Data Center Power Infrastructure Market (2022 - 2035)

DATA CENTER POWER INFRASTRUCTURE MARKET SIZE & SHARE BY COMPONENT (GENERATORS, UPS, POWER DISTRIBUTION UNIT & BUSWAYS, AND SWITCHGEARS, BY DATA CENTER TYPE (HYPERSCALER, COLOCATION, AND ENTERPRISE), BY WORKLOAD (AI BASED, NON-AI BASED), BY SOLUTION & SERVICES, BY END USE, BY HARDWARE, SOFTWARE, AND SERVICE, BY INSTALLATION (FIRST FIT AND REPLACEMENT), AND BY REGIONS & KEY COUNTRIES – FORECAST TO 2035

| Report Code: ICT7002-0602 | Number of Pages: 300 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: SEPTEMBER 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

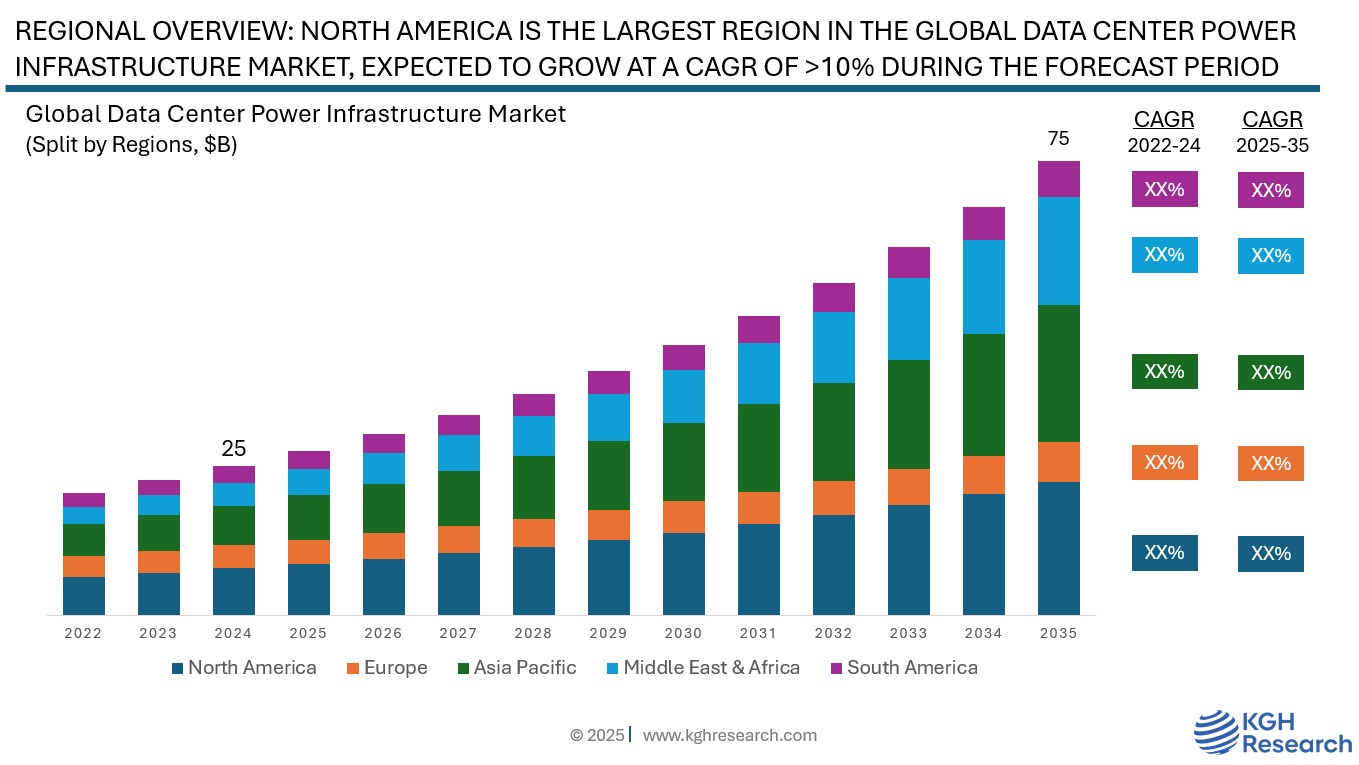

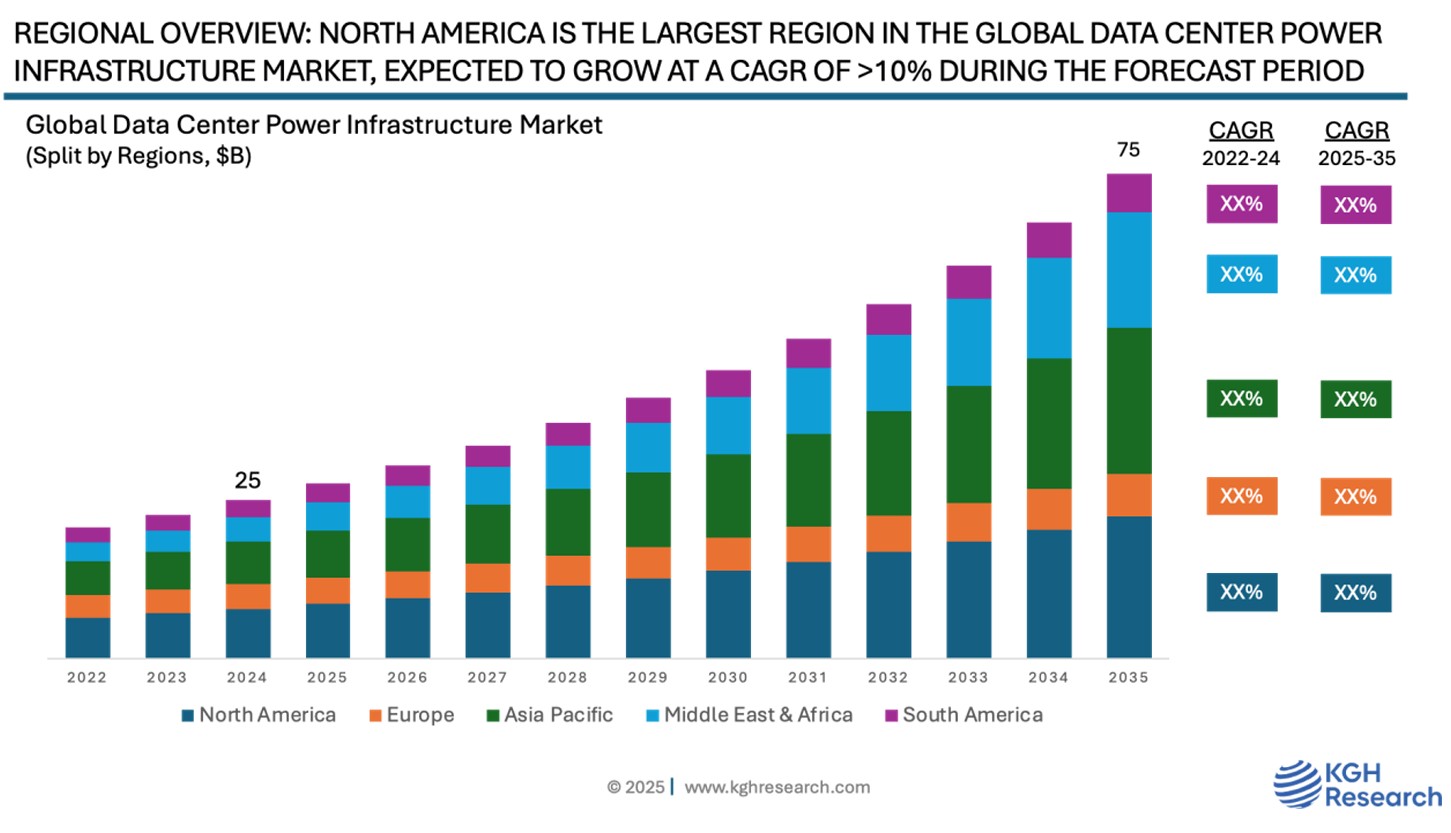

Market Overview: The global data centre power (infrastructure) market is estimated at US $25 Bn (incl. replacement/refresh spending) in 2024, and this market is expected to grow at a CAGR (2025 – 2035) of more than 10% to become USD 75 Bn market opportunity by 2035 The growth is attributed to two prime drivers, that are increasing deployments of compute heavy AI based mega data centers, globally and increasing data center installation worldwide. Data centre power equipment, including PDUs (Power Distribution Units), switchgears, generators, and UPS (Uninterruptible Power Supplies), are critical for ensuring reliable, efficient, and uninterrupted power delivery. The rapid growth of cloud computing, big data analytics, and AI-driven applications are key growth drivers, increasing the demand for resilient power solutions to support 24/7 operations. Additionally, the push for energy efficiency and sustainability has led to innovations in advanced UPS systems and smart PDUs that optimize power usage. The rise of edge computing and hyperscale data centres further drives the need for scalable, high-capacity power equipment capable of handling dynamic workloads while minimizing downtime and energy costs. A typical investment on power infrastructure could cost in between US $1.5 to $2.5 Million per MW IT Load within a data centre.

