Data Center Liquid Cooling CDUs Market (2022 - 2035)

DATA CENTER LIQUID COOLING COOLANT DISTRIBUTION UNITS (CDUs) MARKET SIZE & SHARE BY COOLING TECHNOLGY (COLD PLATE COOLING AND IMMERSION COOLING), BY CAPACITY (UPTO 100 KW, 100 – 500 KW, and ABOVE 500 KW) BY PLACEMENT (ROW BASED, RACK BASED, AND FACILITY BASED), BY LOCATION (CENTRALIZED VERSUS DECENTRALIZED), BY DATA CENTER TYPE (HYPERSCALE, COLOCATION, AND ENTERPRISE) AND BY REGION & COUNTRY–FORECAST TO 2032

| Report Code: S&E6003-1401 | Number of Pages: 300+ | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: SEPTEMBER 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

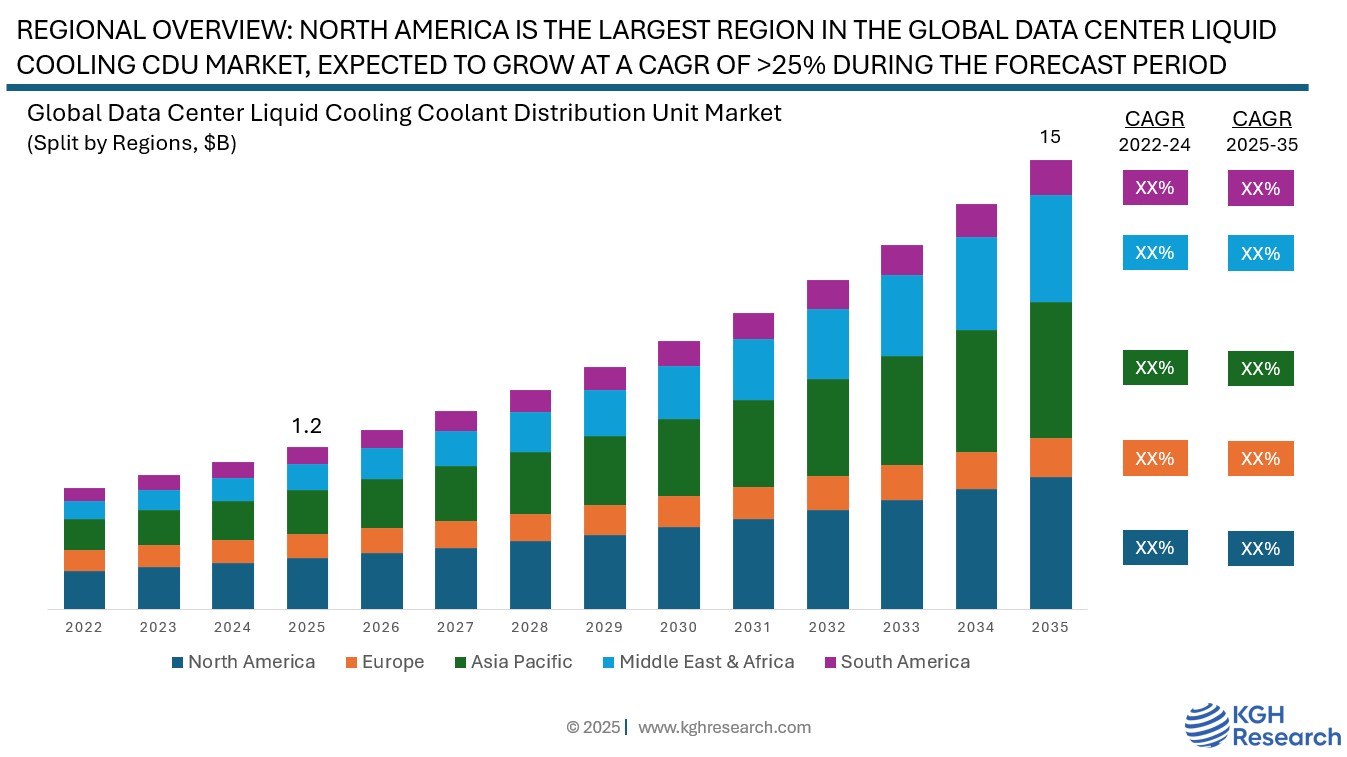

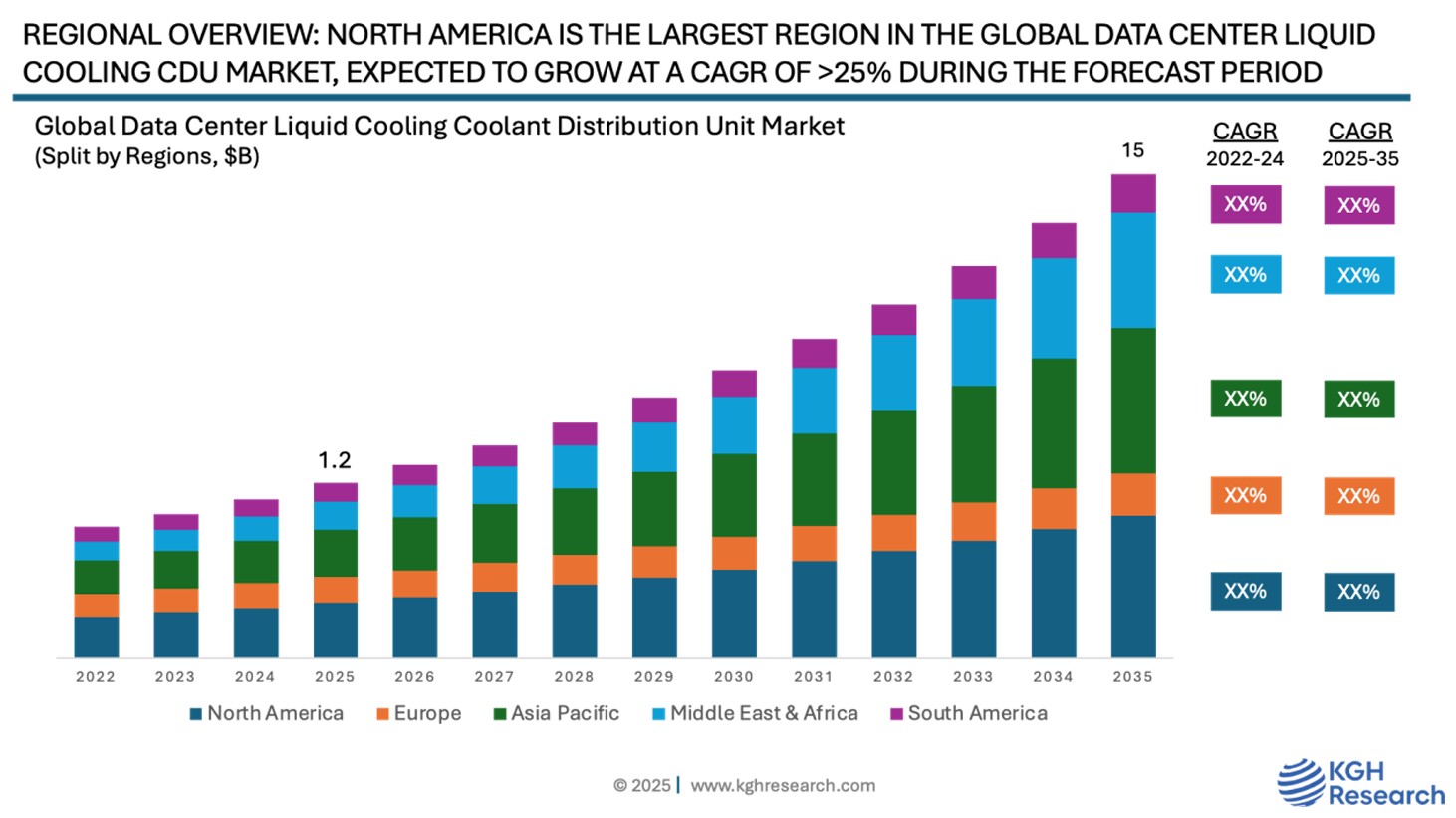

Market Overview: The global data center liquid cooling coolant distribution unit market was estimated at US $1.2 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of more than 25% from 2025 to 2035 to reach US $15 billion by 2035. The global data centre Coolant Distribution Unit (CDU) market is witnessing robust growth, driven by the surging adoption of liquid cooling technologies in high-density and hyperscale data centre environments. CDUs play a critical role in recirculating the coolant and regulating its temperature, making them indispensable in direct-to-chip, and immersion cooling systems. As traditional air-cooling systems struggle to manage rising heat loads, liquid cooling and efficient CDUs are emerging as vital components in ensuring thermal efficiency, space optimization, and sustainable operations.

