Industrial Packaging (2022 - 2032)

INDUSTRIAL PACKAGING MARKET SIZE & SHARE BY PRODUCT TYPE (DRUMS, BOXES & CARTONS, CRATES & TOTES, TRAYS & PALLETS, INTERMEDIATE BULK CONTAINERS, BAGS & SACKS, CANS & PAILS), BY MATERIAL (PLASTIC, METAL, PAPER & PAPERBOARD, WOOD & FIBER), BY MANUFACTURING TECHNIQUE (INJECTION MOLDING, BLOW MOLDING, EXTRUSION, THERMOFORMING), BY PACKAGING TYPE (RIGID, FLEXIBLE), BY END USE AND BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: PKG8002-0303 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: SEPTEMBER 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

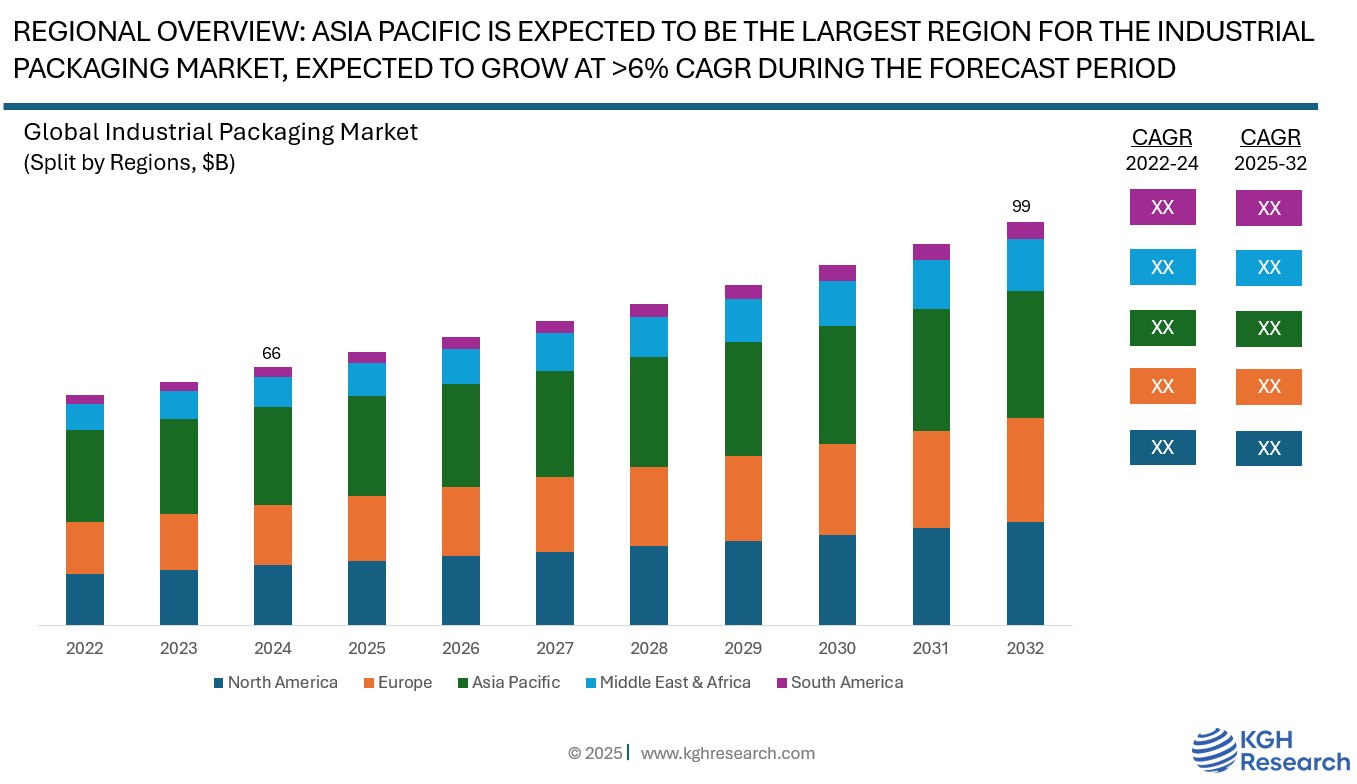

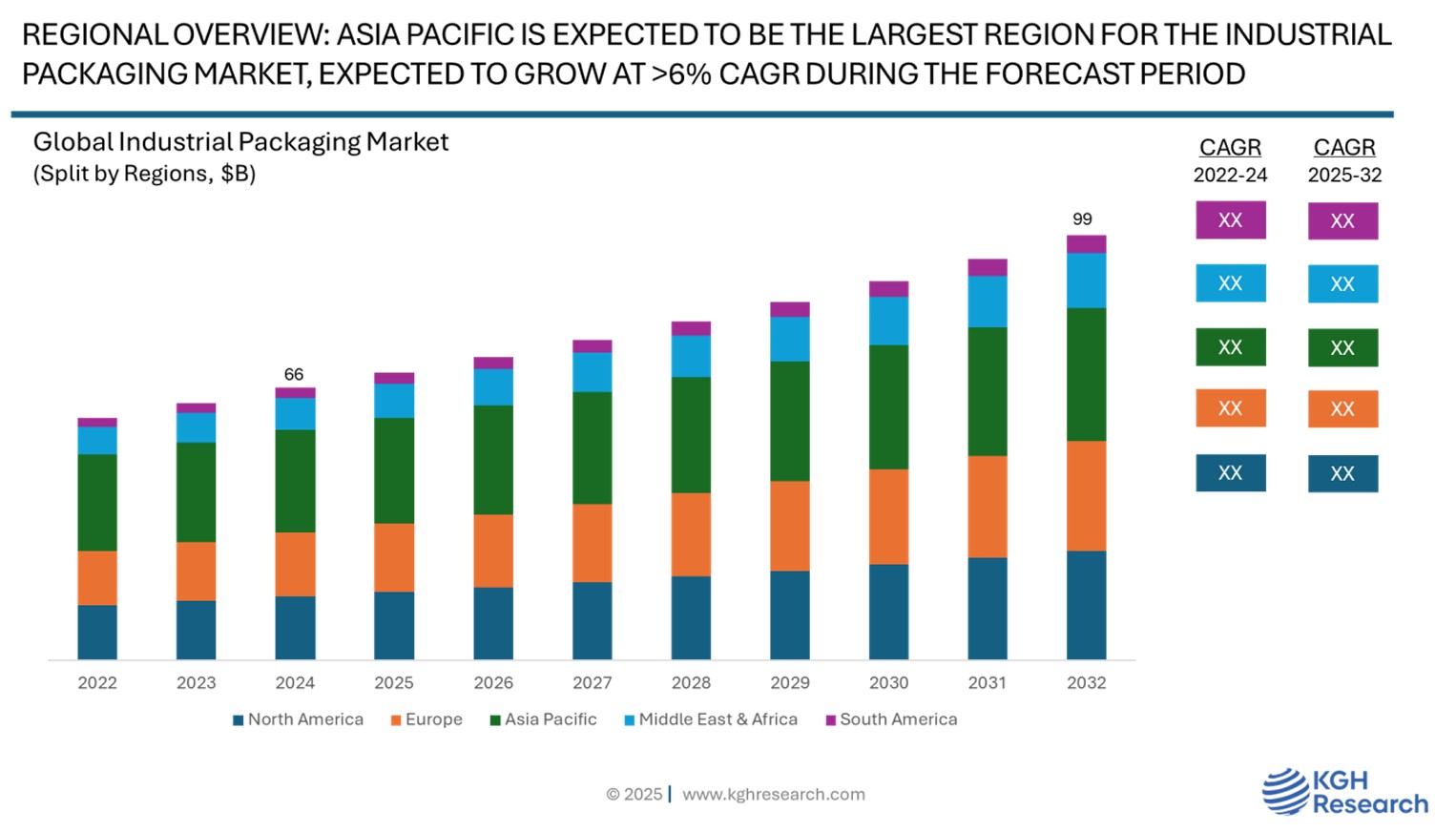

Market Overview: The global industrial packaging market was valued at approximately USD 66 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 5.1% from 2025 to 2032 to reach USD 99 billion by 2032. The rapid expansion of manufacturing and industrial operations in industries like electronics, chemicals, automotive, and construction is the main factor propelling the global industrial packaging market. The need for bulk, tamper-proof, and long-lasting packaging solutions that guarantee the safe handling and long-distance transportation of goods has grown dramatically with the growth of international trade and e-commerce. Furthermore, manufacturers are being compelled by the growing emphasis on sustainability to use recyclable and environmentally friendly packaging materials, which is driving market expansion. The need for industrial-grade packaging is also growing because of the food and beverage industry’s expansion, especially in processed and packaged foods. Additionally, the need for heavy-duty packaging products is being fuelled by infrastructure development and urbanization, particularly in emerging economies.

MARKET DYNAMIC

GROWTH DRIVERS:

- Growth in manufacturing & industrial activities

- Sustainability trends & regulatory push

- Globalization of trade & e-commerce

- Increased demand from food & beverage sector

NEW GROWTH OPPORTUNITIES:

- Integration of IoT and tracking technologies in industrial packaging for traceability and security

- Rapid industrialization in Asia-Pacific, Africa, and Latin America offers untapped growth potential

- Growing demand for biodegradable, reusable, and recyclable solutions opens new markets and innovation scopes

MARKET RESTRAINTS:

- Fluctuations in prices raw materials, such as plastic, metal, and paper can affect profit margin.

- Rising restrictions on single-use plastics and carbon emissions can increase compliance costs

GROWTH HURDLES:

