Automotive Airbag Fabric Market (2022 - 2032)

AUTOMOTIVE AIRBAG FABRIC MARKET SIZE & SHARE BY APPLICATION (DRIVER, PASSENGER, SIDE, CURTAIN, KNEE), BY FABRIC (FLAT, OPW), BY VEHICLE TYPE (PASSENGER CAR, LCV, MHCV, BUSES), BY COATING TYPE (COATED FABRIC, UNCOATED FABRIC), BY COATING MATERIAL (NEOPRENE, SILICONE, POLYURETHANE, OTHERS), BY YARN TYPE (POLYAMIDE, POLYESTER) AND BY REGION & COUNTRY–FORECAST TO 2032

| Report Code: A&T2003-0401 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: AUGUST 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

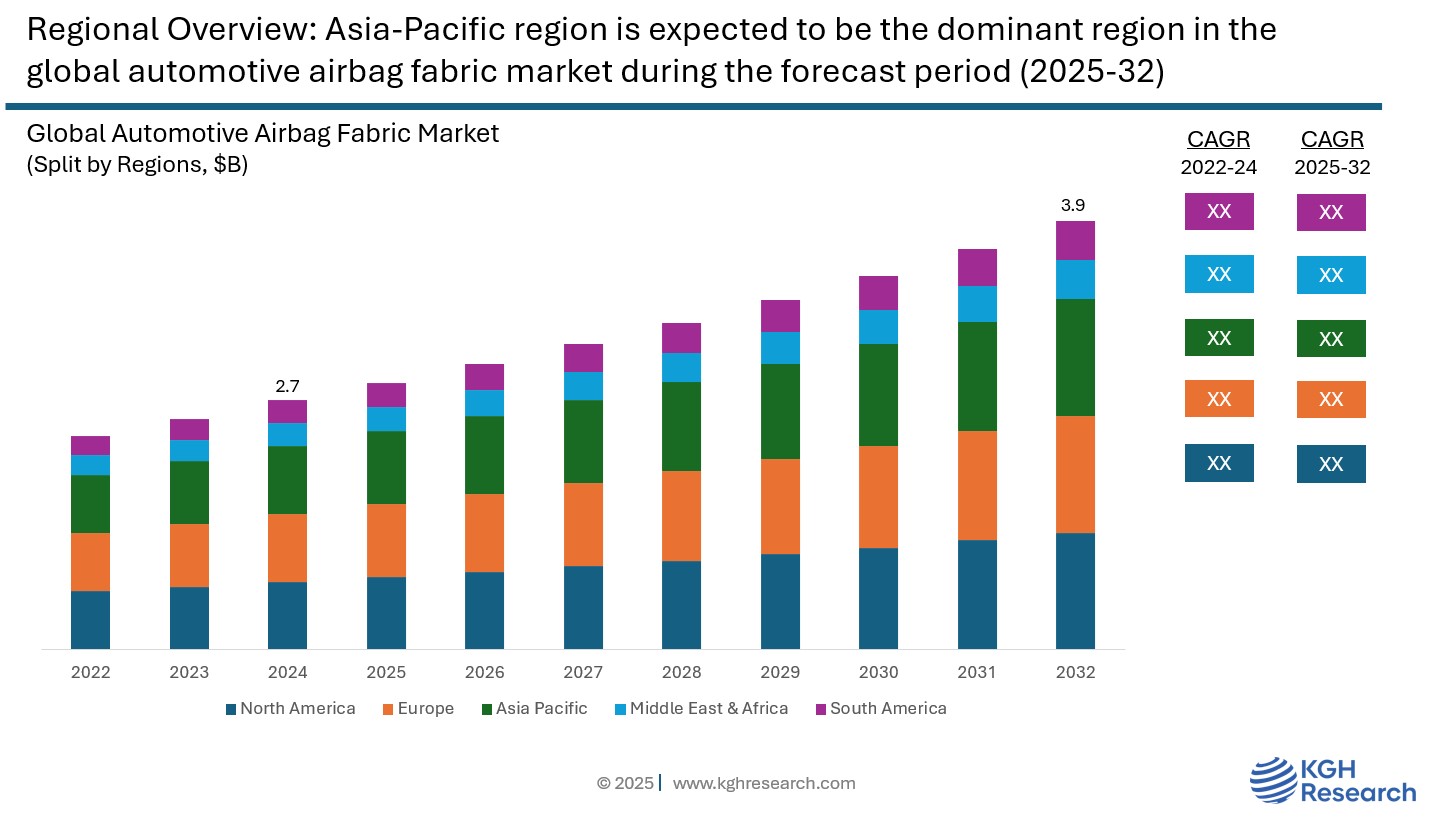

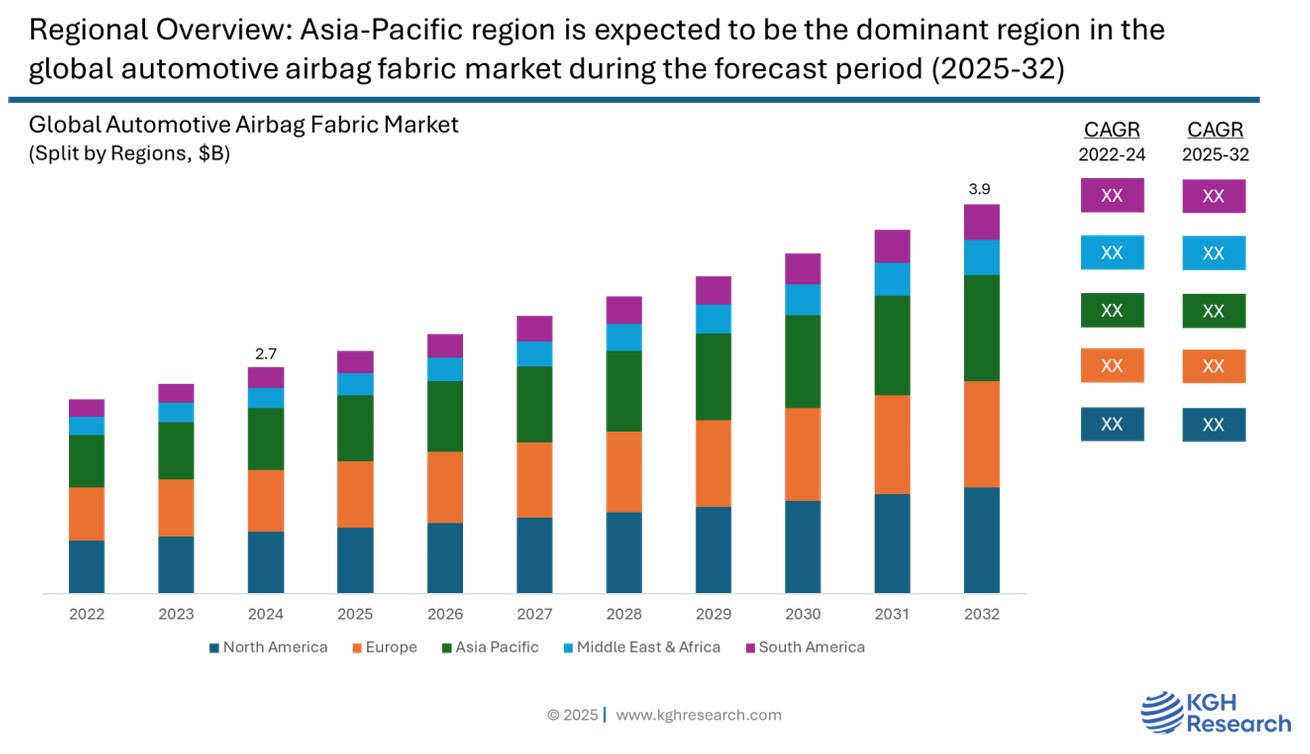

Market Overview: The global automotive airbag fabric market was estimated at US $2.7 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 4.7% from 2025 to 2032 to reach $3.9 billion by 2032. The market is mainly fueled by stricter vehicle safety regulations in many countries. These rules require that both passenger and commercial vehicles include airbags. This regulatory push, along with growing consumer awareness about vehicle safety and the rising demand for better safety features, is greatly boosting the market. Additionally, global automotive production is expanding, particularly in developing countries, which is leading to higher airbag fabric consumption. The trend towards more complete airbag systems, like side, curtain, and knee airbags, is increasing the need for specialized fabrics. Technological improvements in strong, lightweight, and heat-resistant materials, including coated and one-piece woven fabrics, are also very important. Furthermore, the aim to reduce vehicle weight to improve fuel efficiency and meet emission standards is to drive the use of lighter airbag fabrics. The fast growth of electric and self-driving vehicles is creating new interior design needs, leading to more innovation and the adoption of advanced airbag fabric solutions.

