Aerospace Composites Market (2022 - 2032)

AEROSPACE COMPOSITES MARKET SIZE & SHARE BY FIBER TYPE (CARBON FIBER, GLASS FIBER, CERAMIC FIBER, AND OTHERS), BY MATRIX (EPOXY, PHENOLIC, POLYIMIDE, PEEK, PEI, CERAMIC, METAL, AND OTHERS), BY AIRCRAFT TYPE (COMMERCIAL, REGIONAL, BUSINESS, MILITARY, SPACE, AND UAMs / UAVs), BY APPLICATIONS (FUSELAGE, WINGS & CONTROL SURFACES, ENGINES, ROTORBLADES, TAILBOOMS, SEATS, CABIN, FLOOR & BODY PANELS, AND OTHERS), BY MANUFACTURING TECHNOLOGIES (ATL/AFP, LAYUP, RTM, FILAMENT WINDING, AND OTHERS), AND BY REGION & COUNTRY–FORECAST TO 2032

| Report Code: A&D1001-0101 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: JULY 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

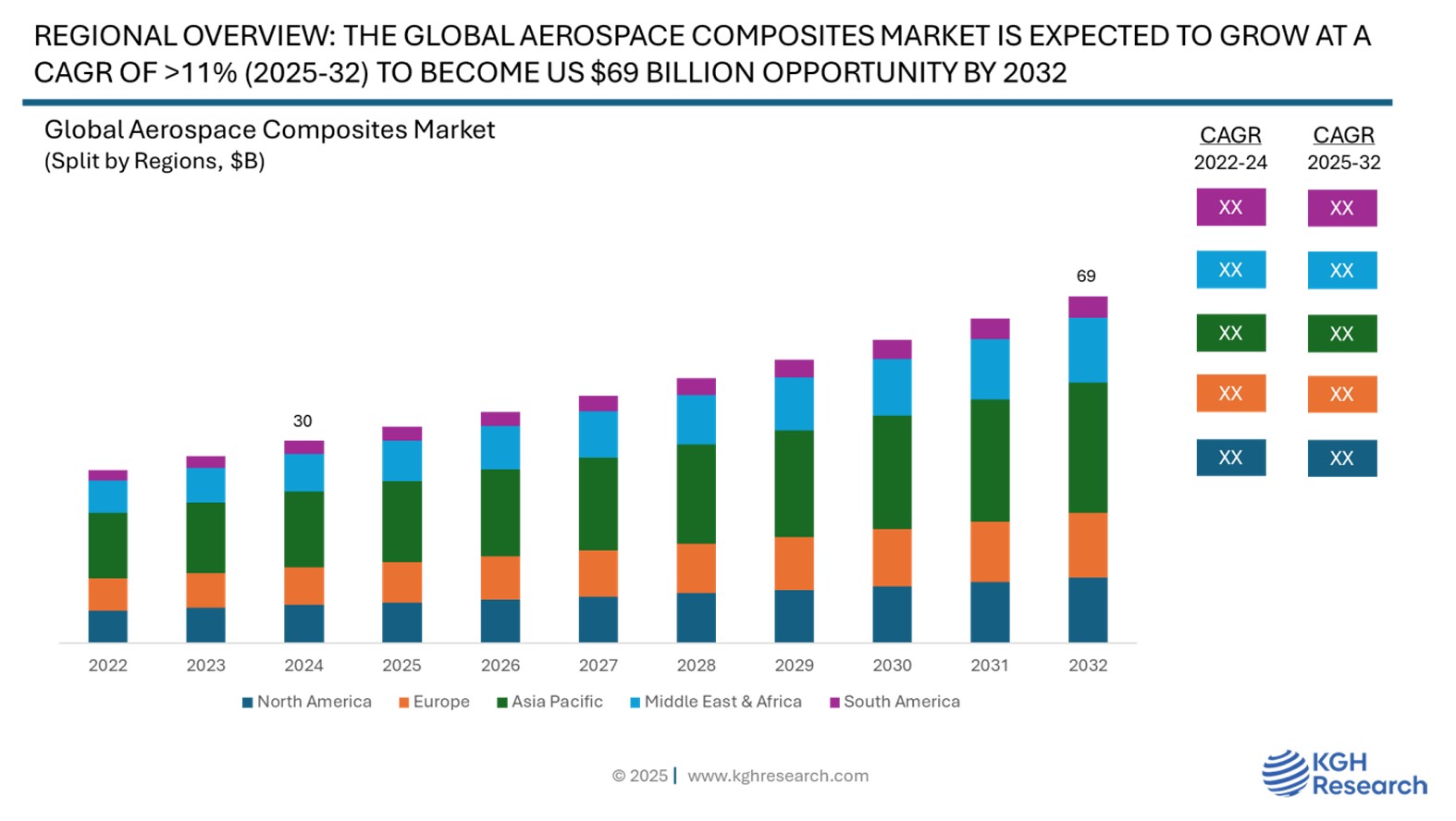

Market Overview: The global aerospace composites market was estimated at US $30 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of more than 11% from 2025 to 2032 to reach US $69 billion by 2032. The aerospace composites market is undergoing a transformative shift, fuelled by the growing need for lightweight structures, sustainability goals, and high-performance materials requirement in the next-generation aircraft. Composites have become indispensable across the aerospace industry value chain offering unmatched strength-to-weight ratios, fuel efficiency benefits, and corrosion resistance compared to traditional materials like aluminium and steel. As the industry pivots toward sustainable aviation, the role of composites is only deepening, especially in fuselage structures, wings, interior panels, rotor blades, engine cowlings, fan blades, and nacelles as the lighter structures are tend to consume less fuel and emit less greenhouse gases.