MARKET DYNAMIC

GROWTH DRIVERS:

- The global data center market is expected to grow at >10% CAGR during the next 10 years, driving huge investment on DC infrastructure

- Increasing adoption of Generative & Specialized AI is driving huge investments on infrastructure in the AI based mega data center

- Driver 3: Refer Report

- Driver 4: Refer Report

- Driver 5: Refer Report

NEW GROWTH OPPORTUNITIES:

- The specialized chips and dense architectures at the heart of AI data centers likely to remain the key driver for the market growth during the forecast period

- Increasing rack density to meet the demand for compute heavy workloads driving demand for expensive, but highly reliable liquid cooling solutions

- Waste heat energy recovery from data center in district heating, power generation, and agriculture to add new revenue stream for infrastructure providers & DC owners & Operators

MARKET RESTRAINTS:

- With growing data center installation around the world, the energy demand is growing exponentially. Huge investment is needed in the energy generation industry to keep up with the pace of data center growth

- Market Restrainer 2: Refer Report

- Market Restrainer 3: Refer Report

GROWTH HURDLES:

- Regulatory pressure to reduce excessive heat generation, water usage, and green house gas emission from data center and ancillary industries supporting data centers putting immense pressure on data center owners & operators and infrastructure providers, globally

- Growth Hurdle 2: Refer Report

- Growth Hurdle 3: Refer Report

Market Insights

