systems across both defense and commercial sectors.

Platform: Market Insights

Based on platforms, the global anti-drone market is segmented into Ground-based, UAV-based, and Handheld systems. Among these, Ground-based systems hold the largest market share as they can integrate advanced radar, RF analysers, EO/IR sensors, and high-powered jammers to detect and neutralize drones over long ranges. While UAV-based and Handheld systems are growing in popularity especially for mobile operations and tactical use, Ground-based systems remain dominant due to their reliability, advanced capability, and broad application in defence and critical infrastructure security.

Component: Market Insights

By component, the global anti-drone market is segmented into Hardware and Software. Hardware holds a larger market share, as it forms the physical foundation of anti-drone systems, including radar, infrared and video surveillance systems, jammer, acoustic sensors, RF detectors, and others. These components are essential for detecting, tracking, and neutralizing drones in real time. The high cost and complexity of advanced hardware, particularly in military and critical infrastructure applications contribute significantly to overall market revenue. Software segment is gaining traction due to its role in data analysis, threat classification, decision-making automation, and system integration. AI- and machine learning-powered software enhances the accuracy of drone detection, reduces false alarms, and improves response times. While software is critical for system intelligence and user interface, hardware continues to dominate the market due to its indispensable role in delivering functional counter-drone capabilities.

End Use: Market Insights

By end use, the global anti-drone market is categorized into Military & Defense, Homeland Security, Commercial, and Others. Among these, the Military & Defense segment holds the largest share due to the rising threat of drones being used in warfare, surveillance, and attacks by state and non-state actors. Armed forces across the globe are increasingly investing in advanced counter drone technologies to protect troops, secure bases, and maintain airspace control, especially in conflict-prone regions. Homeland Security is another significant segment, driven by the need to safeguard national borders, government facilities, prisons, and critical infrastructure from unauthorized drone activities. Commercial end users, including airports, oil & gas facilities, stadiums, and data centers are adopting anti-drone systems to prevent espionage, smuggling, and disruptions caused by rogue drones.

Regional: Market Insights

North America is the largest market for anti-drone technology. This growth comes from high defense spending, advanced technological infrastructure, and rising concerns about security threats from unauthorized use of drones. The United States stands out in the region due to its major investments in military upgrades and the presence of important defense contractors and tech companies. Increasing incidents involving drones near airports, borders, and vital infrastructure have also boosted the need for counter-drone systems. Furthermore, strong government support and regulations, like those from the Department of Homeland Security, are driving the use of anti-drone solutions in both military and civilian areas in the region.

The United States is the biggest market for anti-drone technology in the world. This growth is fueled by increasing national security concerns and a significant rise in unauthorized drone activity near sensitive areas like airports, military bases, and critical infrastructure. The U.S. Department of Defense (DoD), the Department of Homeland Security (DHS), and the Federal Aviation Administration (FAA) are investing and supporting the development and use of counter-UAS systems. These systems include radar detection, RF jamming, electro-optical/infrared sensors, and directed energy weapons, such as high-powered microwaves and lasers. The U.S. market benefits from major defense contractors like Lockheed Martin, Raytheon Technologies, Northrop Grumman, and innovative tech companies like Dedrone and Anduril Industries. Government-led initiatives, including the DoD’s Counter-UAS Strategy and the FAA’s UAS Traffic Management framework, are speeding up adoption in both military and civilian areas. As drone threats keep changing, the U.S. anti-drone market is expected to grow at a strong double-digit rate in the coming years.

Competition: Anti Drone Systems Market

The Anti drone market is highly competitive, with key players focusing on innovation, product efficiency, and strategic partnerships to strengthen their market position. Major companies include Lockheed Martin Corporation, Raytheon Technologies Corporation, Northrop Grumman Corporation, Thales Group, DroneShield Ltd., BAE Systems plc., Boeing. These players are investing in R&D to develop anti drone tailored for military & Défense, homeland security, commercial applications, driving ongoing competition and technological advancement in the market.

Lockheed Martin Corporation, Raytheon Technologies Corporation, Northrop Grumman Corporation, Thales Group, DroneShield Ltd., BAE Systems plc., Boeing are among the leading companies active in the market.

Lockheed Martin Corporation, headquartered in Bethesda, Maryland, is a global aerospace and defense giant and a leading player in the anti-drone technology market. The company leverages its deep expertise in advanced weapon systems, radar technologies, and directed energy weapons to develop cutting-edge counter-UAS solutions. Lockheed Martin’s anti-drone portfolio includes high-energy laser systems, such as the Advanced Test High Energy Asset (ATHENA), and integrated air defense systems capable of detecting, tracking, and neutralizing hostile drones. Its solutions are widely deployed by the U.S. military and allied defense forces to protect critical assets and operational zones from increasing unmanned aerial threats. With continuous investment in R&D and strategic defense contracts from the U.S. Department of Defense, Lockheed Martin remains at the forefront of innovation in the global anti-drone market.