Increasing air passenger traffic, globally driving new commercial aircraft demand and deliveries, replacement of ageing fleets with next generation composites intensive aircraft, geopolitical tensions driving defence budget & expenditure globally, creating demand for military jets, defence drones, helicopters, and transporters, and increasing emphasis on the development of urban air mobility infrastructure, creating demand for composites intensive eVTOLs and UAVs are the major drivers for increasing consumption of composites in the aerospace industry.

MARKET DYNAMIC

GROWTH DRIVERS:

- Increasing commercial aircraft deliveries

- Replacement of ageing fleet with next generation composites intensive aircraft

- Sustainable aviation trends

- Lightweighting trend

- Driver 5

- Driver 6

NEW GROWTH OPPORTUNITIES:

- Innovations and technological advancements defining a new era of air mobility with eVTOLs, UAVs, and commercial drones driving demand for composites

- Green aviation technologies – Electric Powered Aircraft and Hydrogen Powered Aircraft

- Deployment of advanced technology and growing usage of AI to ensure high quality production process with zero tolerance to wastages and growing emphasis on passenger safety.

- Opportunity 4

MARKET RESTRAINTS:

- Growing concerns towards increasing aircraft travel related fatalities due to the usage faulty and defective parts impacting a global OEM.

- Lack of accountability and traceability of substandard parts due to widespread multi-contracting partnerships for part supply.

GROWTH HURDLES:

- Trade tensions, tariffs, and geopolitical instability likely to impact global supply chains, demand, production costs, and profitability of airliners, aircraft and part manufacturers, and associated partners in the supply chain.