Increasing data centre installations, globally, deployment of AI and high performance computing based workloads within data centres comprises of GPUs with thermal design power (TDP) potentially exceeding 1,500W per chip, and mounting pressure on data centre owners and operators to rethink their approach to cooling and energy efficiency driving wholesale switch towards liquid cooling technology in turn boosting the demand for CDUs.

MARKET DYNAMIC

GROWTH DRIVERS:

- Growing data center market – CAGR (2025 – 2032): >10%

- Increasing deployment of compute heavy AI based data centers –AI Data Center CAGR (2025 – 2035): >25%

- Driver 3

- Driver 4

- Driver 5

- Driver 6

NEW GROWTH OPPORTUNITIES:

- Innovations and technological advancements in AI powered compute heavy GPUs, the likes of NVIDIA GB200, RUBIN, AND RUBIN ULTRA with higher TDP (Thermal Design Power) ratings necessitating the deployment of liquid cooling technology

- Opportunity 2 – Development of PFAS free dual phase coolants

- Opportunity 3 –

- Opportunity 4 –

MARKET RESTRAINTS:

- Lack of standardization

- Supply chain bottlenecks, high lead time, critical component shortages

GROWTH HURDLES:

- Trade tensions, tariffs, and geopolitical instability likely to impact global supply chains, demand, production costs, and profitability of CDU and liquid cooling suppliers.

