Solid Oxide Fuel Cell Market (2022 - 2032)

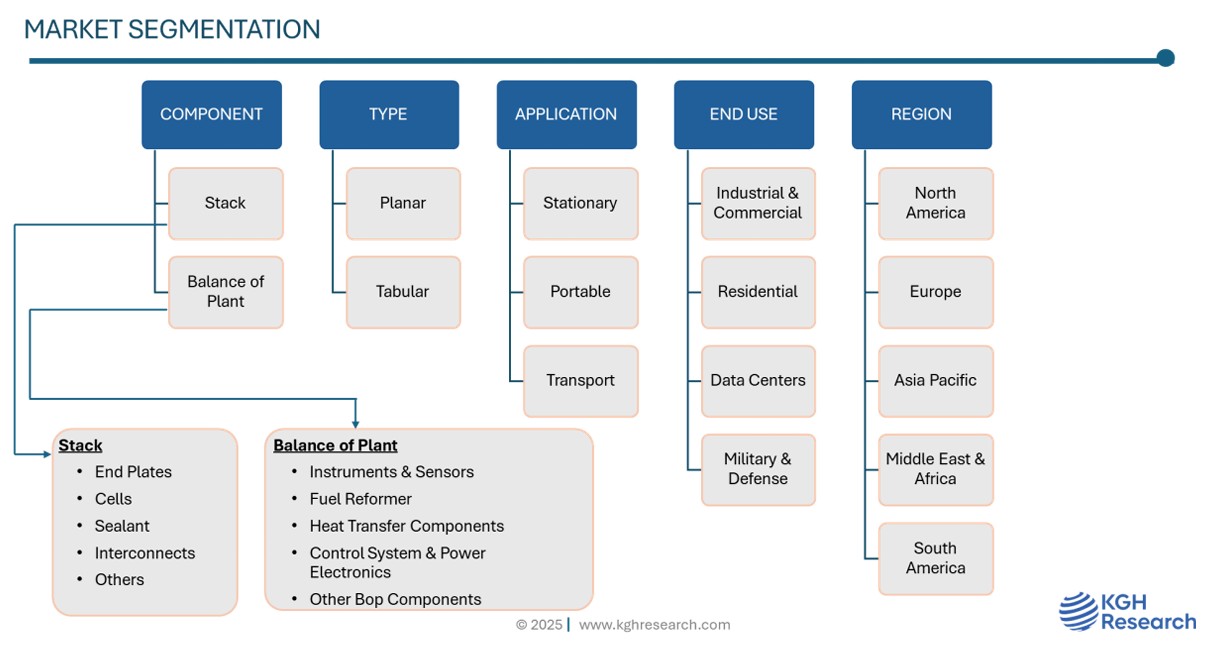

SOLID OXIDE FUEL CELL MARKET SIZE & SHARE BY COMPONENT (STACK, BALANCE OF PLANT), BY TYPE (PALNAR, TABULAR), BY APLICATION (STATIONARY, PORTABLE, TRANSPORT), END USE (INDUSTRIAL & COMMERCIAL, RESIDENTIAL, DATA CENTERS, MILITARY & DEFENSE) AND BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: E&P4015-0102l | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: SEPTEMBER 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