MARKET DYNAMIC

GROWTH DRIVERS:

- Increasing vehicle safety regulations, driving higher number of airbag deployment per vehicle

- Rising global automobile production, especially in emerging economies

- Increasing road fatalities are raising consumer awareness of vehicle safety features

- Rising adoption of curtain and side airbags

- Advancements in fabric technology

- Growing demand for automotive variants with higher number of airbags

NEW GROWTH OPPORTUNITIES:

- Emergence of electric & autonomous vehicle

- Increasing demand in emerging markets

- Technological advancements

- Development of pedestrian airbag and exterior airbags

- Opportunity 4

MARKET RESTRAINTS:

- High cost of advanced fabrics

- Raw material price volatility

- Market Restraint 3

- Market Restraint 4

GROWTH HURDLES:

- Dependence on automotive industry cycles

- Supply chain disruptions

- Stringent quality & safety compliance

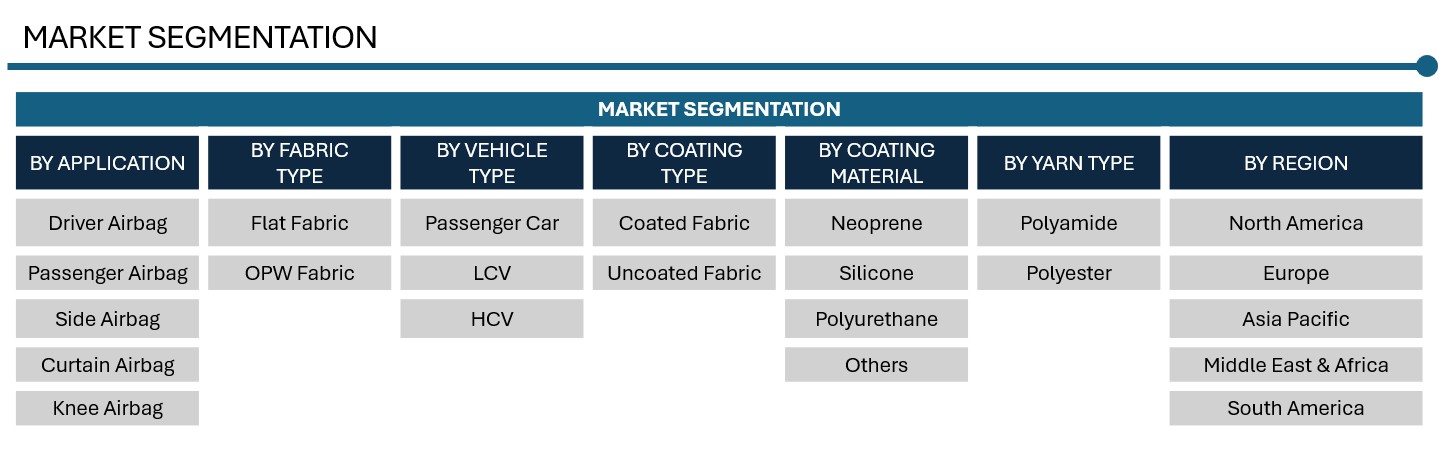

Application: Market Insights

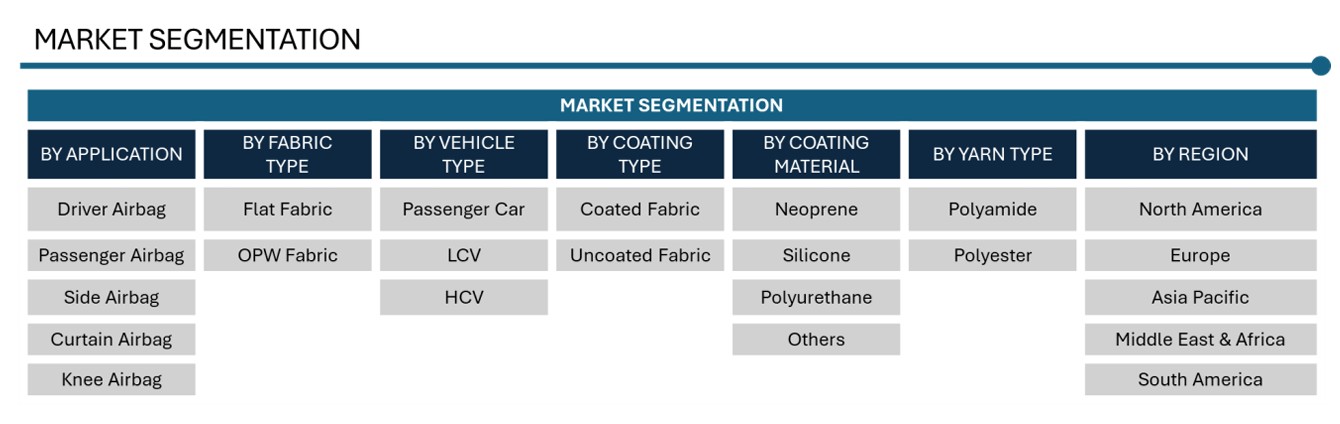

The automotive airbag fabric market includes driver airbags, passenger airbags, side airbags, curtain airbags, and knee airbags. Each type is designed for a specific safety function and requires material characteristics to work well during deployment. Driver airbags are usually placed in the steering wheel. They are among the first airbags required worldwide. These airbags protect the driver’s head and chest during a frontal crash and are often smaller than passenger airbags because they are closer to the driver. Passenger airbags are larger and mounted in the dashboard to protect the front-seat passenger. They need fabrics that can handle higher inflation pressures and temperatures. Many include special coatings to improve heat resistance. Side airbags are typically found in the seat or door panels. They deploy quickly in side-impact crashes to shield the torso. These airbags need strong, compact fabrics that can fold tightly but expand quickly without resistance. Their use is increasing in both front and rear seats as safety standards change. Curtain airbags deploy from the roof lining above the side windows. They help protect the heads of occupants in both the front and rear seats during side impacts or rollovers. Due to their size and coverage area, they require large, lightweight, and tear-resistant fabrics to ensure rapid deployment along the vehicle’s side. Knee airbags are located beneath the dashboard to protect the lower limbs of the driver and, sometimes, the passenger by limiting leg movement during a crash. While they aren’t standard in all vehicles yet, their use is increasing in high-end and safety-focused markets. The fabrics for knee airbags must be strong and flexible to work effectively in tight spaces and inflate quickly. Overall, the increasing number of airbags in each vehicle is driven by stricter crash safety regulations and consumer interest in better safety features. This trend is significantly raising the demand for high-performance airbag fabrics specific to each application. Manufacturers are working to create fabrics that are more heat resistant, stronger, lighter, and capable of being compactly folded.

Fabric Type: Market Insights