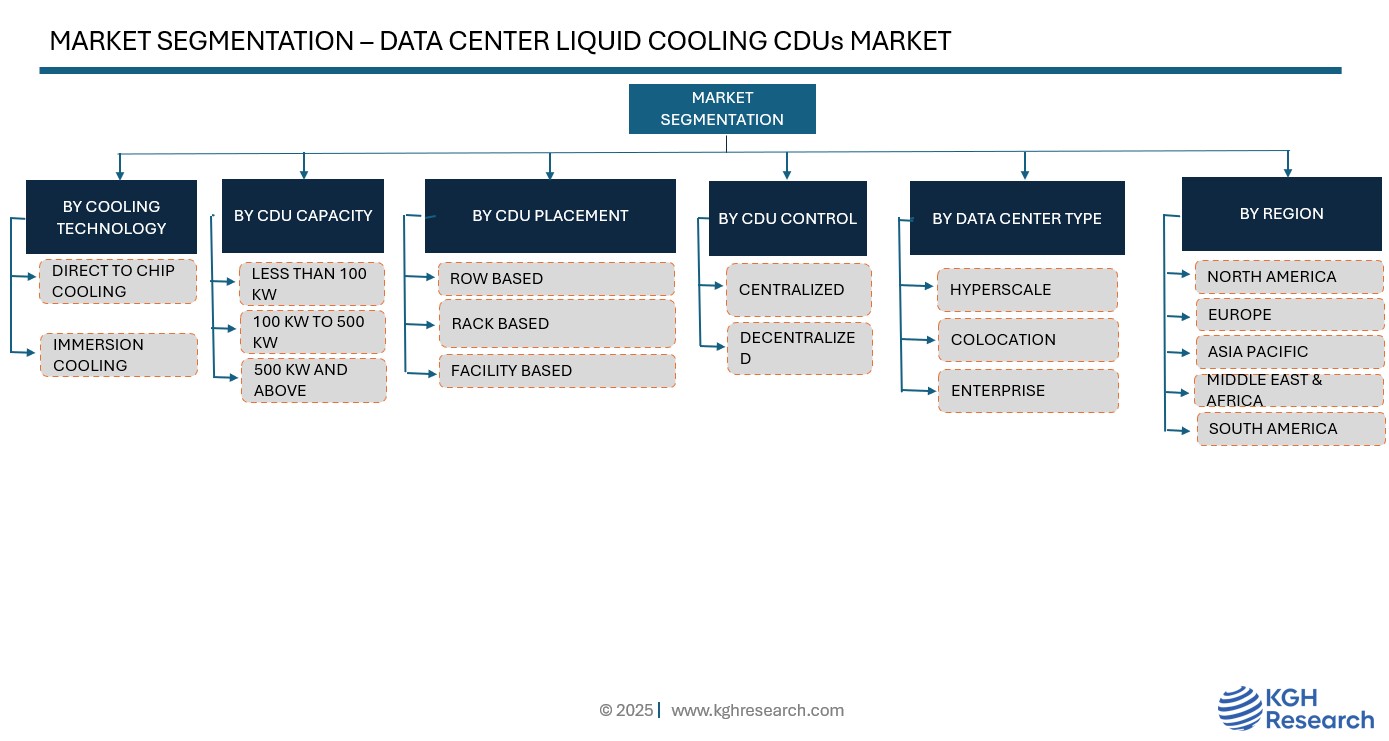

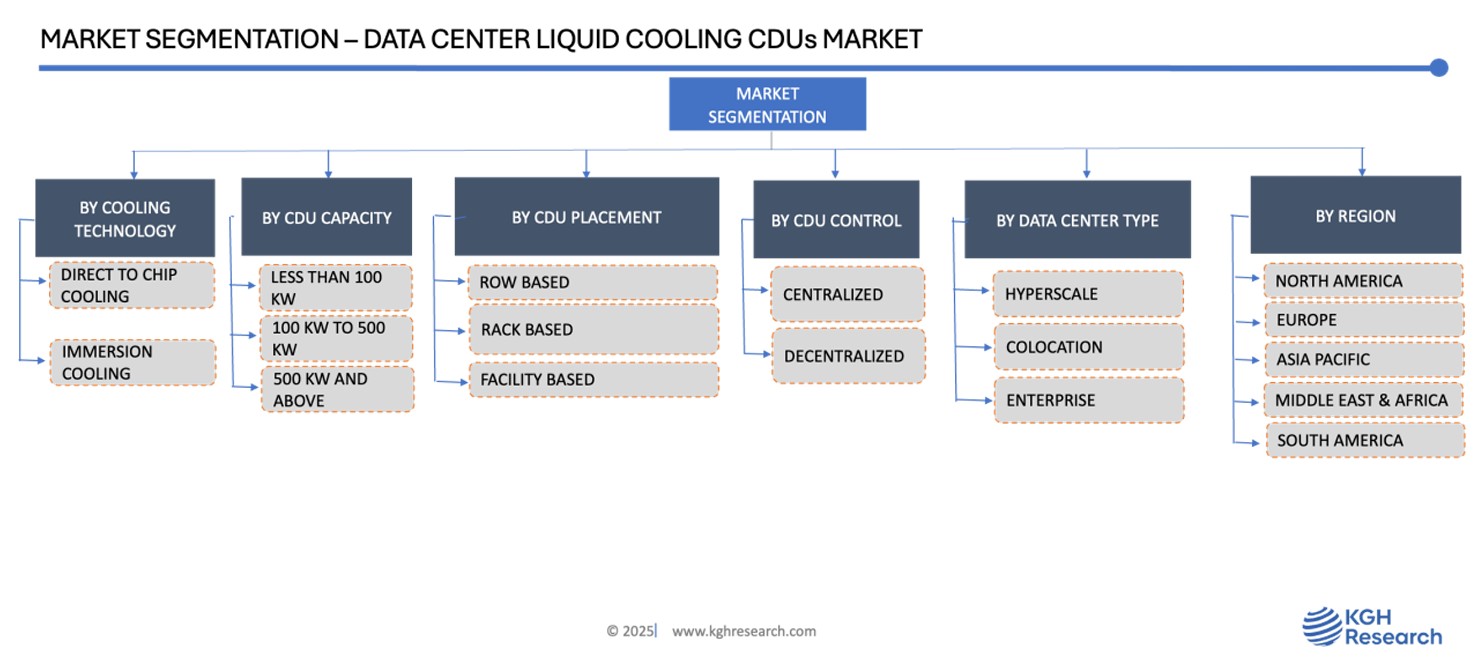

By Liquid Cooling Technology: Market Insights

Coolant Distribution Units (CDUs) are a critical component of liquid cooling systems, especially in high-density data centre environments where thermal loads are rising rapidly. By improving heat management, CDUs help boost overall system efficiency while lowering long-term operational costs, making them a smart investment for data centres looking to scale sustainably. At the heart of their function, CDUs circulate coolant through a closed-loop system that runs between the server chassis and the rack. In full liquid-cooled setups, they interface with facility water systems, coolant to offload heat, while also leveraging ambient air outside the rack for additional thermal exchange ensuring consistent cooling performance without excess energy use.