- Intense market competition

- Supply chain disruption

- Stringent export/import regulations

- Economic slowdowns or recessions

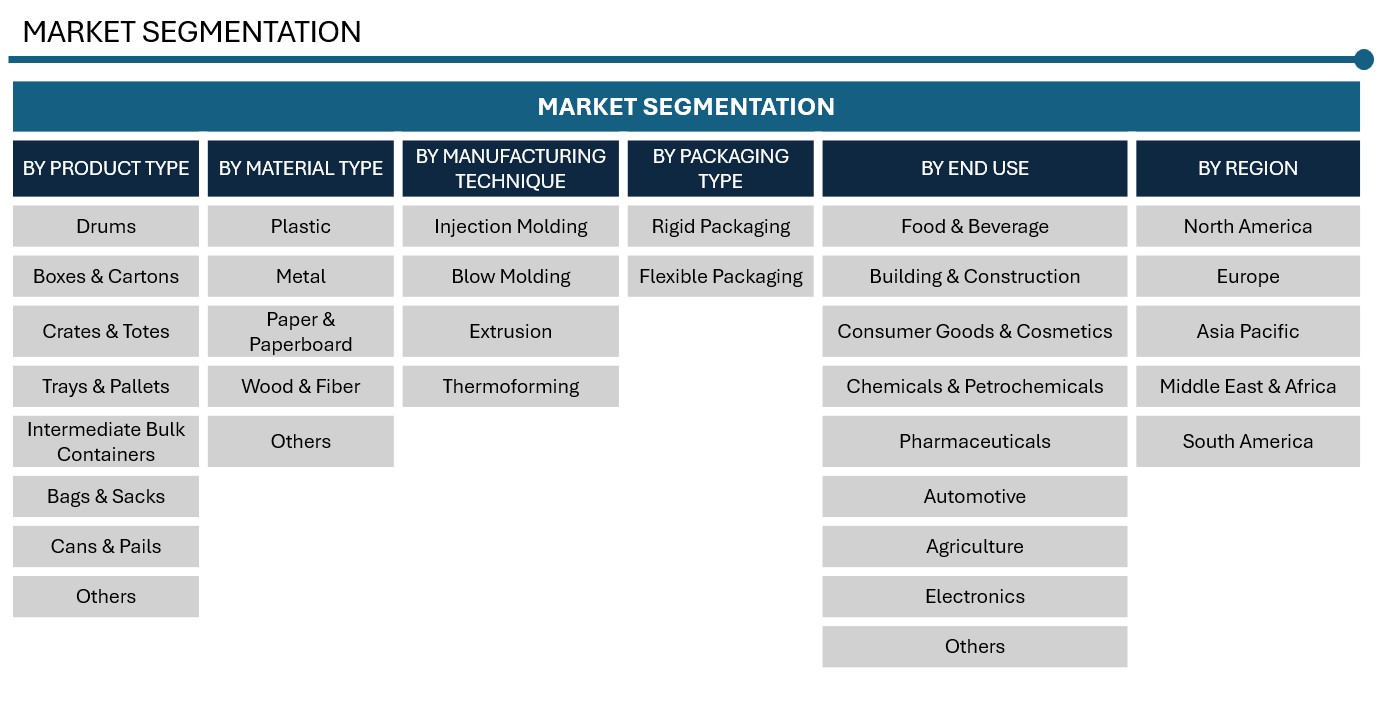

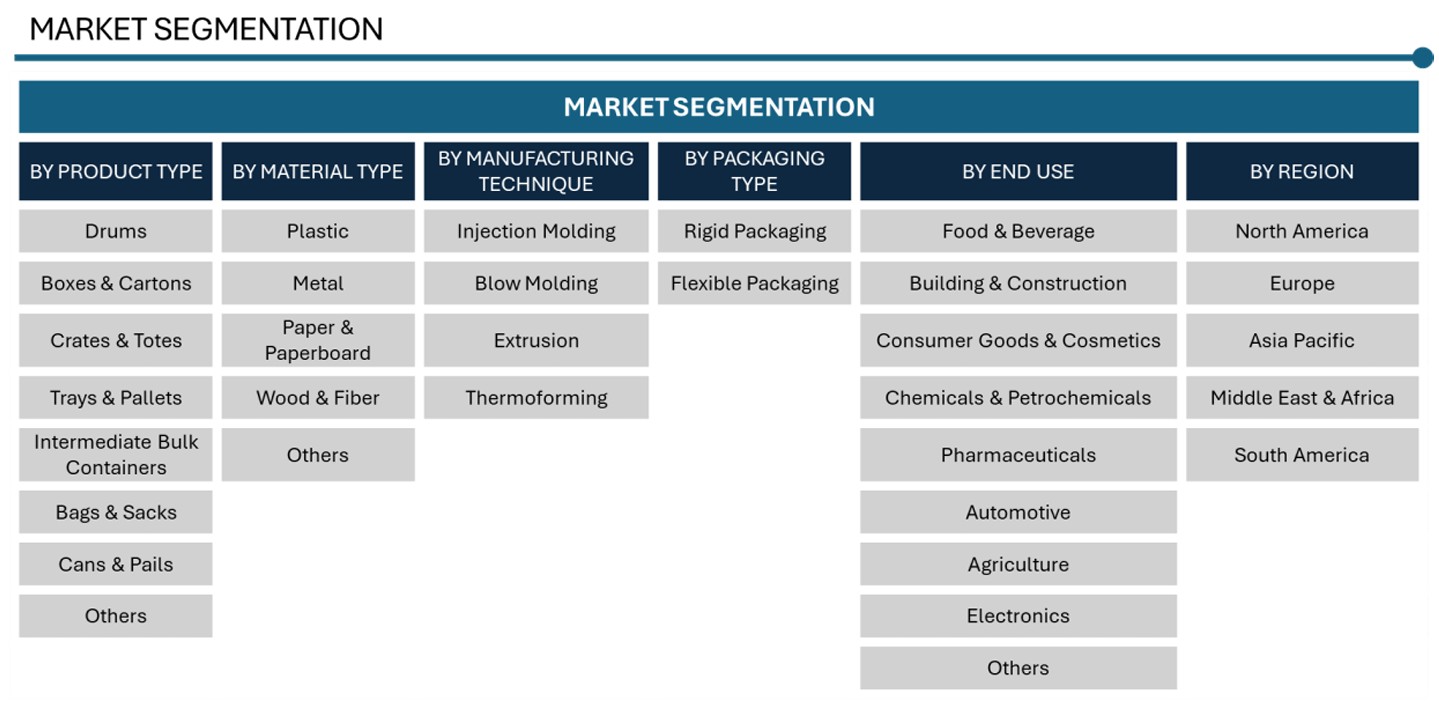

Product Type: Market Insights

The global industrial packaging market is divided into several product types, including drums, boxes and cartons, crates and totes, trays and pallets, intermediate bulk containers (IBCs), bags and sacks, cans and pails, and a few others. Drums are a preferred option for transporting liquids and hazardous materials because they’re durable and leak-proof. On the other hand, boxes and cartons are flexible and cost-effective, making them perfect for a variety of dry goods and industrial parts. Crates and totes are favoured for their strength and reusability, especially in the automotive and manufacturing industries. Trays and pallets play a crucial role in stacking and bulk handling, particularly in warehousing and logistics. Intermediate bulk containers (IBCs) are designed for moving large quantities of fluids or powders, prized for their space efficiency and reusability. Bags and sacks are often used for chemicals, grains, and building materials due to their lightweight and economical design. Cans and pails meet the packaging needs of paints, lubricants, and other semi-liquid products. Lastly, the “others” category encompasses niche or specialized containers that cater to unique industrial needs. Each product type has its specific applications, and the choice often hinges on material characteristics, logistics requirements, and regulatory compliance.