The automotive airbag fabric market is mainly divided into Flat Fabric and OPW (One-Piece Woven) Fabric. Each type has unique manufacturing processes and performance features suited for specific airbag uses. Flat Fabric is a traditional woven material that is cut and stitched into the necessary airbag shape. It is the most used type in the market because it is cost-effective and adaptable for various airbag applications, especially in passenger, side, and curtain airbags. However, this type involves extra steps like cutting, sewing, and sealing, which can slightly complicate production and increase the risk of seam failure. On the other hand, OPW Fabric is a more advanced airbag material woven directly into a three-dimensional shape without seams. This design removes the need for sewing, which improves the airbag’s structural integrity and reliability during deployment. OPW fabric is especially important in critical applications like driver and knee airbags, where quick and precise inflation is crucial. Although OPW fabrics are more expensive and harder to produce, their benefits in safety, faster production times, and weight savings are making them more popular, particularly in high-end and safety-focused vehicles. In summary, while flat fabric remains the primary choice and have dominant share in the market due to its flexibility and cost benefits, OPW fabric is gaining attention for its greater strength, fewer failure points, and improved performance in critical deployments.

Vehicle Type: Market Insights

The automotive airbag fabric market is divided into four main types of vehicles including, Passenger Cars, Light Commercial Vehicles (LCVs), Medium & Heavy Commercial Vehicles (HCVs), and Buses. Each category has unique needs based on vehicle design, usage, and safety standards. Passenger Cars hold the largest share of the market. With rising consumer awareness and strict safety regulations worldwide, adding multiple airbags (driver, passenger, side, curtain, and knee) in cars has become common. This trend greatly increases the demand for airbag fabrics in this segment. Automakers are also putting advanced airbag systems in mid-range and compact cars, which further drives up fabric use. Light Commercial Vehicles (LCVs), like vans and small trucks for logistics and transportation, are also seeing more airbag adoption due to changing safety rules, especially in developing countries. While LCVs have typically lagged in airbag use, they are now being fitted with basic airbag systems, such as driver and passenger airbags. This creates a moderate but growing need for airbag fabric. Heavy Commercial Vehicles (HCVs), which include large trucks and buses, make up a smaller yet significant segment. Airbag use in HCVs is increasing, especially in areas with strict safety regulations like Europe and North America. As awareness of driver safety in long-haul transportation rises, manufacturers are starting to include airbag systems in premium and fleet-heavy HCVs. In summary, while passenger cars lead the market due to their volume and the integration of multiple airbags, commercial vehicles—both light and heavy are slowly increasing their contribution to the demand for airbag fabric as safety regulations and fleet upgrades expand worldwide.