Generators:

The global data centre generators market was valued at US $6.5 Billion in 2024 (incl. aftermarket services, fuel tank, fuel pump, other ancillary products, installation cost, and replacement) and is expected to grow at a CAGR of (2025 – 2035) of >10% to become US $18 Billion opportunity by 2035. For example, a typical 10 MW data centre would require an investment on US $6 to $8 Million in setting up 10 MW worth of power generators on-site to ensure 99.99% uptime for clients.

Diesel generators are predominantly used in the market with more than 98% share of the market, KGH research suggests that there has been a growing demand for generators that are not only energy efficient but are also ecofriendly with lower carbon footprint, thus driving demand for alternative fuel generators running on HVOs and other biofuels. At the same time there are companies working on commercializing fuel cell based generators for scalable operation within data centres.

Uninterrupted Power Supply (UPS):

The global data centre uninterrupted power supply (UPS) market was valued at US $8.0 Billion (including new installation & replacement) in 2024 and is expected to grow at a CAGR of (2025 – 2035) of >10% to become US $20 Billion opportunity by 2035. New Installation accounted for approx. 3/5th of the global DC UPS market, while replacement accounted for the remaining share. Data Centre owners / operators usually replaces the UPS systems in every 10 years, thus driving replacement market demand. UPS systems deliver short-term backup power, typically lasting 15 to 30 minutes—in the event of a power outage, bridging the gap until backup generators become fully operational. As a result, the size of the UPS battery array is directly proportional to the electrical load it supports within the data centre.

