Food Packaging Market (2022 - 2032)

FOOD PACKAGING MARKET SIZE & SHARE BY PRODUCT TYPE (BOXES, BAGS & POUCHES, BOTTLES & JARS, TRAYS, CANS, CARTONS), BY MATERIAL TYPE (PLASTIC, CORRUGATED BOARD, PAPER & PAPERBOARD, WOOD, METAL), PACKAGING TYPE (RIGID, FLEXIBLE, SEMI-RIGID), TECHNOLOGY (MAP, VACUUM PACKAGING, ACTIVE PACKAGING, INTELLIGENT PACKAGING), BY APPLICATION, BY END USE AND BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: PKG8001-0302 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: JULY 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

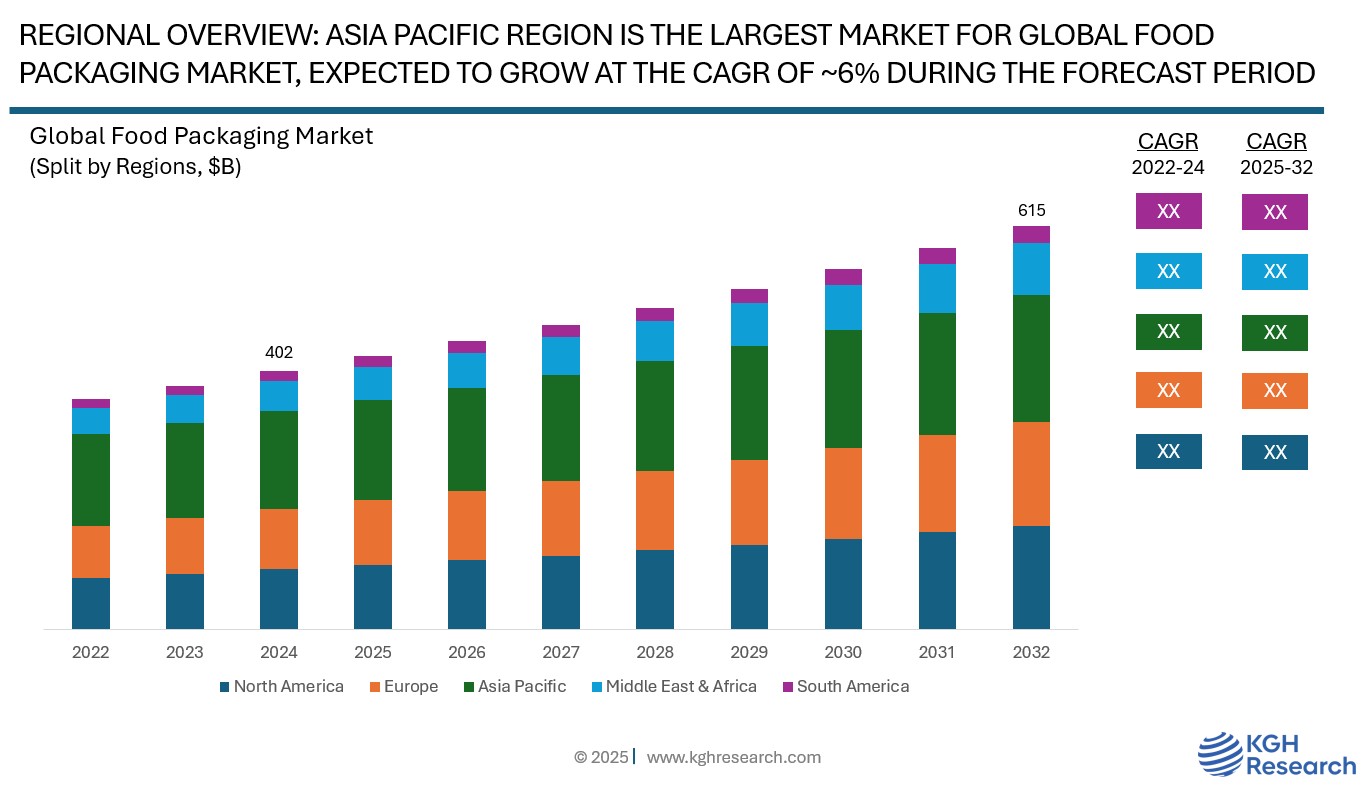

Market Overview: The global food packaging market was valued at approximately USD 402 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 5.4% from 2025 to 2032 to reach USD 615 billion by 2032. The global market for food packaging is largely propelled by the increasing demand for convenient, ready-to-eat, and processed food items, especially in urban environments and fast-paced lifestyles. Heightened consumer awareness about food safety, hygiene, and extending shelf life has led to a notable rise in the use of advanced packaging solutions that safeguard food from contamination and spoilage. Furthermore, the growth of online food delivery services and e-commerce grocery platforms has increased the need for sturdy and secure packaging types. Innovations in technology, such as active, smart, and sustainable packaging, are also becoming more popular due to environmental concerns and regulatory demands for eco-friendly options. The expanding middle-class population in developing nations, along with shifting dietary patterns and elevated disposable incomes, is additionally driving the substantial growth of the food packaging sector globally.