CDUs that are an integral part of a Direct to Chip Cooling system accounted for more than 90% share of the global data centre liquid cooling CDUs market, followed by CDUs that are used with immersion cooling technology. DTC cooling based CDUs likely to remain the dominant CDU type during the forecast period. DTC / Cold Plate Liquid Cooling technology to remain mainstream technology offering years of application track record, ease of deployment, and lower maintenance, on the other hand the current adoption rate of immersion cooling technology is less than 10% in the global data centre liquid cooling market, thus the prime drive immersion cooling CDU demand.

By CDU Capacity: Market Insights

Low-capacity CDUs that are typically less than 100 kw are typically deployed for rack based cooling or small cluster of IT equipment making them ideal for targeted cooling applications and retrofitting existing infrastructure in compute heavy infrastructure. Mid and high-capacity CDUs are increasingly crucial in supporting the rapid growth of high-performance computing (HPC), AI workloads, and GPU-intensive tasks within large-scale colocation and hyperscale facilities.

Mid capacity CDUs are typically in between 100 kw to 500 kw units serve multi-rack configurations and are often integrated with rear door heat exchangers or in-row cooling systems and holds the largest share of the market.

High-capacity CDUs are engineered to support facility-wide cooling distribution, capable of handling hundreds of kilowatts while interfacing with external facility water systems and is gaining traction in the market, the likes of CDUs introduced by DCX cooling. These units feature redundant pumping systems, advanced controls, and heat exchangers designed for optimal efficiency and uptime. As power densities in racks exceed 30–50 kW, and as adoption of direct-to-chip and immersion cooling technologies expands, demand for scalable, high-capacity CDUs is expected to surge, particularly in North America, Europe, and emerging Asia-Pacific markets.

By CDU Placement: Market Insights

Rack-based CDUs are compact units designed to cool individual server racks, often used in direct-to-chip or cold plate applications. They are closely coupled with the IT load and are ideal for edge data centres, AI inference clusters, or high-density enterprise deployments where localized heat removal is critical. These CDUs are valued for their modularity, precision cooling, and ease of retrofitting without reengineering entire cooling infrastructures. Demand is steadily growing as rack power densities increases (exceeding 60kw & beyond) and high-performance workloads driving demand of rack based CDUs

Row-based CDUs serve multiple racks within a single row and are typically integrated with in-row cooling units or rear-door heat exchangers. They strike a balance between performance and scalability, making them popular in colocation and mid-size data centres. These systems offer a favourable CAPEX-to-cooling capacity ratio and are often implemented during infrastructure upgrades or new builds where traditional CRACs are insufficient. Row-based CDUs are a popular choice for facilities operating in the 10–40 kW per rack range, offering redundant pumping, localized heat exchanger, and real-time thermal monitoring features.

Facility-level CDUs are the largest and most powerful units, deployed to manage coolant distribution across an entire data centre or zone. These systems interface directly with external facility water loops or chillers and are engineered for hyperscale and HPC environments where workloads like AI model training, scientific simulations, and crypto mining demand ultra-high rack densities. Facility-based CDUs can support multiple cooling technologies, including immersion cooling, direct-to-chip, and hybrid systems, and are built with robust controls for failover, leak detection, and thermal optimization and are very cost effective in data centre with large scale IT equipment deployment with higher IT load. Their adoption is accelerating due to the rise of liquid cooling as a default architecture in new hyperscale builds, especially in North America, Europe, and China.

By Data Center Type: Market Insights

The liquid cooling technology has become an integral part of hyperscale builds, mainly around the HPCs and AI based workloads especially in North America, Europe, and China, this segment is expected to experience double-digit growth in CDU deployments, followed by colocation and enterprise data centres. Cryptocurrency mining accounted for 5% to 10% of the global liquid cooling CDUs deployment.

Regional: Market Insights

North America leads global adoption of liquid cooling technology in the data centre market with more than 45% share, driven mainly by rapid growth of hyperscale and AI-focused data centres in the United States and Canada. The region is home to major cloud / hyperscale providers (AWS, Microsoft, Google, Meta), who are deploying facility-level liquid cooling infrastructure to accommodate power densities exceeding 40–60 kW per rack, particularly for AI/ML workloads. CDUs especially high-capacity facility-based units and row-based systems are integral to direct-to-chip and rear-door heat exchanger deployments across hyperscale campuses. Additionally, regional sustainability mandates and rising energy costs are encouraging the replacement of traditional air cooling systems with liquid cooling loops anchored by CDUs.