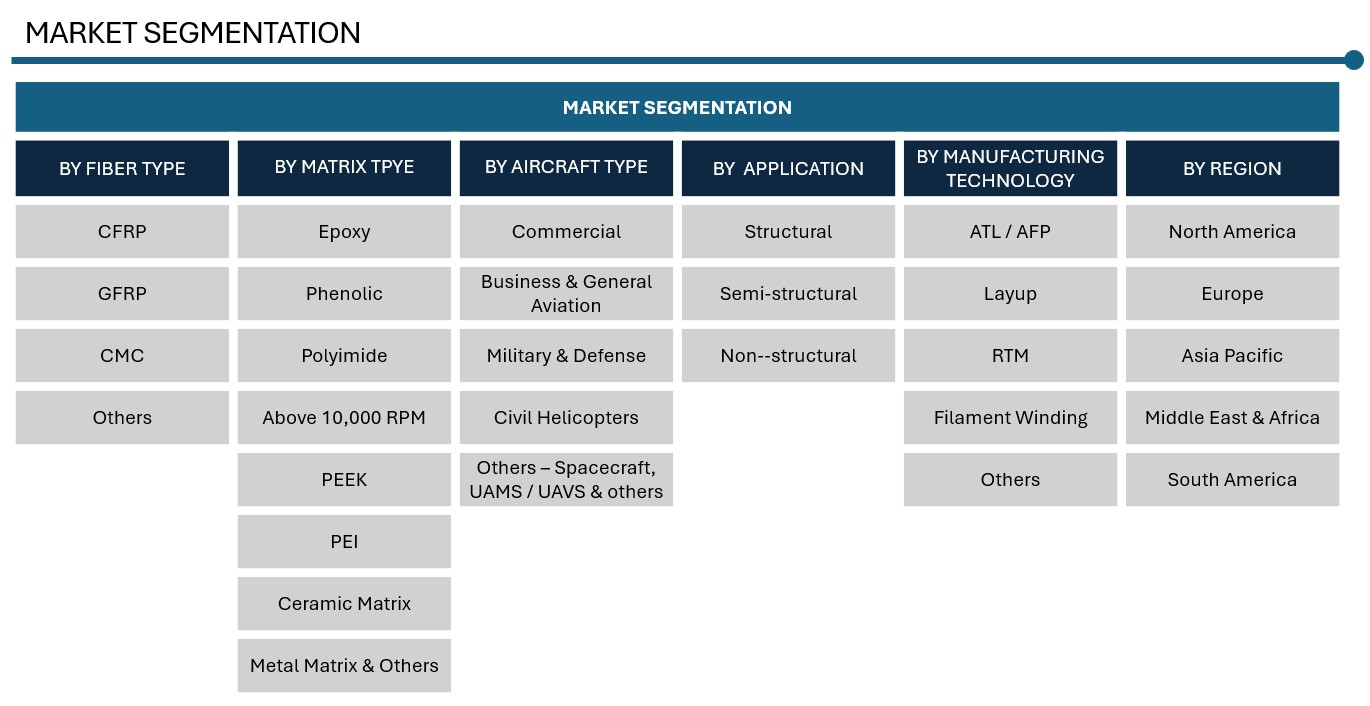

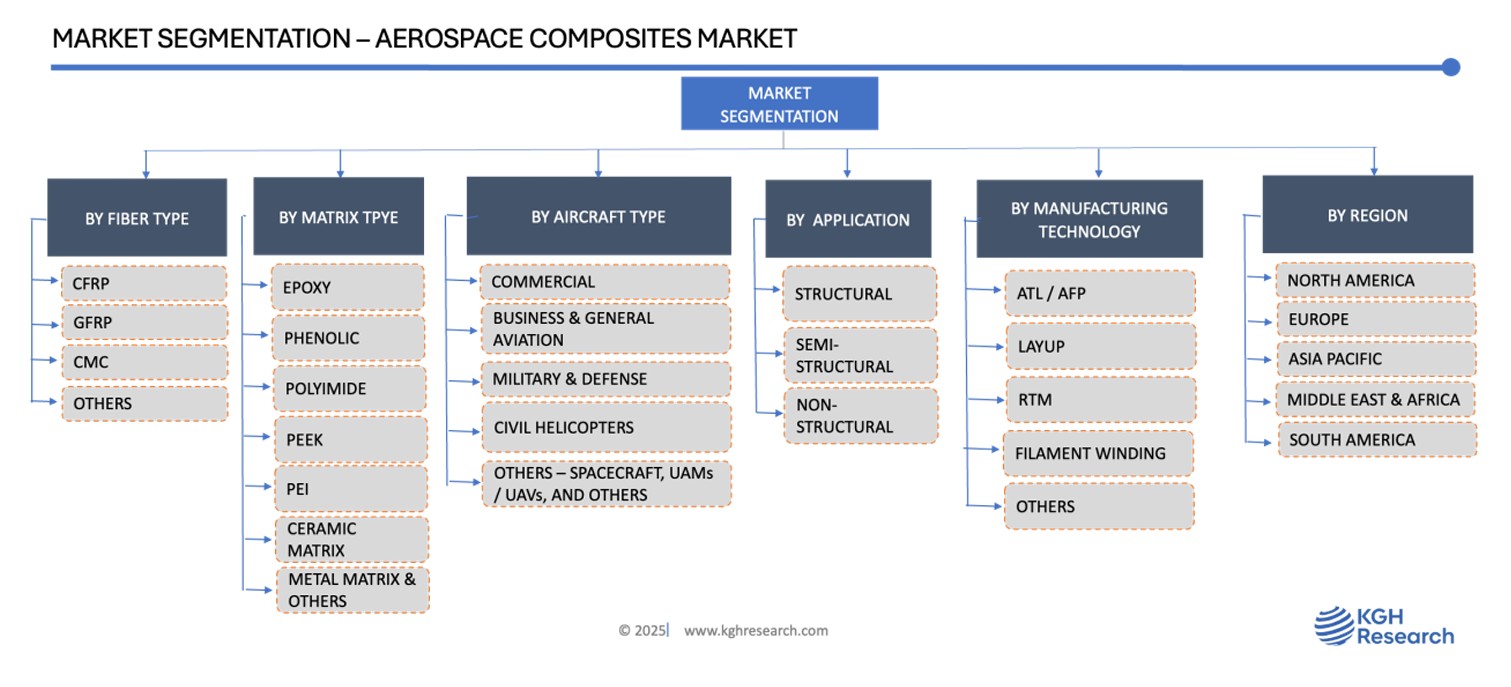

By Fiber Type: Market Insights

The aerospace composites market is segmented by fibre type into carbon fiber, glass fiber, ceramic fiber, and others. Among these, carbon fibre continues to lead the segment, having captured the largest market share in 2024 and is projected to maintain its dominance throughout the forecast period. This leadership is driven by its growing adoption in aerospace and defence applications, where strength-to-weight performance is critical. Known for its exceptional tensile strength, modulus, lightness, and resistance to environmental degradation, carbon fiber also provides surface customization, making it ideal for a wide range of structural and semi-structural aerospace components.