MARKET DYNAMIC

GROWTH DRIVERS:

- Rising demand for processed & packaged foods due to urbanization and busy lifestyles

- Increased awareness about food hygiene and safety, leading to adoption of tamper-evident and protective packaging.

- Growing e-commerce and online food delivery services demanding durable packaging

- Technological advancements such as smart packaging, biodegradable films, and vacuum sealing to enhance shelf life

NEW GROWTH OPPORTUNITIES:

- Development of sustainable packaging solutions to meet eco-conscious consumer demands

- Adoption of smart and intelligent packaging (e.g., freshness indicators, QR codes) to enhance safety

- Emerging markets like India, Southeast Asia, and Africa with rising consumption of packaged food

- Customization and branding through innovative packaging to create differentiation on retail shelves

MARKET RESTRAINTS:

- Environmental concerns and waste management issues related to single-use plastic packaging

- Volatility in raw material prices

- High costs associated with sustainable and smart packaging technologies

- Regulatory restrictions on certain packaging materials, especially plastics and non-recyclables

GROWTH HURDLES:

- Intense competition from regional and global players leading to price pressures. Supply chain disruption

- Consumer shift toward zero-waste and plastic-free lifestyles may reduce demand for traditional packaging

- Supply chain disruptions

Product Type: Market Insights

The food packaging market, when divided by product type, consists of a variety of packaging solutions aimed at addressing the different requirements of food producers and consumers. Boxes are frequently utilized for dry foods, frozen meals, and baked goods because of their robust design and ease of stacking. Bags and pouches, recognized for their lightweight and flexible nature, are commonly employed for snacks, frozen foods, and single-serve items, providing convenience and cost-effectiveness. Bottles and jars, usually made from plastic or glass, are well-suited for holding liquids, sauces, and condiments, offering visibility and prolonged shelf life. Films and wraps play a crucial role in packaging perishable goods such as fruits, vegetables, and meats, as they help maintain freshness and provide barrier protection. Trays are frequently used for fresh meats, poultry, and seafood, ensuring product stability and sanitation. Cans, known for their strength and longevity, are utilized for a variety of preserved foods including soups and vegetables. Cartons are favoured for packaging liquids like milk and juices, particularly in aseptic formats that do not need refrigeration. The “Others” category encompasses niche and innovative packaging solutions such as clamshells and eco-friendly options. Collectively, these product types respond to changing consumer preferences, safety regulations, and sustainability demands within the global food packaging sector.

Material Type: Market Insights

The food packaging sector is divided by material type into Plastic (both non-biodegradable and biodegradable), Corrugated Board, Paper & Paperboards, Wood, Metal, and Others. Plastic remains the predominant material due to its lightweight nature, versatility, and excellent barrier properties; nonetheless, rising environmental concerns are boosting the demand for biodegradable plastic alternatives. Corrugated boards are widely utilized for secondary and tertiary packaging because of its durability and recyclability. Paper and paperboards are becoming more popular as sustainable options, particularly for dry and takeaway food items. While wood and metal are used less frequently, they play a significant role in premium or long-shelf-life packaging. Other materials encompass a variety of combinations or innovations, such as compostable biopolymers and multi-layer laminates. The growing focus on sustainability and recyclability continues to shape material preferences throughout the industry.

Packaging Type: Market Insights

The food packaging industry can be categorized into three types: rigid, flexible, and semi-rigid packaging. Rigid packaging includes materials such as glass bottles, metal cans, and hard plastic containers, which provide excellent protection and structural integrity, making them suitable for beverages, dairy items, and ready-to-eat meals. In contrast, flexible packaging comprises materials like films, pouches, and wraps that are lightweight and can easily conform to the shape of their contents. This type is often used for snacks, frozen meals, and condiments, thanks to its affordability and convenience. Semi-rigid packaging offers a compromise between the two, providing moderate support while maintaining some degree of flexibility. It is commonly utilized for products such as trays, tubs, and clamshell containers. This classification allows manufacturers to meet diverse product needs, extend their shelf life, enhance branding, and respond to consumer demands for convenience and sustainability.