Material Type: Market Insights

By material type, the global industrial packaging market is segmented into plastic, metal, paper & paperboard, wood & fiber, and others. Plastic dominates the market due to its versatility, durability, lightweight nature, and cost-effectiveness. It is the preferred material for both rigid and flexible packaging across a variety of industries, including chemicals, food & beverages, and pharmaceuticals. On the other hand, metal packaging is celebrated for its strength and ability to withstand extreme conditions, making it ideal for storing hazardous materials, liquids, and bulk chemicals. Meanwhile, paper & paperboard are becoming increasingly popular as eco-friendly options, especially in areas where sustainability and recyclability are top priorities. These materials are widely used in food packaging and light industrial applications. Wood & fiber materials are known for their impressive durability and load-bearing capacity, making them perfect for crates, pallets, and heavy-duty tasks.

Manufacturing Technique: Market Insights

The global market for industrial packaging is categorized by manufacturing methods, which include injection molding, blow molding, extrusion, and thermoforming. Injection molding is commonly utilized for creating intricate, high-strength packaging components with accurate dimensions, such as containers, caps, and pallets, particularly in large-scale applications. Blow molding is mainly employed to produce hollow plastic packaging such as bottles, drums, and intermediate bulk containers (IBCs), making it suitable for holding liquids and chemicals. Extrusion is a continuous process that generates long, uniform packaging items like plastic films, sheets, and flexible wraps, which are frequently used in protective and stretch packaging. Thermoforming consists of heating a plastic sheet and shaping it into a designated form using a mold, and is extensively used for trays, clamshells, and other rigid or semi-rigid packaging types. Each manufacturing technique presents distinct benefits in terms of cost, speed, design flexibility, and appropriateness for various packaging requirements, allowing manufacturers to serve a broad spectrum of industrial applications.

Packaging Type: Market Insights

The global industrial packaging market is categorized by packaging type into rigid packaging and flexible packaging. Rigid packaging encompasses containers such as drums, boxes, crates, pallets, and cans, offering strong structural integrity and safeguarding for high-value or heavy-duty goods. This type is commonly utilized in industries such as chemicals, automotive, construction, and pharmaceuticals, where durability, impact resistance, and safe stacking are crucial. Flexible packaging consists of materials like sacks, bags, films, and wraps that easily adapt to the shape of the product. This type provides advantages such as lightweight handling, cost-effectiveness, and efficient storage, making it suitable for packaging powdered or granular materials, agricultural items, and lightweight industrial products. The decision between rigid and flexible packaging is influenced by factors like product weight, handling conditions, transportation requirements, and environmental concerns.