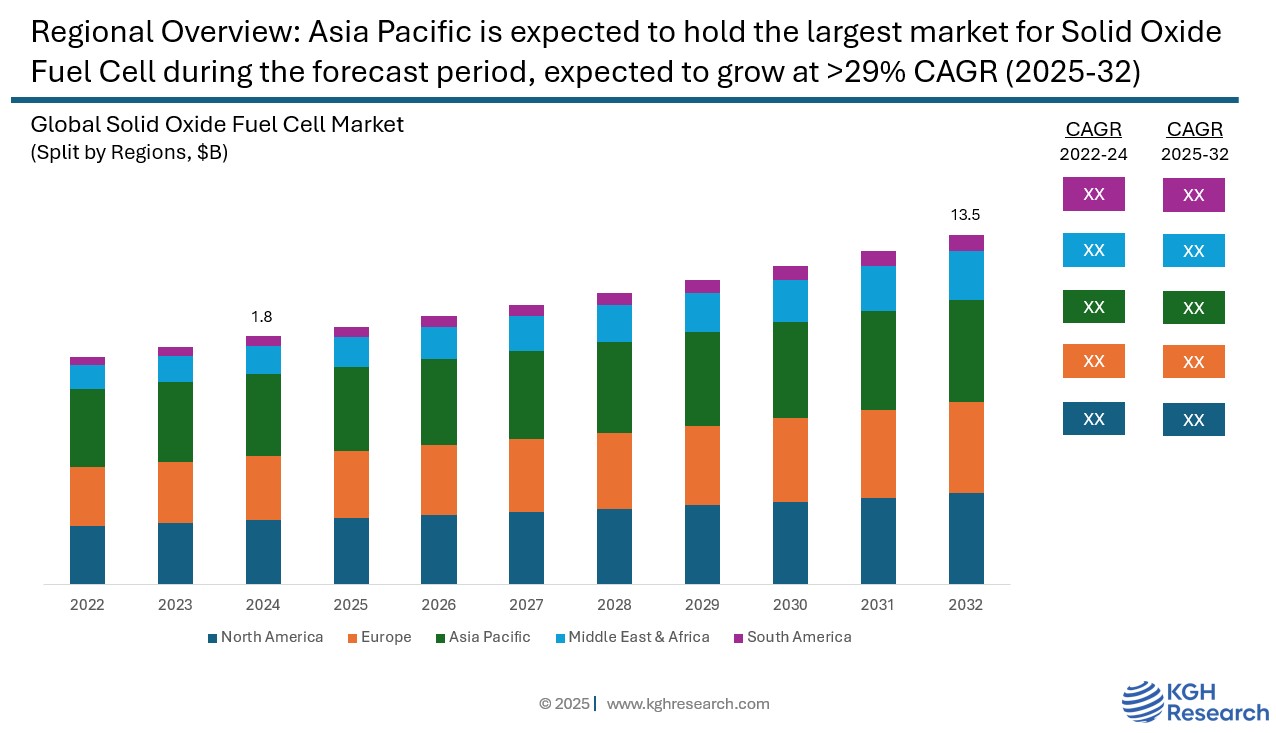

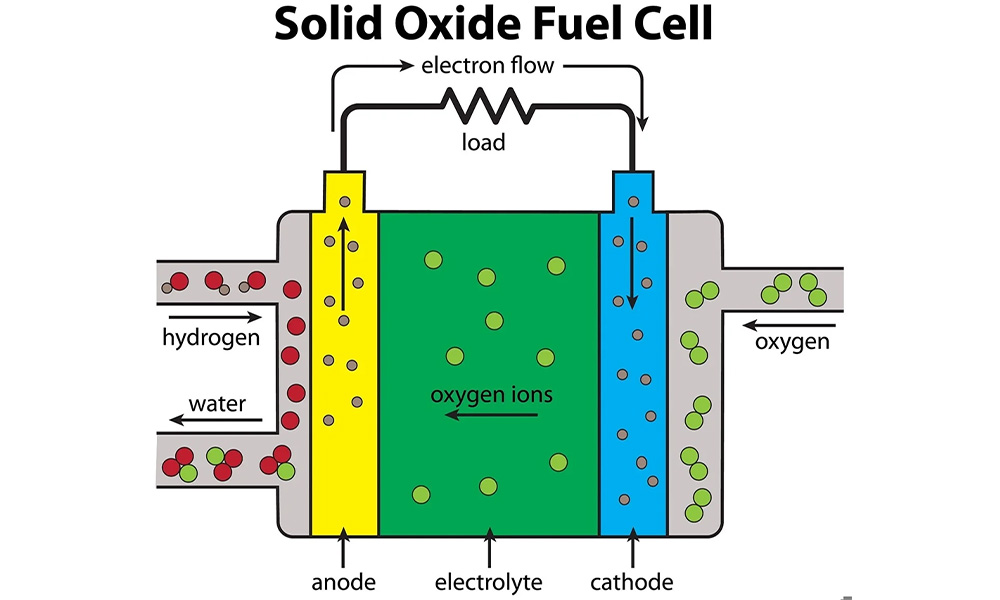

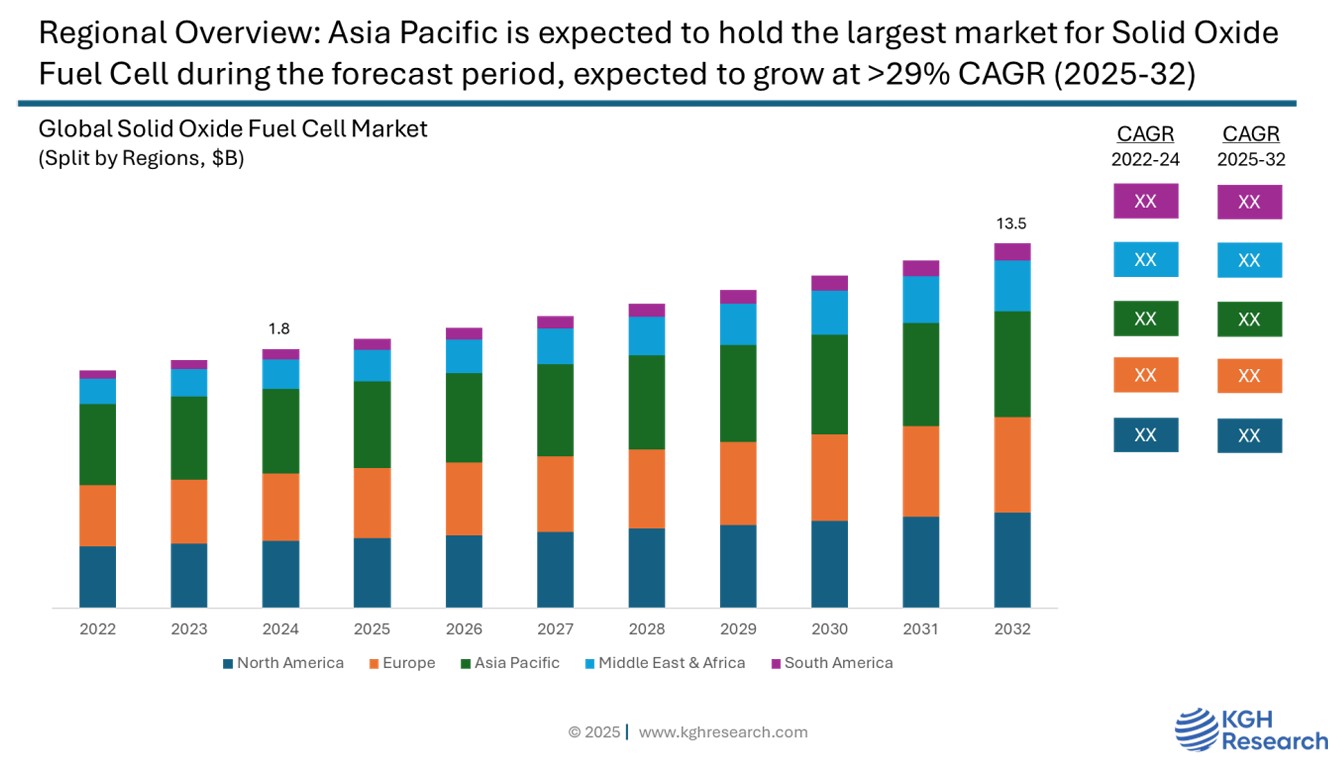

Market Overview: The global solid oxide fuel cell market was valued at approximately USD 1.8 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 28.5% from 2025 to 2032. The market is driven by by the global shift toward clean, efficient, and low-emission energy technologies. SOFCs offer high electrical efficiency and fuel flexibility, capable of operating on hydrogen, natural gas, biogas, and other hydrocarbons—making them suitable for both transitional and future energy systems. Growing demand for distributed power generation, particularly in industrial & commercial, residential, data centres applications, is fuelling adoption due to SOFCs’ ability to provide reliable, long-duration power with minimal environmental impact.

MARKET DYNAMIC

GROWTH DRIVERS:

- Growing demand for low-emission, clean and decentralized energy solutions

- Incentives, subsidies, and R&D funding from governments worldwide are fostering SOFC technology development

- Increasing investments in hydrogen infrastructure

- SOFCs offer superior electrical efficiency and can operate on a variety of fuels, making them adaptable for diverse applications.

NEW GROWTH OPPORTUNITIES:

- Ongoing R&D into cost-effective, durable ceramic materials and metal-supported cells

- Integration with renewable energy

- Increased use of SOFCs in microgrids, remote power systems, and critical infrastructure offers new deployment potential

- Expanding demand for efficient home energy solutions

- Increasing energy consumption in data centres

MARKET RESTRAINTS:

- High capital and operational costs

- Slow start-up time, as SOFCs operate at very high temperatures which results in longer warm-up periods

- Durability issues

GROWTH HURDLES:

- Competition from alternative fuel cell technologies

- Hydrogen infrastructure lag

- Scalability and standardization issues

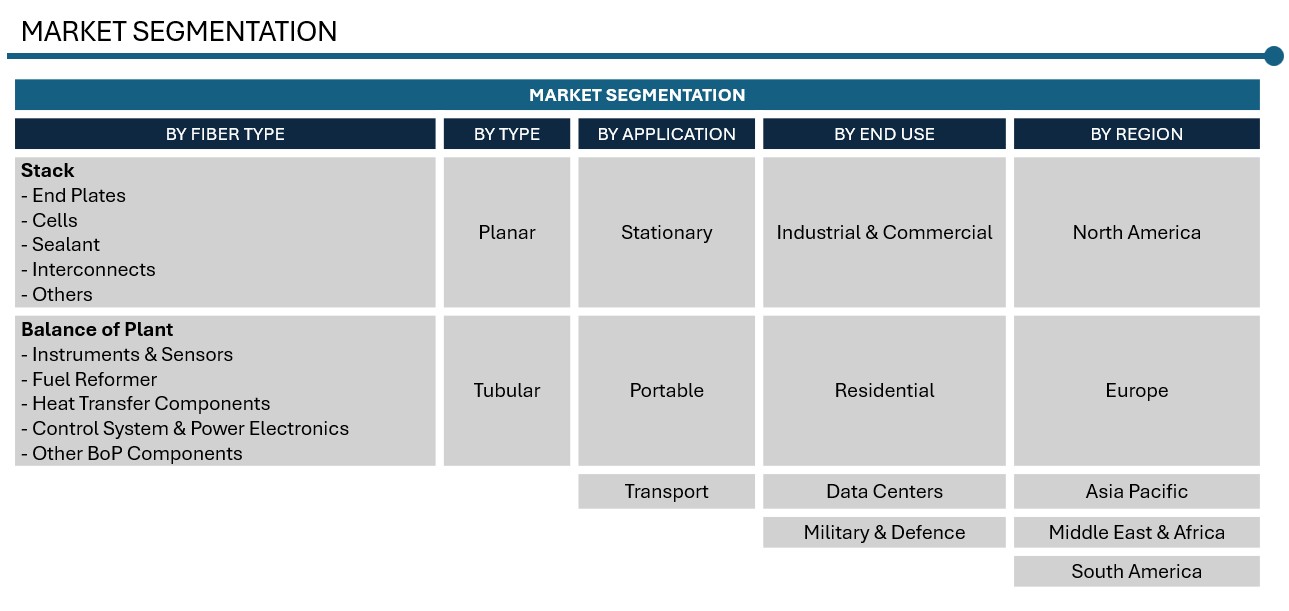

Component: Market Insights

In the solid oxide fuel cell market, components are mainly categorized into the stack and the balance of plant (BoP). The stack segment accounts for the largest market share, as it forms the heart of the system where electrochemical reactions take place, directly affecting the cell’s efficiency and power output. It’s also the most complex and expensive part, attracting major investments and research. On the other hand, the balance of plant includes supporting components like fuel processors, heat exchangers, pumps, blowers, and control systems. Although crucial for the overall functioning of the system, BoP makes up a smaller share of the market in terms of value.

Type: Market Insights

By type, the planar solid oxide fuel cell (SOFC) is expected to hold the largest share of the market during the forecast period. This dominance is due to its relatively simple design, ease of stacking, high power density, and better scalability for various applications such as stationary power. The planar configuration allows for efficient heat management and compact system integration, making it a preferred choice for commercial deployment over other types like tubular SOFCs.

Application: Market Insights

By type, the global solid oxide fuel cell market is segmented into stationary, portable, and transport. The stationary segment holds the largest share in the solid oxide fuel cell (SOFC) market. This is primarily due to the high demand for reliable, efficient, and low-emission power generation in residential, commercial, and industrial settings. Stationary SOFCs are widely used for data centres, and off-grid power applications. Their ability to provide continuous power with high fuel efficiency and lower environmental impact makes them ideal for stationary use, compared to portable or transport applications, which are still in earlier stages of commercialization.

End Use: Market Insights

The solid oxide fuel cell (SOFC) market is broadly segmented by end use into commercial & industrial, residential, military & defense, and data centers. Among these, the commercial & industrial sector leads the adoption of SOFC technology, driven by increasing demand for efficient, low-emission, and decentralized power generation. These systems are particularly valuable in applications that benefit from combined heat and power (CHP) capabilities, offering both economic and environmental advantages. The residential segment is growing steadily, especially in countries like Japan and South Korea, where government support and compact fuel cell solutions are making home energy systems more viable. In military and defense applications, SOFCs are valued for their fuel flexibility, silent operation, and ability to provide reliable off-grid power in challenging environments. Data centers are an emerging growth area and is expected to be the fastest growing segment during the forecast period due to their need for constant, clean, and resilient power, with SOFCs offering a stable alternative to traditional backup systems. Each segment reflects unique needs and adoption trends, contributing to the overall expansion of the SOFC market.