Asia Pacific is the fastest-growing region for CDU deployments, fuelled by explosive demand for digital infrastructure across China, India, Singapore, Japan, and South Korea. Hyperscale expansions, driven by cloud adoption and AI services, are pushing operators toward high-efficiency liquid cooling systems, particularly in urban areas with land constraints and high ambient temperatures. China and Singapore, in particular, are investing heavily in facility-wide CDUs integrated with immersion and direct-to-chip cooling technologies to optimize power and water use. Additionally, the region’s growing AI, fintech, and gaming ecosystems are increasing thermal loads, making row- and rack-based CDUs a preferred solution in modular and prefabricated data centre builds. Though still in early stages, the CDU market in the Middle East & Africa is gaining traction in mega-scale data centre projects being developed in the UAE, Saudi Arabia, Israel, and South Africa. The region’s hot climate and limited water resources make closed-loop liquid cooling systems with CDUs an attractive alternative to energy-intensive air conditioning. CDUs are particularly relevant in government-backed smart city and AI infrastructure projects, such as NEOM in Saudi Arabia, where high-density compute clusters require scalable, energy-efficient cooling. Adoption is expected to accelerate as cloud providers and telcos invest in local hyperscale capacity and edge compute nodes.

Competitive Landscape

The global CDU (Coolant Distribution Unit) market is characterized by a mix of established thermal management giants, specialized liquid cooling system suppliers, and emerging & startups addressing the evolving needs of high density data centres for an efficient and cost effective cooling technology and thus CDUs. Vertiv, Schneider Electric,, CoolIT Systems, Submer, Rittal, Nidec Corporation (pure CDU supplier), nVent, Motivair, DCX Cooling are some of the prominent names in the global data center liquid cooling market and are also integrated to CDU supply. Top 10 players accounted for more than 70% share of the market of the global data center liquid cooling CDUs market.

Recent Developments by Major Data Centre Liquid Cooling CDUs Market

- Vertiv: Vertiv is a dominant player offering a wide range of CDUs as part of its broader liquid cooling ecosystem. The company’s Liebert® XDU and XDU800 series are engineered for direct-to-chip and rear-door heat exchanger applications, with flexible configurations from 50 kW to over 400 kW. Vertiv’s strength lies in its global service infrastructure, integration with existing facility water loops, and partnerships with hyperscalers and OEMs.

- Schneider Electric: Through its EcoStruxure™ Liquid Cooling Solutions, Schneider provides CDUs that integrate with direct liquid cooling and rear-door heat exchangers, optimized for energy savings and operational transparency. Schneider is particularly focused on modular and prefabricated deployments, targeting colocation providers and edge facilities, and is strengthening its CDU portfolio through alliances with liquid cooling startups.

- DCX Cooling: DCX Cooling has recently launched its groundbreaking Facility Distribution Units (FDUs), marking a significant evolution in data center liquid cooling architecture. Unlike traditional Coolant Distribution Units (CDUs), which are typically distributed near server racks, the new DCX FDU is a centralized, high-capacity solution deployed outside of white space, such as in technical corridors. This design enables it to efficiently cool entire data halls or AI clusters, supporting up to 60 high-density racks and delivering up to 5MW of heat transfer capacity—ideal for the demands of next-generation AI and hyperscale data centers

- Motivair Corporation: Specializing in high-performance cooling, Motivair is known for its ChilledDoor® system and high-capacity CDUs (up to 1 MW), which are widely deployed in AI/ML, HPC, and government computing environments. The company emphasizes custom-engineered CDU systems with advanced telemetry, redundant pumping, and integration with water-cooled GPUs—making it a preferred supplier for AI datacenters and national labs.

- CoolIT Systems: CoolIT is a key innovator in direct-to-chip liquid cooling, providing rack-based and row-based CDUs as part of its Rack DCLC™ platform. The company’s compact, high-efficiency CDUs are deployed in hyperscale, enterprise, and OEM-integrated systems, with advanced control software and telemetry support. CoolIT’s partnerships with server manufacturers and recent expansions in Asia and North America are enhancing its market footprint.