End Use: Market Insights

The global industrial packaging market is divided by end use into several segments: food and beverage, building and construction, consumer goods and cosmetics, chemicals and petrochemicals, pharmaceuticals, automotive, agriculture, electronics, and others. The food and beverage segment is significant, necessitating hygienic, tamper-proof, and bulk packaging for processed foods, drinks, and ingredients. The building and construction sector depends on strong packaging to transport heavy materials such as cement, adhesives, tiles, and tools. The consumer goods and cosmetics segment require attractive and durable packaging for household products and personal care items, often merging practicality with branding efforts. Chemicals and petrochemicals utilize specialized containers like drums and intermediate bulk containers (IBCs) for the safe storage and transport of hazardous or corrosive substances. Pharmaceuticals need secure, contamination-resistant packaging to ensure product integrity and adhere to stringent health regulations. The automotive sector involves packaging for parts, lubricants, and batteries, frequently calling for robust, reusable solutions. In agriculture, sacks, crates, and bulk containers are used for seeds, grains, fertilizers, and pesticides. Electronics packaging emphasizes anti-static and shock-absorbing materials to safeguard sensitive components during transportation.

Regional: Market Insights

The Asia Pacific region leads the global industrial packaging sector, holding the largest market share, primarily due to its robust industrial infrastructure, economic growth, and swift urban development. Nations like China, India, Japan, and South Korea play significant roles, providing a mix of high manufacturing capacity, cost-effective labor, and advantageous trade regulations that boost the demand for packaging.

In China, known as the world’s largest manufacturing center, there is a considerable demand for industrial packaging across sectors like electronics, chemicals, and heavy machinery. The “Made in China 2025” initiative is driving innovation and modernization within manufacturing, which subsequently heightens the need for advanced packaging solutions. Currently, India’s rapidly growing construction, automotive, and fast-moving consumer goods sectors, combined with government-led infrastructure initiatives such as ‘Make in India’, are greatly increasing domestic demand for industrial packaging.

The chemical and petrochemical sectors in the region, notably in China and Southeast Asia, require robust packaging solutions for bulk transportation and storage. Additionally, the increasing exports of electronics, textiles, and automotive parts from Asia Pacific necessitate secure and efficient packaging for international shipping.

Furthermore, the growth of e-commerce, along with improvements in warehousing and logistics infrastructure, is enhancing the demand for both flexible and rigid packaging options that can accommodate bulk distribution while ensuring product safety. The movement towards sustainable and recyclable materials is also shaping packaging innovations throughout the region. Along with a large consumer base, substantial industrial production, and rising foreign investments position the Asia Pacific as the most significant and rapidly expanding region in the global industrial packaging arena.

Competition: Industrial packaging

The global industrial packaging sector is fiercely competitive, with top companies prioritizing innovation, product effectiveness, sustainability, and strategic collaborations to enhance their market presence and secure a competitive advantage. These organizations are investing in advanced materials, smart packaging technologies, and recyclable options to address the changing needs of end-use industries and adhere to environmental regulations. Key players in the global industrial packaging market include Mondi Group, International Paper Company, Greif, Inc., Amcor Plc, Mauser Packaging Solutions, Berry Global Inc., and Sonoco. These firms continuously adjust to market trends by emphasizing recyclability, automation, and digital integration in packaging to efficiently meet industrial requirements while minimizing environmental impact.

Berry Global Inc., based in the United States, is a significant entity in the worldwide industrial packaging sector, providing a wide array of rigid and flexible plastic packaging options for various industries, including chemicals, automotive, construction, and agriculture. Berry is committed to delivering high-quality packaging that addresses the needs for durability, protection, and sustainability. The company is well-regarded for its innovations in lightweight materials, barrier films, and recyclable packaging, with a firm dedication to achieving 100% recyclable, reusable, or compostable packaging by 2025. Its acquisition of RPC Group has enhanced its global presence and capabilities in rigid packaging. Berry’s extensive scale, technical knowledge, and focus on sustainability and customization establish it as a vital player in meeting the changing demands of the industrial packaging industry.