Coating Type: Market Insights

Based on coating types, there are two main types of coating: Coated Fabric and Uncoated Fabric. Each type has its own performance features based on specific application needs. Coated Fabric is the leading choice. It is popular because of its excellent air retention and heat resistance. Usually coated with silicone or neoprene, this fabric helps ensure that the airbag inflates properly and stays inflated during an impact. Coated fabrics are mainly used inside airbags, curtain airbags, and passenger airbags, where controlled deployment and sustained inflation are crucial for protecting occupants. The coating also adds durability against the high temperatures produced during deployment from fast gas expansion. Uncoated Fabric is lighter and more breathable. It works well for airbags that need to deploy quickly but do not require prolonged inflation, like driver airbags. It is also more cost-effective and is increasingly found in compact and economy vehicles. This helps lower manufacturing costs without sacrificing basic safety. Recent technological improvements have also boosted the performance of uncoated fabrics, making them a better choice for certain applications. In summary, while coated fabrics are vital for high-performance and safety-critical airbag systems due to which they have dominant share in the market, uncoated fabrics are becoming more popular due to their lightweight nature and cost advantages, particularly in vehicles that prioritize fuel efficiency and affordability.

Coating Material: Market Insights

In the automotive airbag fabric market, the main coating materials are Neoprene, Silicone, Polyurethane, and Others. Each material has unique properties that meet performance, safety, and environmental standards. Neoprene has long been a popular choice. It resists heat, oil, and abrasion effectively. This gives it durability, making it commonly used in older airbag systems. However, its popularity is decreasing due to environmental issues connected to halogenated compounds. Silicone is the most common coating material in today’s airbag fabrics. It offers great thermal resistance, flexibility, and stability. Silicone helps fabrics endure the high heat generated during airbag deployment while maintaining reliable performance over time. You usually find silicone-coated fabrics inside and curtain airbags, where the deployment dynamics are more complex. Polyurethane is becoming more popular as a lightweight and cost-effective option. It resists wear well and has a lower environmental impact than neoprene. Polyurethane is especially useful in applications that need lower burst pressure and is increasingly found in newer airbag designs. The “Others” category includes advanced or hybrid coatings, such as fluoropolymers and specialized blends. These coatings are made to improve specific features like flame resistance, permeability control, or recyclability. They are often used in niche or high-performance automotive markets. Overall, silicone is the leading choice. However, polyurethane and eco-friendly options are gaining traction due to regulatory pressures and automakers’ shift towards lighter, sustainable materials.

Yarn Type: Market Insights

Based on yarn types, the global automotive airbag fabric market is primarily classified as Polyamide and Polyester. Both significantly affect the strength, durability, and deployment efficiency of airbag systems. Polyamide, or Nylon, is the most common yarn type used for airbag fabrics, especially Nylon 6,6. It is preferred for its high tensile strength, resistance to abrasion, and excellent elasticity. These features ensure effective inflation and durability during deployment. Polyamide fabrics can handle high impact forces and are widely used in important applications like driver, passenger, and curtain airbags. Polyester serves as a cost-effective alternative to polyamide. It provides good strength, thermal stability, and chemical resistance, though it typically performs lower than nylon. Polyester yarns are becoming more popular, especially in emerging markets, due to their affordability and ease of processing. Furthermore, polyester’s recyclability and alignment with environmental goals make it an appealing choice in the move towards sustainable airbag materials. Overall, polyamide is dominant in high-performance applications, while polyester is growing in budget-friendly and sustainability-focused areas. This creates a diverse and changing yarn landscape in airbag fabric manufacturing.