Technology: Market Insights

The food packaging market is categorized by technology into several segments including Modified Atmosphere Packaging (MAP), Vacuum Packaging, Active Packaging, Intelligent Packaging, and Others. MAP technology enhances the shelf life of food products by altering the internal atmosphere of the package, typically by decreasing oxygen levels and increasing inert gases such as nitrogen or carbon dioxide. Vacuum packaging entails removing air from the package prior to sealing, which prevents oxidation and the growth of microbes. Active packaging features elements that engage with the product or its surroundings, such as oxygen scavengers or moisture absorbers, to preserve food quality. Intelligent packaging consists of components like sensors or indicators that give real-time updates regarding the food’s condition, including its freshness, temperature, or spoilage status. The “Others” category encompasses innovative or hybrid packaging solutions that cater to the needs of specialized food products. This classification underscores the industry’s increasing focus on food safety, extending shelf life, and monitoring quality in real-time.

Application: Market Insights

According to application, the food packaging industry is categorized into segments such as Bakery & Confectionery, Beverages, Dairy Products, Meat, Poultry & Seafood, Ready-to-Eat Food, Snacks & Savory Items, Fruits & Vegetables, and Others. Each segment possesses unique packaging requirements, Bakery & Confectionery emphasize freshness and aesthetic appeal; Beverages necessitate materials that are secure against leakage and tampering; Dairy Products require hygiene and temperature management; while Meat, Poultry & Seafood demand packaging that is resistant to leaks and contamination. Ready-to-Eat Foods must have solutions that are microwavable and easy to carry, whereas Snacks & Savory Items focus on convenience and portion sizing. Fruits & Vegetables benefit from packaging that allows for breathability and sustainability.

End Use: Market Insights

Based on end use, the food packaging market is divided into segments such as Quick Service Restaurants (QSRs), Cafés & Kiosks, Full-Service Restaurants, Chain Restaurants, and Others (including FMCG companies, hotels, and retailers). Quick Service Restaurants require packaging that facilitates speed, portability, and brand visibility. Cafés & Kiosks prioritize compact, user-friendly designs that cater to on-the-go consumption. Full-Service Restaurants typically need packaging for take-out and delivery that preserves food quality and presentation. Chain Restaurants look for standardized, scalable, and sustainable packaging solutions that align with their brand identity. The “Others” category includes various sectors such as FMCG brands, hospitality, and retail, each with specific packaging needs influenced by product type, shelf life, and consumer experience. This segmentation underscores the necessity for packaging to evolve in response to different foodservice settings and distribution channels.

Regional: Market Insights

The Asia Pacific region is currently the largest and the most rapidly expanding market for food packaging worldwide, which can be attributed to a mix of economic, demographic, and industrial influences. This area includes some of the most populous nations globally, such as China, India, Indonesia, and Japan, where increasing urbanization and a growing middle class are greatly raising the demand for both processed and packaged food items.

The swift industrial growth and the expansion of the food and beverage industry across various countries in Asia Pacific have resulted in a higher adoption of sophisticated packaging technologies, such as vacuum packaging, modified atmosphere packaging (MAP), and active packaging, aimed at improving shelf life and ensuring food safety. Notably, China is at the forefront of the region, characterized by a strong manufacturing sector, an evolving retail environment, and a highly digitized e-commerce market that has contributed to the rise in packaged food consumption via online platforms. Additionally, a heightened awareness of health and a preference for hygienically packaged, ready-to-eat meals among urban consumers are driving the demand for innovative and sustainable food packaging options. Additionally, regional governments are promoting sustainability initiatives, encouraging manufacturers to utilize biodegradable materials, recyclable plastics, and paper-based substitutes. The presence of both global and local food packaging firms, the availability of raw materials, lower labor costs, and favorable regulatory frameworks further bolster the ability of the region to effectively cater to both domestic and export markets. Consequently, Asia Pacific is anticipated to maintain its leadership in the global food packaging market regarding both market share and future growth potential.

Competition: Food Packaging

The global food packaging sector is fiercely competitive, with top companies prioritizing innovation, product effectiveness, sustainability, and strategic collaborations to enhance their market presence and secure competitive advantage. These organizations are investing in advanced materials, smart packaging technologies, and recyclable options to address the changing needs of end-use industries and adhere to environmental regulations. key players in the global Food Packaging market include Amcor Plc, Berry Global Inc., Mondi Group, Smurfit Kappa Group, Sealed Air Corporation, Coveris Holdings S.A., Constantia Flexibles, Sonoco Products Company, and WestRock Company. These firms continuously adjust to market trends by emphasizing recyclability, automation, and digital integration in packaging to efficiently meet industrial requirements while minimizing environmental impact.