Regional: Market Insights

Asia-Pacific is expected to hold the largest share of the solid oxide fuel cell (SOFC) market during the forecast period, driven by a combination of supportive government policies, increasing investments in clean energy technologies, and rising energy demand across major economies such as Japan, South Korea, China, and India. Japan and South Korea are at the forefront, with strong initiatives promoting fuel cell adoption for both residential and commercial use, including government-subsidized programs like Japan’s ENE-FARM. The region’s focus on reducing carbon emissions, enhancing energy security, and promoting decentralized power generation has further accelerated the deployment of SOFC systems. Additionally, the presence of leading market players, advancements in manufacturing capabilities, and ongoing research and development activities are contributing to the region’s dominance. The rapid pace of urbanization, industrialization, and the shift toward sustainable energy infrastructure in Asia-Pacific are expected to sustain and expand its leadership in the global SOFC market.

China is poised to become a dominant force in the solid oxide fuel cell (SOFC) market, driven by a combination of rapid industrial growth, strong government support, and a clear national commitment to clean energy. The country has set ambitious climate goals, including peaking carbon emissions by 2030 and achieving carbon neutrality by 2060, which are fueling large-scale investments in hydrogen and fuel cell technologies. China’s SOFC market is witnessing exponential growth, with projections indicating a surge from just over USD 4 million in 2022 to more than USD 100 million by 2030. The stationary segment, particularly for distributed power generation and combined heat and power (CHP) systems, leads the market due to rising demand from industrial and commercial sectors. Government-backed initiatives, including subsidies, infrastructure development, and a national hydrogen roadmap, are accelerating deployment. Additionally, significant advancements in domestic research and manufacturing capabilities are reducing system costs and improving efficiency, further strengthening China’s position. With expanding infrastructure, including hundreds of hydrogens refueling stations and supportive provincial-level policies, China is not only the fastest-growing SOFC market in Asia-Pacific but is also emerging as a global leader in fuel cell adoption and innovation.

Competition: Solid oxide fuel cell

The Solid oxide fuel cell market is highly competitive, with key players focusing on innovation, product efficiency, and strategic partnerships to strengthen their market position. Major companies include Mitsubishi Heavy Industries Ltd., Bloom Energy, Aisin Corporation, Kyocera Corporation, and Miura Co., Ltd. These players are investing in R&D to develop SOFC tailored for applications in industrial & commercial, residential, data centers, military & defense sectors, driving ongoing competition and technological advancement in the market.

Mitsubishi Heavy Industries Ltd., Bloom Energy, Aisin Corporation, Kyocera Corporation, and Miura Co. Ltd. are among the leading companies active in the market.

Mitsubishi Heavy Industries is one of the key players in the solid oxide fuel cell (SOFC) market, leveraging its strong engineering expertise and technological capabilities to drive innovation in clean energy solutions. The company, through its subsidiary Mitsubishi Power, has been actively developing and deploying SOFC systems, particularly for stationary power generation and combined heat and power applications. MHI’s SOFC systems are known for their high efficiency, low emissions, and suitability for commercial and industrial use. The company has collaborated with partners in Japan and globally to advance SOFC technology, including pilot projects and commercial installations that support energy decentralization and carbon reduction goals. Backed by a strong commitment to sustainability and clean energy transition, Mitsubishi Heavy Industries continues to invest in research and development and expand its presence in the global fuel cell market, reinforcing its position as a leading player in the SOFC space.

Bloom Energy, based in San José, California, has emerged as a global leader in solid oxide fuel cells (SOFCs) for stationary power generation. Its flagship product, the Bloom Energy Server, uses high-temperature SOFC technology to efficiently convert a variety of fuels—such as natural gas, biogas, hydrogen, or blends—into reliable, on-site electricity with high efficiency and low emissions. The company is also pushing the frontier of hydrogen-based SOFCs: it demonstrated 100% hydrogen-fueled SOFCs achieving ~60 % electrical efficiency and commercialized the world’s largest solid oxide electrolyzer system in partnership with NASA. Bloom maintains strategic partnerships—such as with SK ecoplant in South Korea, Sembcorp in Singapore, and collaborations with major data center operators like Intel and CoreWeave—to expand its footprint in mission-critical, clean-power applications. With its modular, fuel-flexible design and a business model offering both equipment sales and energy-as-a-service options, Bloom Energy is a standout innovator in commercializing SOFC technology for on-site, resilient, and low-carbon power generation.