An Uninterruptible Power Supply (UPS) system delivers automated backup power to ensure continuous operation of data centres during electrical outages. Beyond backup capabilities, UPS systems also provide power conditioning by regulating voltage fluctuations, addressing under- or over-voltage situations, and stabilizing frequency variations. Our primary focus is on the large-scale UPS segment, which is particularly relevant to data centre environments.

Switchgears:

The global data center switchgears market was valued at US $5.5 Billion in 2024 (incl. switches, fuses, isolators, relays, and circuit breakers) and is expected to grow at a CAGR of (2025 – 2035) of >10% to become US $16.5 Billion opportunity by 2035. This sustained investment in IT infrastructure, particularly in areas like AI/ML, cloud computing, and edge deployments, underscores the increasing power demands within data centres and the consequent need for reliable and advanced power distribution solutions, including sophisticated switchgear systems. Switchgear is a critical component in power distribution systems, designed to control, protect, and isolate electrical equipment. Key components include circuit breakers, fuses, disconnect switches (isolators), and protective relays. In data centers, two main types of switchgear are commonly used: medium-voltage switchgear, which manages incoming utility power before it passes through the step-down transformer, and low-voltage switchgear, which distributes power to downstream systems, including uninterruptible power supply (UPS) batteries. This layered setup ensures reliable power management, fault protection, and operational continuity for mission-critical infrastructure.

Power Distribution Units & Busways:

Traditionally, electrical power flowed from the UPS system to power distribution units (PDUs), which included components like circuit breakers, power monitoring panels, meters, and cabling to each rack. However, PDUs have some drawbacks—they occupy valuable floor space in the data hall and produce waste heat. In high-density data centers, busway systems offer an alternative. Mounted overhead, busways deliver power to racks via plug-in units with built-in breakers and draw power directly from low-voltage switchgear. While busways free up floor space, they tend to be more costly to install and less adaptable to changes in rack layout.

Rack power distribution units (rPDUs) are installed directly on the racks and serve as the final link in the power distribution chain to IT equipment. They supply power outlets for servers, storage devices, and networking gear. In Tier 3 and Tier 4 data centres, each rack typically includes two rPDUs to ensure redundancy and continuous power availability.

Regional: Market Insights

North America continues to lead the global data center market accounted for almost 50% share of the new installations, with the U.S. and Canada driving significant investments. The region is projected to maintain a compound annual growth rate (CAGR) of approx. 10% from 2025 to 2035. Major hyperscale operators like Amazon Web Services, Microsoft, and Google are expanding their infrastructure to meet the growing demand for cloud services and AI applications.

Europe is expanding steadily, with a focus on energy efficiency and sustainability in data centre architecture. More money is being invested in colocation and modular data centres in nations like the UK, the Netherlands, and Germany. Data centre development is being influenced by the region’s emphasis on green technologies and adherence to strict data protection laws.

Asia Pacific is also experiencing significant growth, and is likely to become the second largest region after North America in terms of cumulative installations during the forecast period. The data center boom in Asia Pacific is being fuelled by how fast the region is going digital. With more people online than anywhere else in the world, especially in countries like China, India, and across Southeast Asia, there’s a massive need for reliable, high-speed infrastructure. Cloud adoption is skyrocketing as businesses modernize, and tech giants like AWS, Google, and Alibaba are racing to build out their networks. At the same time, 5G is rolling out across places like Japan and South Korea, pushing the need for faster, more localized data processing—AI workloads, edge computing. Governments are also playing a big role, with initiatives like Digital India and smart city projects across the region making it easier for companies to invest and build. Even countries like Malaysia and Indonesia are stepping up, offering new opportunities as demand spreads beyond the traditional hubs like Singapore and Hong Kong.