GLOBA INDUSTRIAL PACKAGING MARKET SNAPSHOT | |

Market size in 2024 | USD 66 Billion |

Market forecast in 2032 | USD 99 Billion |

Compound Annual Growth Rate (2025-2032) | 5.1% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Growth Drivers | Growth in manufacturing & industrial activities, Sustainability trends & regulatory push, Globalization of trade & e-commerce, Increased demand from food & beverage sector |

Segments Covered | Product Type, Material Type, Manufacturing Technique, Packaging Type, End Use, And Region |

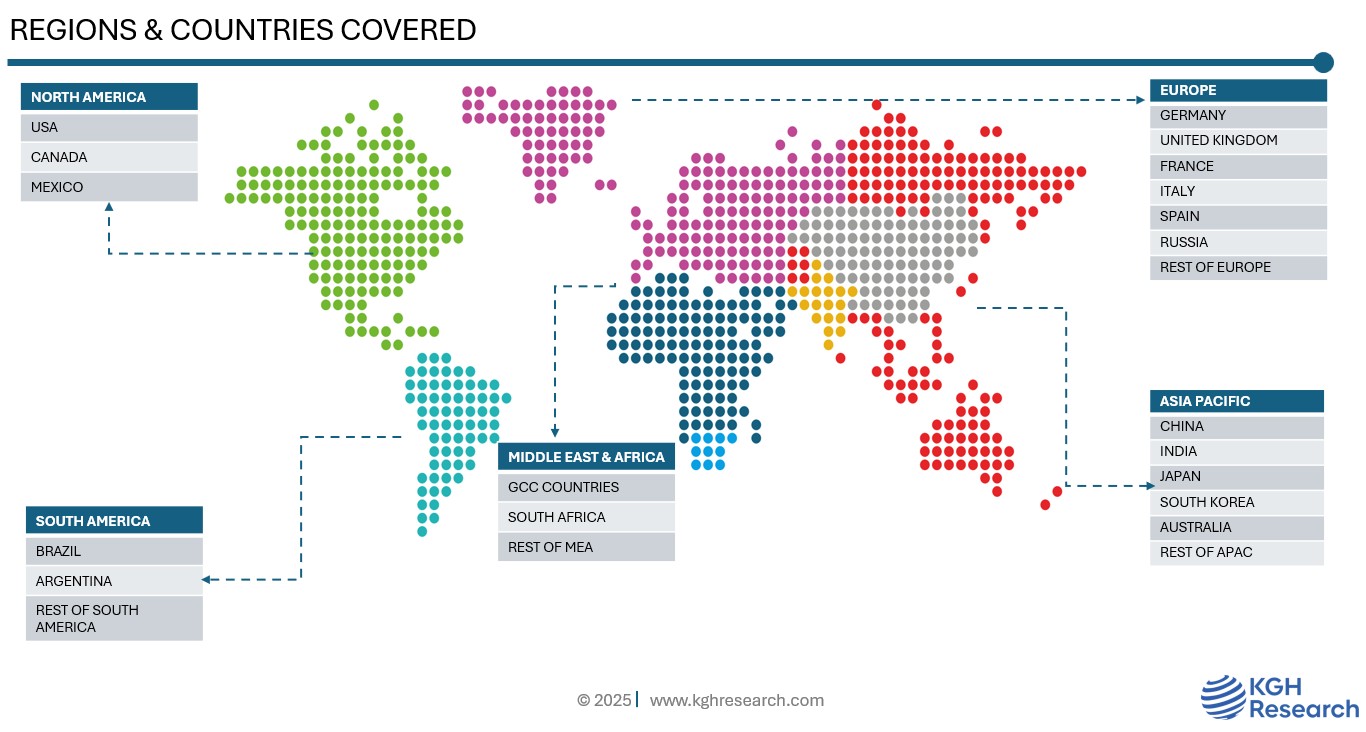