Regional: Market Insights

Asia Pacific leads the global automotive airbag fabric market due to high vehicle production volumes, growing use of safety features, and supportive regulatory policies. China, as the largest producer and consumer of vehicles, plays a key role in driving market growth in the region. The Chinese government’s rules requiring airbags in all passenger vehicles, along with increased consumer demand for safer cars, have significantly raised the need for airbag fabrics. India is also becoming an important market, mainly because of government rules that require the installation of driver and passenger airbags in all new cars. Rising middle-class incomes and more vehicle ownership contribute to this trend. Japan and South Korea, known for their advanced automotive technologies and strong export-oriented auto industries, also make significant contributions through both domestic use and global supply of airbag parts. The region has a strong supply chain network, low labour costs, and major global and local airbag fabric manufacturers like Toyobo, Toray Industries, and Hyosung. These companies continue to invest in research and development to create lightweight, high-strength airbag materials that meet changing international safety standards. As vehicle sales keep rising, especially in the compact and mid-sized segments, the demand for airbag fabrics in passenger cars and commercial vehicles is expected to stay strong, further solidifying Asia Pacific’s leading position in the global market.

China holds the largest share of the Asia Pacific automotive airbag fabric market and plays a crucial role worldwide because of its massive automotive production capacity and fast-changing safety regulations. As the biggest car producer and consumer, China has seen a significant rise in the demand for airbag fabrics. This demand is driven by the growing focus on vehicle safety and government requirements. In recent years, the Chinese government has implemented stricter rules requiring airbags in all new vehicles, including both driver and passenger sides. These policies, along with rising consumer awareness and expectations about automotive safety, have sped up the use of advanced airbag systems across different types of vehicles. China has many domestic fabric manufacturers and Tier-1 suppliers that support the airbag production process. Having local manufacturing lowers production costs and ensures quicker delivery times, which makes China a key manufacturing hub for airbag fabrics. Global companies are also increasingly investing in Chinese facilities or teaming up with local businesses to meet the rising demand. Furthermore, with the rapid growth of electric vehicles (EVs) and premium car segments in China, the use of complex multi-airbag systems has become more common. This trend is driving up fabric consumption. As the Chinese market continues to embrace advanced safety technologies, its impact on global airbag fabric trends will remain strong and enduring.

Competition: Automotive Airbag Fabric Market

The automotive airbag fabric market is highly competitive. Several global and regional players are working hard to increase their market share through innovation, partnerships, and technology. Key manufacturers focus on improving fabric strength, durability, and heat resistance to meet safety standards set by regulatory bodies in various regions. The strong competition also comes from the rising demand for lightweight, high-performance materials that boost vehicle efficiency and occupant safety. Companies are investing heavily in research and development to create cost-effective and sustainable solutions, including recyclable and eco-friendly coatings. Moreover, partnerships between automakers and airbag fabric suppliers are becoming more common. This leads to quicker innovation cycles and tailored product offerings. In addition to established global companies, regional manufacturers in Asia Pacific, especially in China, Japan, and India, are entering the market with competitive prices and local production capabilities. This has increased price competition and pressured global companies to maintain efficiency while ensuring product quality. Overall, the competitive nature of the market is driving rapid technological progress, greater production scalability, and ongoing improvements in product performance. Key players in the market include Toray Industries, Inc., Hyosung Corporation, Kolon Industries, Inc., HMT (Xiamen) New Technical Materials CO., Ltd, Teijin, Indorama Ventures, and many more.

Toray Industries, Inc. is one of the top companies in the global automotive airbag fabric market. It is known for its skills in high-performance fibers and material technologies. Headquartered in Japan, Toray has a strong global presence and a diverse portfolio that spans various industries, including automotive, aerospace, electronics, and life sciences. In the airbag fabric segment, Toray is recognized for producing high-quality nylon 6.6 and polyester yarns, which are essential materials for airbag fabrics. The company uses its own fiber technologies to create fabrics with outstanding strength, durability, heat resistance, and low permeability. These qualities are crucial for effective airbag deployment. Toray’s fabrics are widely used in driver, passenger, side, curtain, and knee airbags. Toray’s advantage comes from its vertically integrated production model, global supply chain, and strong research and development capabilities. The company continues to innovate with eco-friendly materials and sustainable manufacturing processes. This is in response to the growing demand for lightweight and recyclable automotive parts. With manufacturing facilities and partnerships in Asia, North America, and Europe, Toray is well-positioned to meet the rising demand from global automotive original equipment manufacturers. Its long-standing relationships with major car makers and airbag module suppliers strengthen its reputation as a reliable and important player in the automotive airbag fabric market.