The Middle East & Africa is quickly becoming a hotspot for data center growth, thanks to a wave of digital transformation sweeping across the region. Countries like the UAE, Saudi Arabia, and South Africa are leading the charge, investing heavily in cloud infrastructure, smart cities, and AI technologies. Global tech giants and local players alike are setting up data centers to meet the rising demand for digital services, driven by everything from online banking and e-commerce to video streaming and government digitalization efforts. What’s fuelling this momentum even more is strong government backing—think Vision 2030 in Saudi Arabia and the UAE’s digital economy strategies—plus improved connectivity through new undersea cables and better fiber networks. As internet penetration grows and more businesses move to the cloud, the region is positioning itself as a serious player in the global data center landscape.

Competition: Data Center Power Infrastructure

The Data center generators market is highly consolidated with top five players, namely Caterpillar, Cummins, ABB, Rolls Royce, and Generac Power Systems together accounted for more than 75% share of the market. HITEC Power, KOHLER, and YANMAR are some of the other important players in the DC generators market.

The data centre Uninterruptible Power Supply market is highly consolidated with top five players, namely Schneider Electric, Vertiv, ABB, Eaton, and Legrand together accounted for more than 60% share of the market. Ametek, General Electric, Fuji Electric, Belkin, Benning, Clary Corporation, and Emerson Electric are some of the other prominent players actively participating in the global DC UPS market.

The data center switchgears market is highly consolidated with top six players, namely Schneider Electric, ABB, Vertiv, Eaton, Siemens, and Legrand together accounted for more than 90% share of the market.

The global Data Centre Power Distribution Unit market is highly consolidated with top six players, namely Vertiv, Schneider Electric, Eaton, Legrand, ABB, and Siemens together accounted for more than 85% share of the market.

GLOBAL DATA CENTRE POWER INFRASTRUCTURE MARKET SNAPSHOT | |

Market size in 2024 | USD 25 Billion |

Market forecast in 2035 | USD 75 Billion |

Compound Annual Growth Rate (2025-2032) | >10% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2035 |

Growth Drivers | Growing Data Center Market, Increasing Deployments of Generative AI and Specialized AI based Data Centers |