SOLID OXIDE FUEL CELL MARKET PURVIEW | |

Market size in 2024 | USD 1.8 Billion |

Market forecast in 2032 | USD 13.5 Billion |

Compound Annual Growth Rate (2025-2032) | 28.5% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Market Drivers | Growing demand for low-emission, clean and decentralized energy solutions Incentives, subsidies, and R&D funding from governments worldwide are fostering SOFC technology development Increasing investments in hydrogen infrastructure SOFCs offer superior electrical efficiency and can operate on a variety of fuels, making them adaptable for diverse applications. |

Segments Covered | Component, Type, Application, End Use |

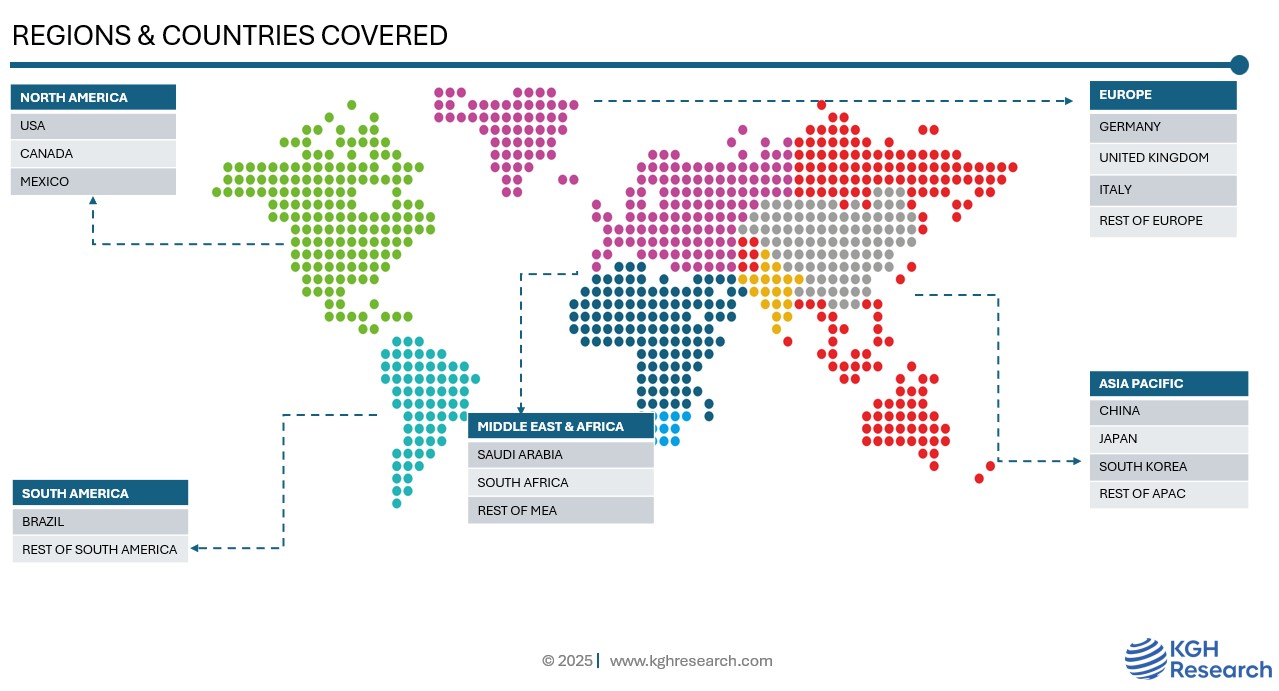

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, China, Japan, South Korea, South Africa, Saudi Arabia, Brazil |

Companies Profiled | ASIN CORPORATION, BLOOM ENERGY, CONVION, KYOCERA CORPORATION, MIURA CO., LTD., ADELAN, SOFCMAN, WATT FUEL CELL CORPORATION, ELCOGEN AS, MITSUBISHI HEAVY INDUSTRIES, LTD., SUNFIRE GMBH, SOLYDERA SPA, H2E POWER, EDGE AUTONOMY, CERES |