- Nidec Corporation: Nidec Corporation is a prominent name in the global data centre liquid cooling CDU market, supplying its CDUs mainly to SuperMicro. Nidec Corporation has increased its production capacity of 100 kw to 250 kw CDUs jointly developed in collaboration with SuperMicro from 200 per month to 2000 unit per month in 2024 at the Ayutthaya Plant in Thailand,

- Rittal GmbH & Co. KG: Rittal offers CDU systems as part of its LCP (Liquid Cooling Package) portfolio, often integrated into enclosure cooling for data centers and edge environments. Known for German-engineered precision and modularity, Rittal is gaining traction in Europe and the Middle East, especially among colocation and enterprise clients pursuing energy-efficient cooling retrofits.

- Submer Technologies: A pioneer in immersion cooling, Submer provides integrated CDU solutions for its SmartPodX™ and SmartPodXL™ immersion systems. As immersion cooling scales in crypto mining, AI, and telco edge, Submer’s ability to pair CDUs with dielectric coolant systems positions it well in this emerging niche.

DATA CENTER LIQUID COOLING COOLANT DISTRIBUTION UNIT MARKET SNAPSHOT | |

Market size in 2025 | USD 1.2 Billion |

Market forecast in 2032 | USD 15 Billion |

Compound Annual Growth Rate (2025-2035) | >25% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2035 |

Region Dominance (Regional Share %) | North America: >45% Share |

Country Dominance (Share %) | US: >40% Share |

Growth Drivers & Emerging Trends | Growing data centre market, increasing deployment of compute heavy HPC / AI based works, and Innovations & technological advancements in AI powered compute heavy GPUs, the likes of NVIDIA GB200, RUBIN, AND RUBIN ULTRA with higher TDP (Thermal Design Power) ratings necessitating the deployment of liquid cooling technology and thus driving demand for CDUs |

Segments Covered | By Cooling Technologies, by CDU Capacity, by CDU Placement, by CDU Location, by Data Center Type, by and by Regions & Countries |