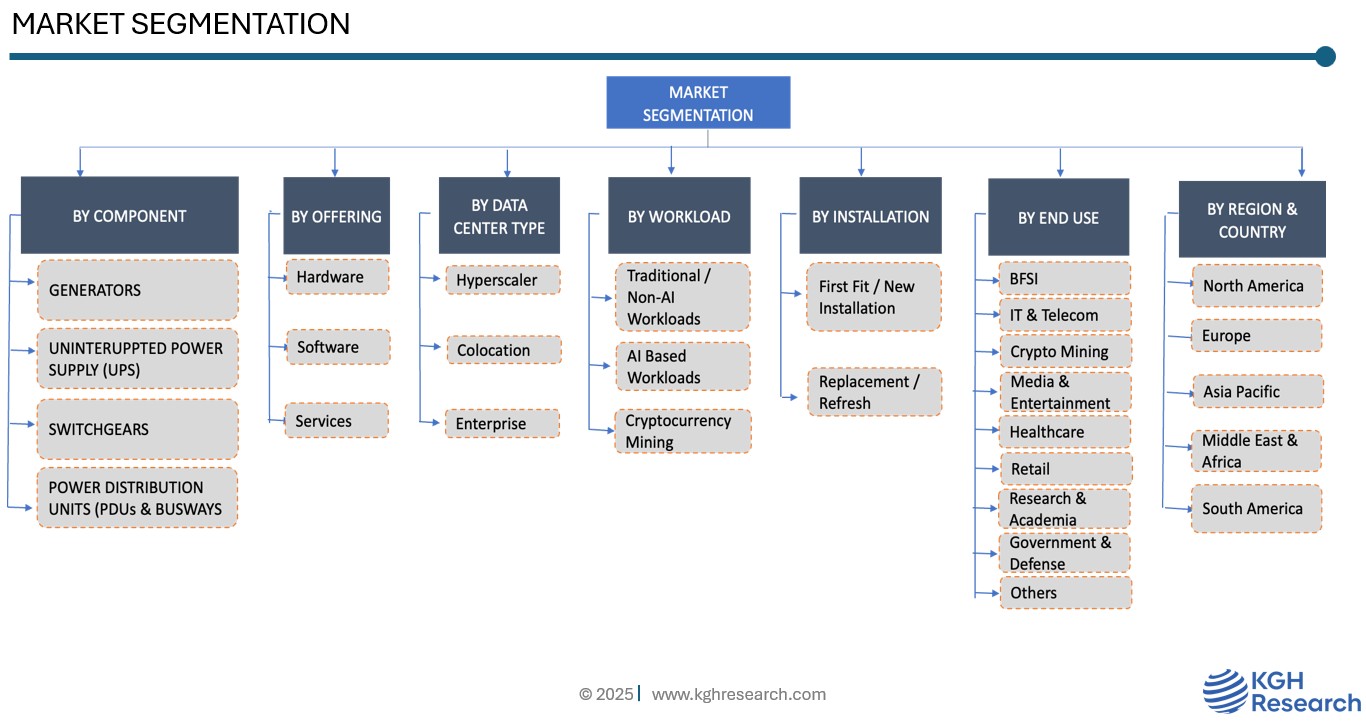

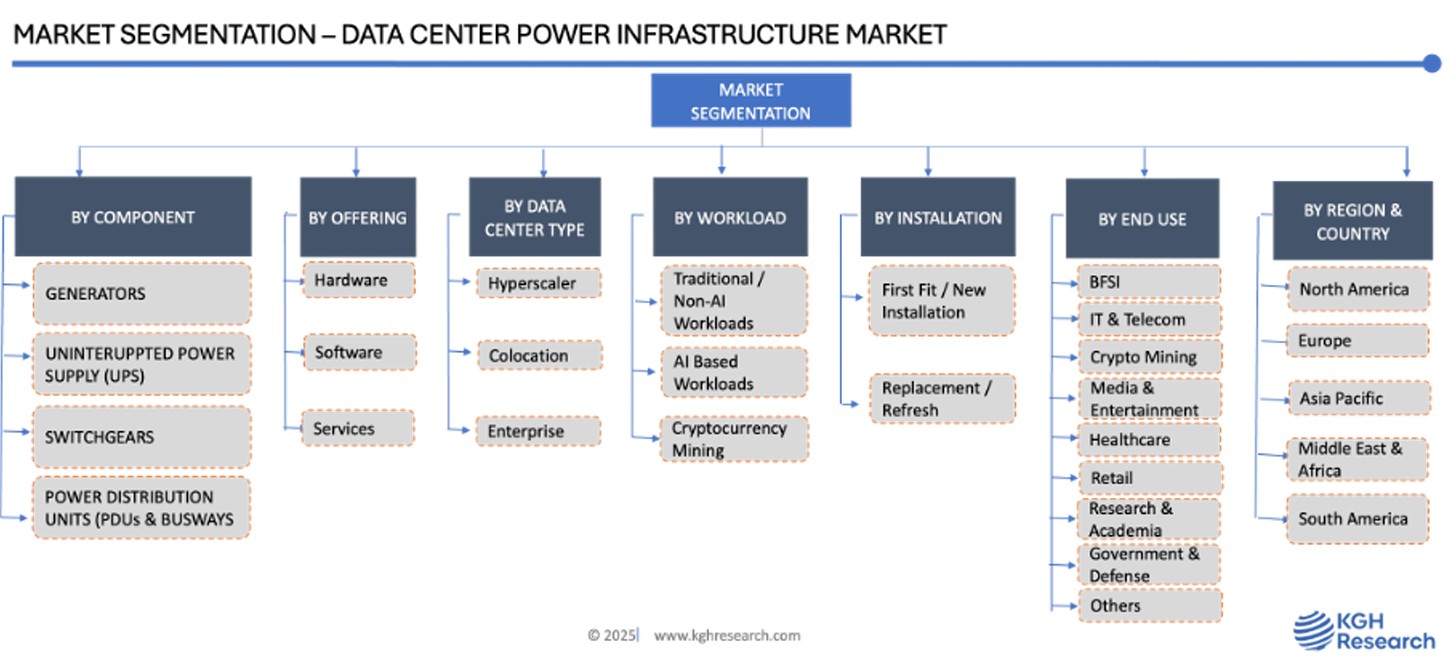

Segments Covered | Component Type, Offering, Data Center Type, Workload, Installation, End Use, and By Region and Countries |