AUTOMOTIVE AIRBAG FABRIC MARKET SNAPSHOT | |

Market Size In 2025 | USD 2.7 BILLION |

Market Forecast In 2032 | USD 3.9 BILLION |

Compound Annual Growth Rate (2025-2032) | 4.7% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Region Dominance | Asia Pacific |

Country Dominance | China |

Growth Driver | Increasing vehicle safety regulations, Rising global automobile production, especially in emerging economies, Increasing road fatalities are raising consumer awareness of vehicle safety features Rising adoption of curtain and side airbags Advancements in fabric technology, Automakers are seeking lightweight components to improve fuel efficiency and reduce emissions |

Segments Covered | BY APPLICATION, BY FABRIC TYPE, BY VEHICLE TYPE, BY COATING TYPE, BY COATING MATERIAL, BY YARN TYPE, AND BY REGION & COUNTRIES |

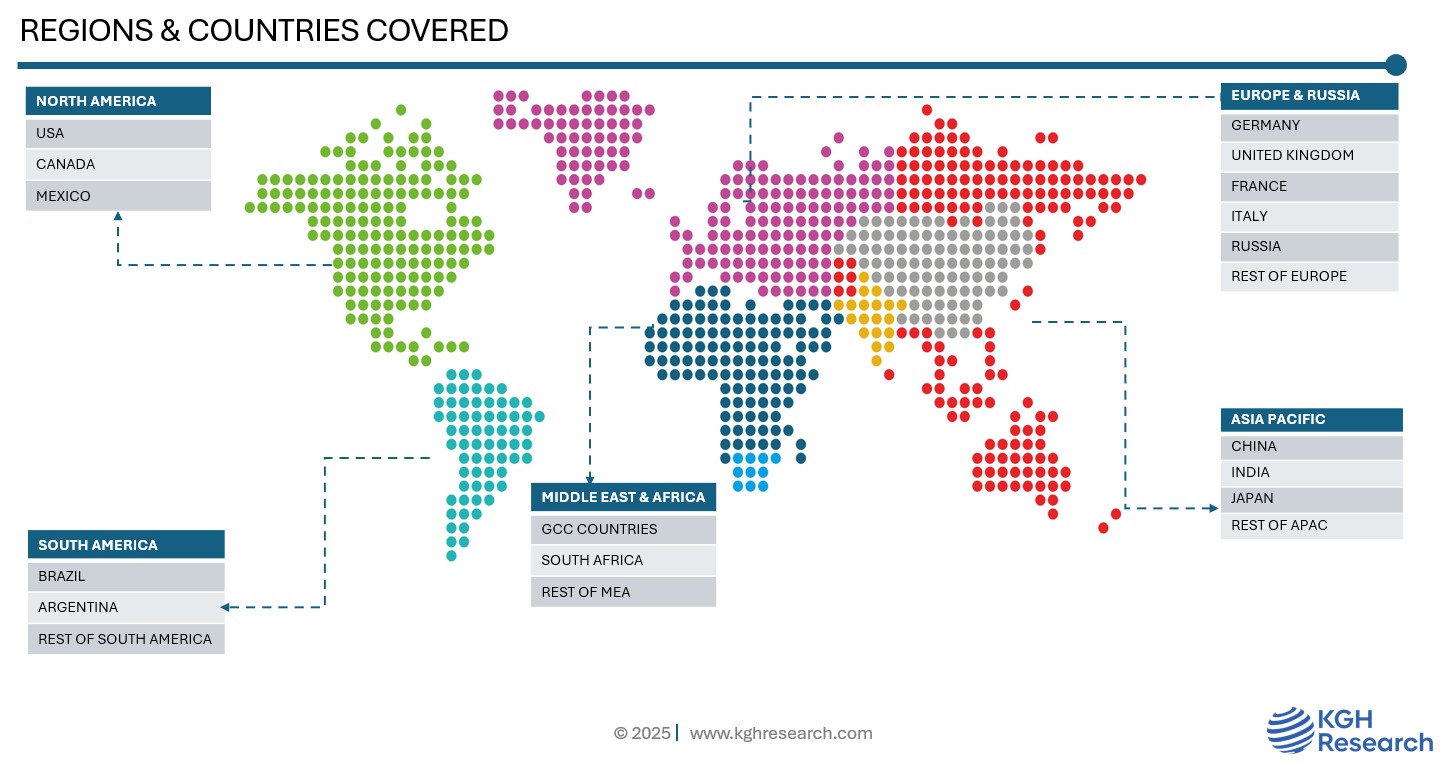

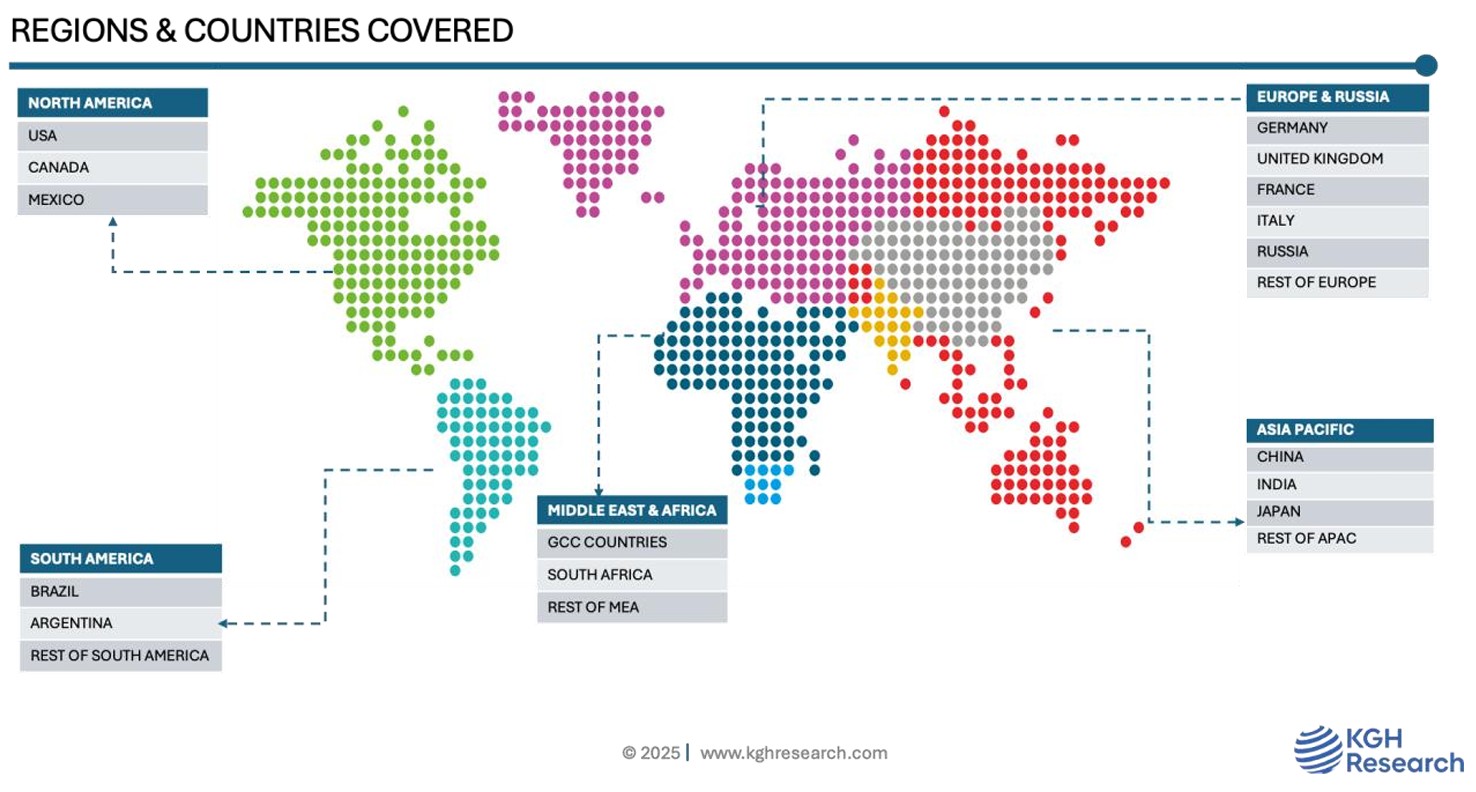

Regions Covered | NORTH AMERICA, EUROPE, ASIA PACIFIC, SOUTH AMERICA, MIDDLE EAST & AFRICA |

Countries Covered | USA, CANADA, MEXICO, UK, GERMANY, FRANCE, RUSSIA, ITALY, REST OF THE EUROPE, CHINA, INDIA, JAPAN, AUSTRALIA, INDONESIA, REST OF APAC, BRAZIL, ARGENTINA, REST OF THE WORLD |

Companies Profiled (20+) | TORAY INDUSTRIES, INC., HYOSUNG CORPORATION, KOLON INDUSTRIES, INC., HMT (XIAMEN) NEW TECHNICAL MATERIALS CO., LTD, INDORAMA VENTURES, GLOBAL SAFETY TEXTILES, AUTOLIV, INC., KOLON INDUSTRIES, TEIJIN LIMITED, TOYOBO, MILLIKEN, AND MANY MORE. |