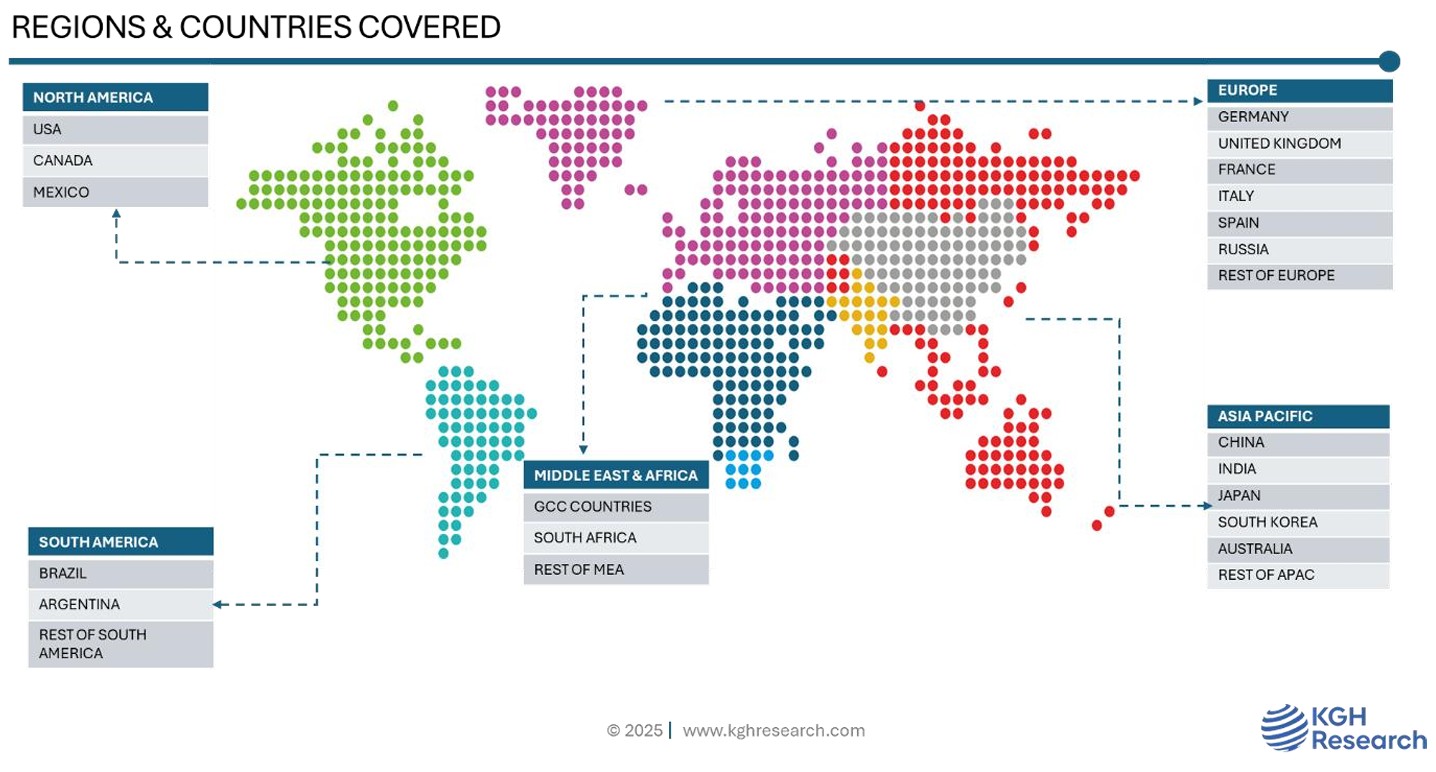

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, France, Spain, Russia, China, India, Japan, South Korea, Australia, South Africa, Brazil, Argentina |

Companies Profiled | BERRY GLOBAL, AMCOR LIMITED, BAG CORP, CHEM-TAINER INDUSTRIES, EAST INDIA DRUMS & BARRELS, SEALED AIR, INTERNATIONAL PAPER, SMURFIT WESTROCK PLC, MONDI, JUMBO BAG, NEFAB, HOOVERS CONTAINER SOLUTIONS, ORORA PACKAGING AUSTRALIA, SONOCO PRODUCTS COMPANY, SCHÜTZ GMBH & CO, GREIF, WESTROCK COMPANY, AMERIGLOBE, MAUSER, CORRPAKBPS, LC PACKAGING, AND MANY MORE |