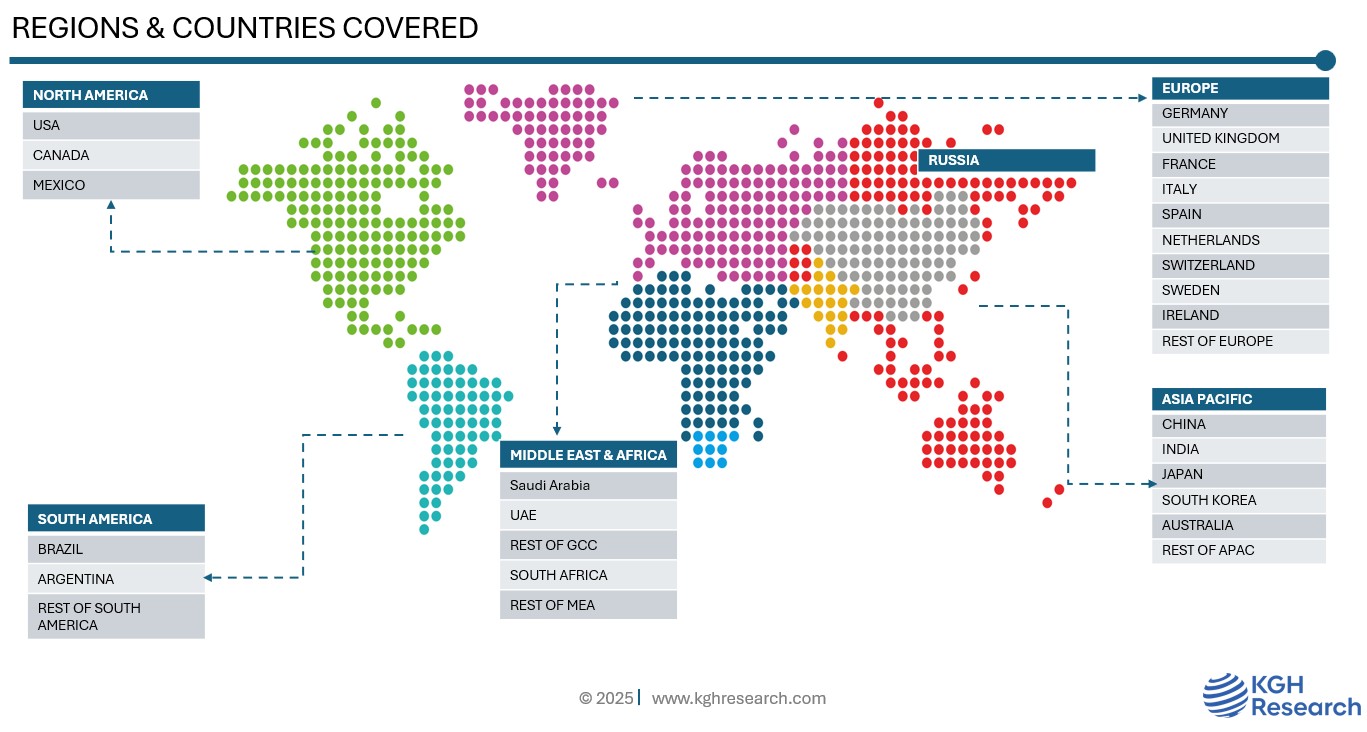

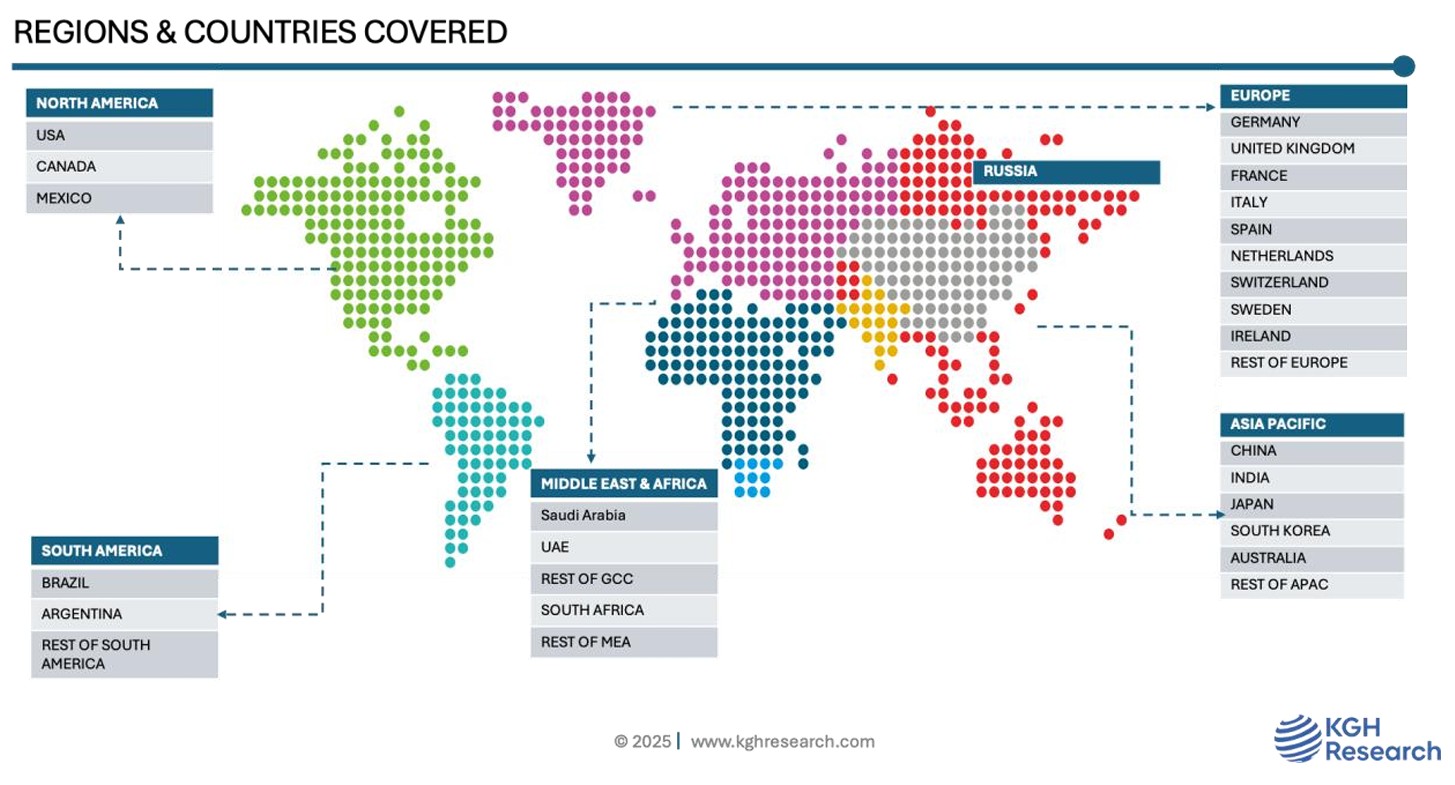

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK Germany, France, Italy, Ireland, Sweden, Netherlands, Switzerland, Spain, Russia, China, India, Japan, Singapore, South Korea, Thailand, Indonesia, Australia, Malaysia, Saudi Arabia, UAE, South Africa, Brazil, Argentina, and Rest of the World |

Companies Profiled | Caterpillar, Cummins, ABB, Rolls Royce, Generac Power Systems, HITEC Power, Kohler, Yanmar, Schneider Electric, Vertiv, ABB, Eaton, Legrand, Ametek, General Electric, Fuji Electric, Belkin, Benning, Clary Corporation, Emerson Electric, Siemens, and Many More |