ANTI DRONE SYSTEMS MARKET SNAPSHOT | |

Market size in 2024 | USD 3.7 Billion |

Market forecast in 2032 | USD 22.1 Billion |

Compound Annual Growth Rate (2025-2032) | 24.8% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Segments Covered | System Type, Application, Range, Platform, Frequency Band, Component, End Use |

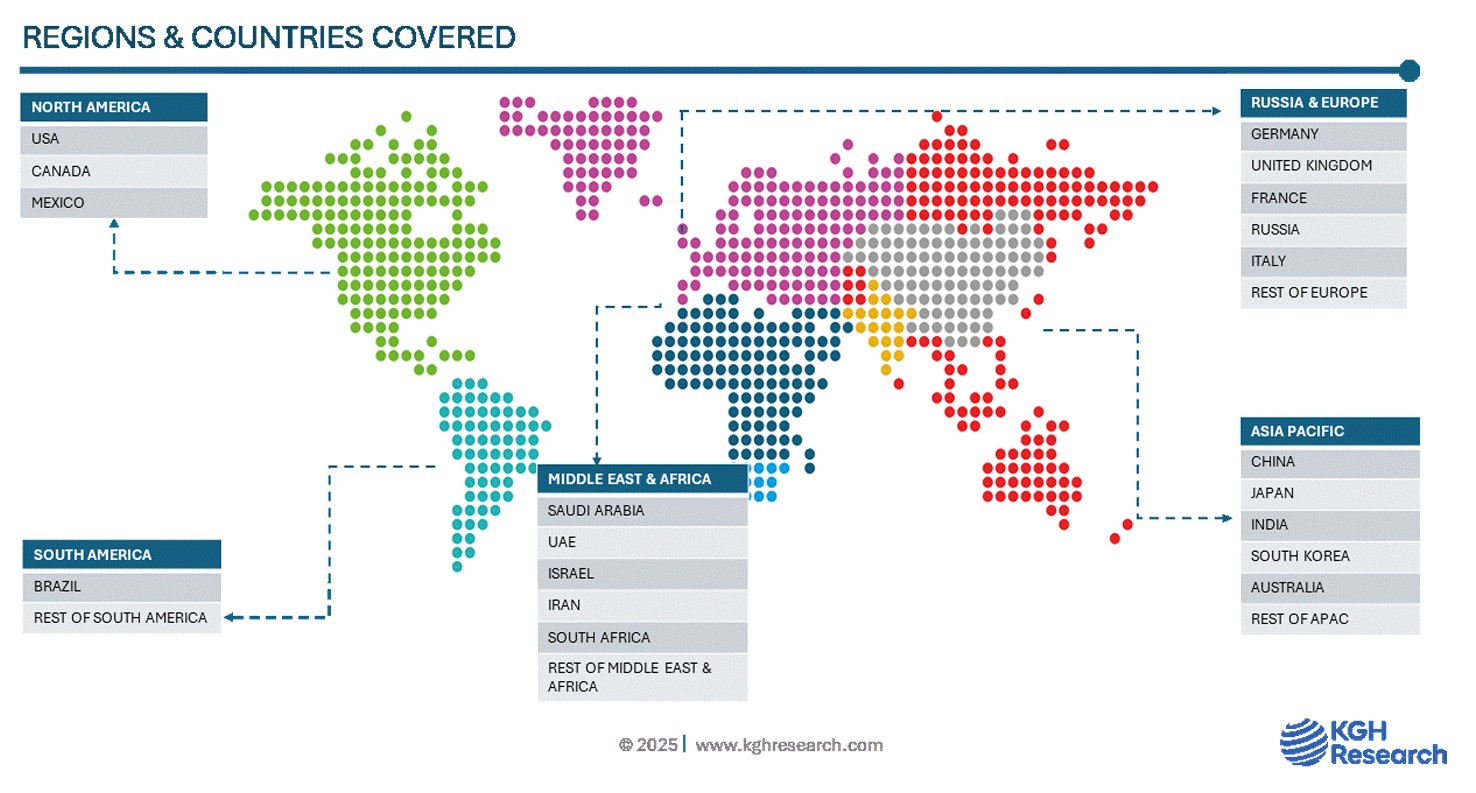

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, Russia, France, China, India, Japan, South Korea, Australia, South Africa, UAE, Saudi Arabia, Israel, Iran, Brazil, and Rest of the World |

Companies Profiled | RTX, BOEING, DETECT, LOCKHEED MARTIN, LEONARDO, THALES, NORTHROP GRUMMAN CORPORATION, ELBIT SYSTEMS, LITEYE SYSTEMS, RAYTHEON TECHNOLOGY, SAAB, IAI, RAFAEL, SKYLOCK, DRONESHIELD, DEDRONE. |