GLOBAL FOOD PACKAGING MARKET SNAPSHOT | |

Market size in 2024 | USD 402 Billion |

Market forecast in 2032 | USD 615 Billion |

Compound Annual Growth Rate (2025-2032) | 5.4% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Growth Drivers | Rising demand for processed & packaged foods due to urbanization and busy lifestyles, Increased awareness about food hygiene and safety, leading to adoption of tamper-evident and protective packaging, growing e-commerce and online food delivery services demanding durable packaging, Technological advancements |

Segments Covered | Product Type, Material Type, Technology, Packaging Type, Application, End Use, And Region |

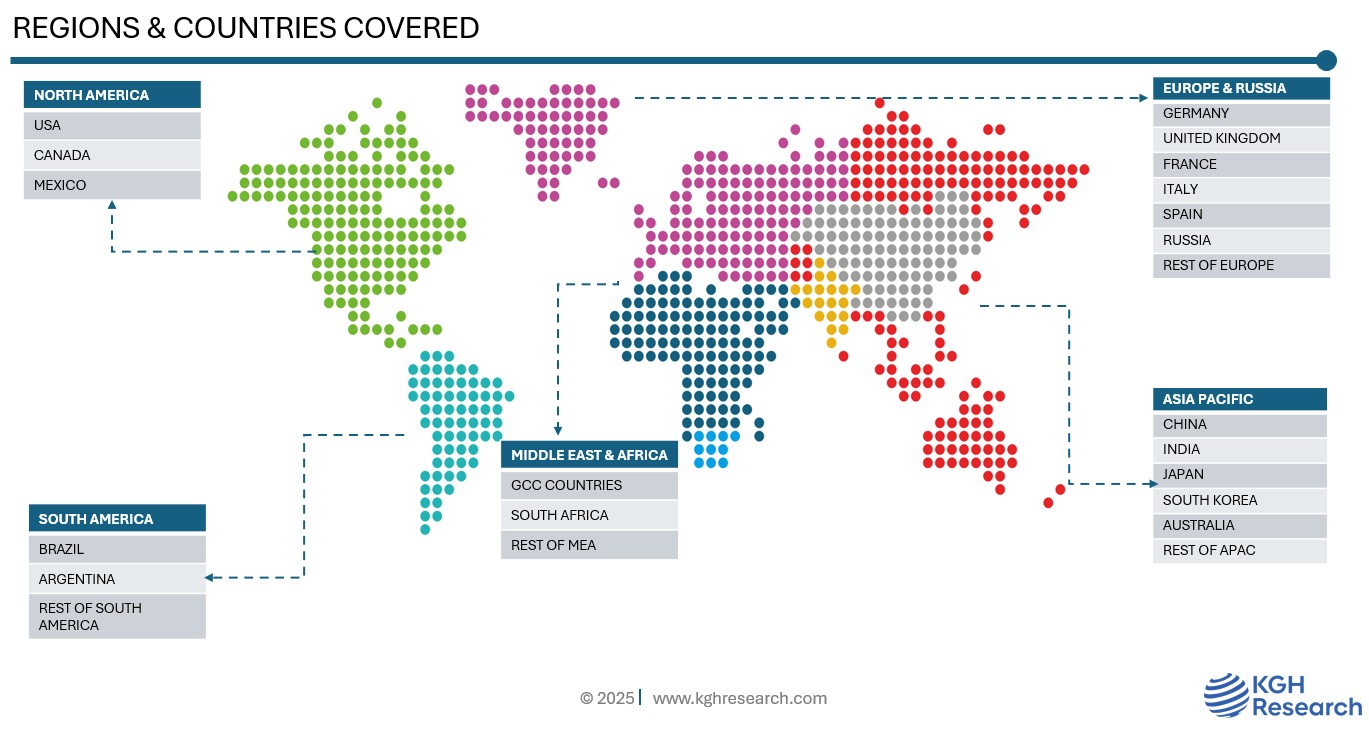

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, France, Spain, Russia, China, India, Japan, South Korea, Australia, South Africa, Brazil, Argentina |

Companies Profiled (25+) | BERRY GLOBAL, AMCOR LIMITED, SMURFIT WESTROCK PLC, MONDI, STORA ENSO, CONSTANTIA FLEXIBLES, PLASTIPAK, TETRA PAK INTERNATIONAL S.A., DS SMITH, CROWN HOLDINGS INC., COVERIS GROUP, EXXONMOBIL CHEMICAL, SMURFIT KAPPA GROUP, GRAPHIC PACKAGING INTERNATIONAL, WESTROCK COMPANY, SONOCO PRODUCTS COMPANY, AND MANY MORE |