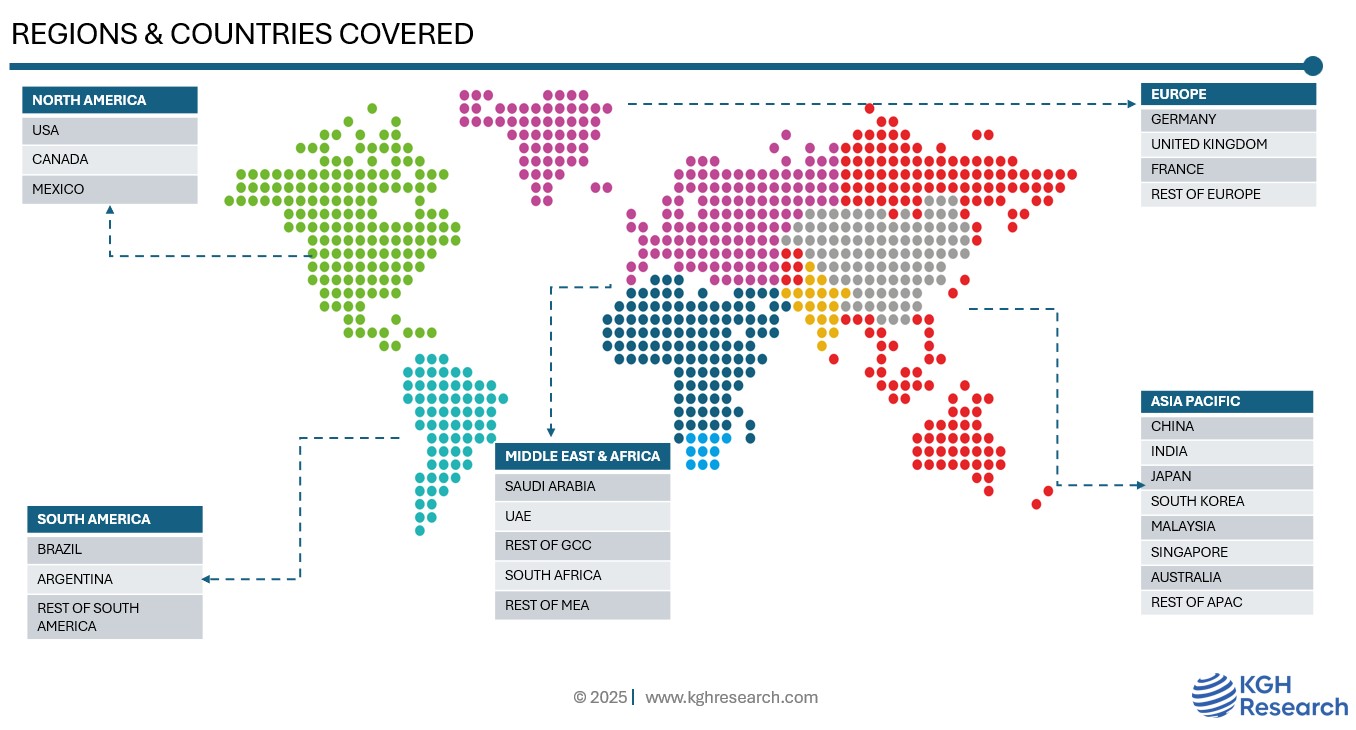

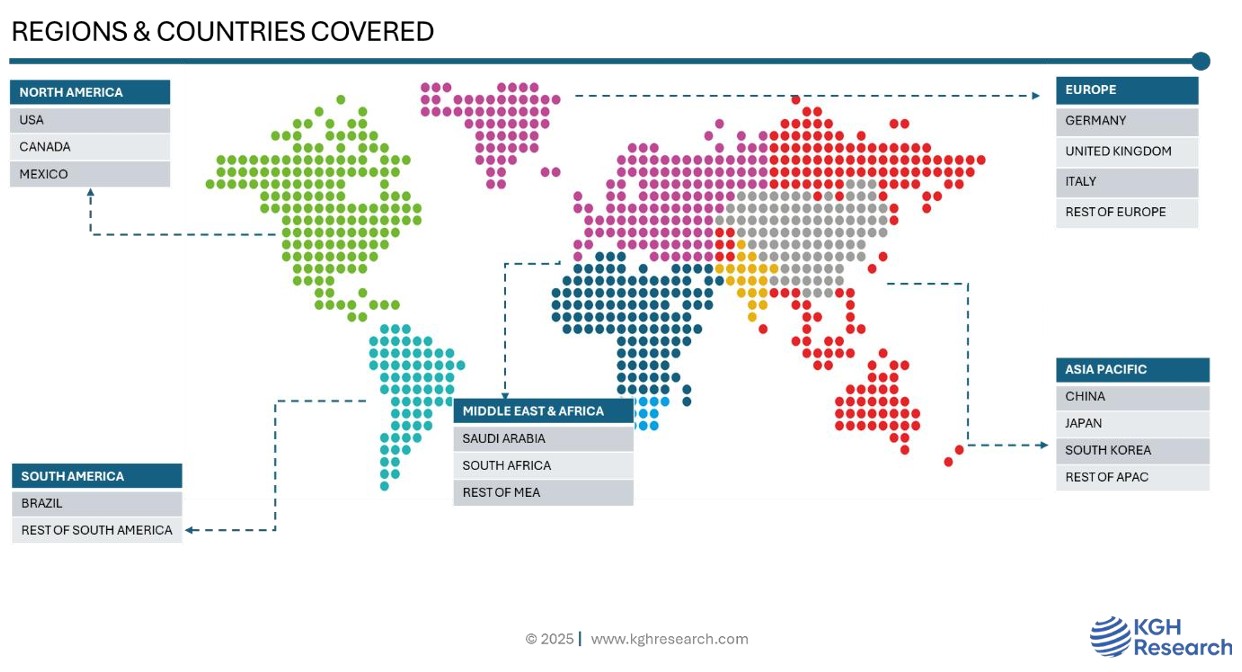

Regions Covered | North America, Europe, Asia Pacific, Middle East & Africa, and South America |

Countries Covered | US, Canada, Mexico, The UK, Germany, France, Rest of the Europe, China, India, Japan, South Korea, Malaysia, Singapore, Australia, and Rest of APAC, Saudi Arabia, GCC Countries, South Africa and Rest of MEA, Brazil, and Rest of South America |

Companies Profiled (20+) | Vertiv, Schneider Electric, CoolIT Systems, Accelcius, Nidec Corporation, Kaytus, Stulz, DCX Cooling, Asetek, CoolCentric, nVent, Motivair, BOYD, RITTAL, Submer, Midas, Kaori, Envicool, Canatec, Zutacore, Liquid Stack, Airdate by Modine, Nortek, Chilldyne, and Many More |