By Matrix Type: Market Insights

The aerospace composites market, when segmented by matrix type, includes polymer matrix, metal matrix, and ceramic matrix. Among these, polymer matrix composites are expected to dominate the market in both value and volume over the forecast period. This leadership is fuelled by their increasing adoption in modern aircraft designs, driven by the aerospace industry’s relentless pursuit of fuel efficiency, durability, and environmental performance.

Polymer matrix composites offer an optimal blend of lightweight properties, structural strength, and versatility, making them the material of choice for manufacturers aiming to meet evolving regulatory and operational standards. Ongoing investments in research and development are further enhancing their performance, affordability, and processing efficiency. These advancements are not only reinforcing their role in aerospace applications but also paving the way for their continued expansion across next-generation aircraft platforms.

By Composites Type: Market Insights

The aerospace composites market, when segmented by composites type, includes thermoset polymer composites, thermoplastic polymer composites, metal matrix composites, and ceramic matrix composites. Among these, thermoset plastics held the largest market share, while thermoplastic composites are anticipated to grow more rapidly during the forecast period owing to its exceptional properties, such as ease of processing, recyclability, and strength to weight ratio.

By Aircraft Type: Market Insights

In terms of aircraft classification, the market encompasses commercial aircraft, business and general aviation, civil helicopters, military aircraft, spacecrafts, and UAMs, and UAVs. Commercial aircraft segment held the dominant market share, largely due to the shift toward high composite intensive airframes in new aircraft models. For example, Airbus’s A350 extensively incorporates composite materials far more than legacy aircraft designs that typically used only 2% to 6% composites. The demand for lighter, corrosion-resistant, and low-maintenance materials is accelerating adoption, particularly in commercial fleets striving for better fuel efficiency and reduced lifecycle costs.

By Application: Market Insights

The aerospace composites market is broadly segmented by application into structural components and semi & non-structural components. The structural components mainly includes fuselage, wings, control surfaces, rotor blades, tail boom, bulkhead, and others, while semi & non-structural components includes interior applications, such as seats, cabin, overhead bins, floor & body panels, engine cowlings, fan blades, and others. Among these, structural applications accounted for the largest share, owing to the high performance requirements and weight sensitivity of these components. Advanced composites such as carbon fiber reinforced polymers (CFRPs) have become integral to modern aircraft designs due to their superior strength-to-weight ratio, fatigue resistance, and corrosion resistance properties.

Interior applications are also witnessing increased composites usage, particularly in seats, cabin panels, and overhead bins, driven by the need for enhanced fuel efficiency through weight reduction without compromising on structural integrity of the component, passenger safety and comfort. Meanwhile, composite use in engine nacelles, blades, and brackets is rising, propelled by innovations in high-temperature-resistant matrix systems. As the aerospace industry pivots toward sustainable and next-generation aircraft, the role of composites across all application areas is expanding enabling improved fuel economy, extended service life, and reduced environmental impact.

Manufacturing Technology: Market Insights

In the aerospace composites market, manufacturing technologies play a pivotal role in shaping material performance, production efficiency, and overall cost competitiveness. Key technologies include Automated Fiber Placement (AFP), Automated Tape Layup (ATL), Lay-up, Resin Transfer Moulding (RTM), Filament Winding, and others. Among these, automated processes, such as AFP / ATL and RTM are gaining significant traction, as they enable precise control over fibre orientation and resin distribution while supporting high-throughput production, critical for modern aerospace programs that demand consistency, speed, and scalability.

The rising complexity of aircraft components and the industry’s push for lightweight, high-strength structures have accelerated the adoption of advanced, automated manufacturing techniques. These innovations not only reduce material wastage and labour dependency but also improve structural integrity and productivity. As aerospace OEMs and tier suppliers continue to invest on digitalization and smart manufacturing, these technologies are expected to remain at the forefront of composites part production, shaping the future of cost-effective and sustainable aircraft manufacturing.

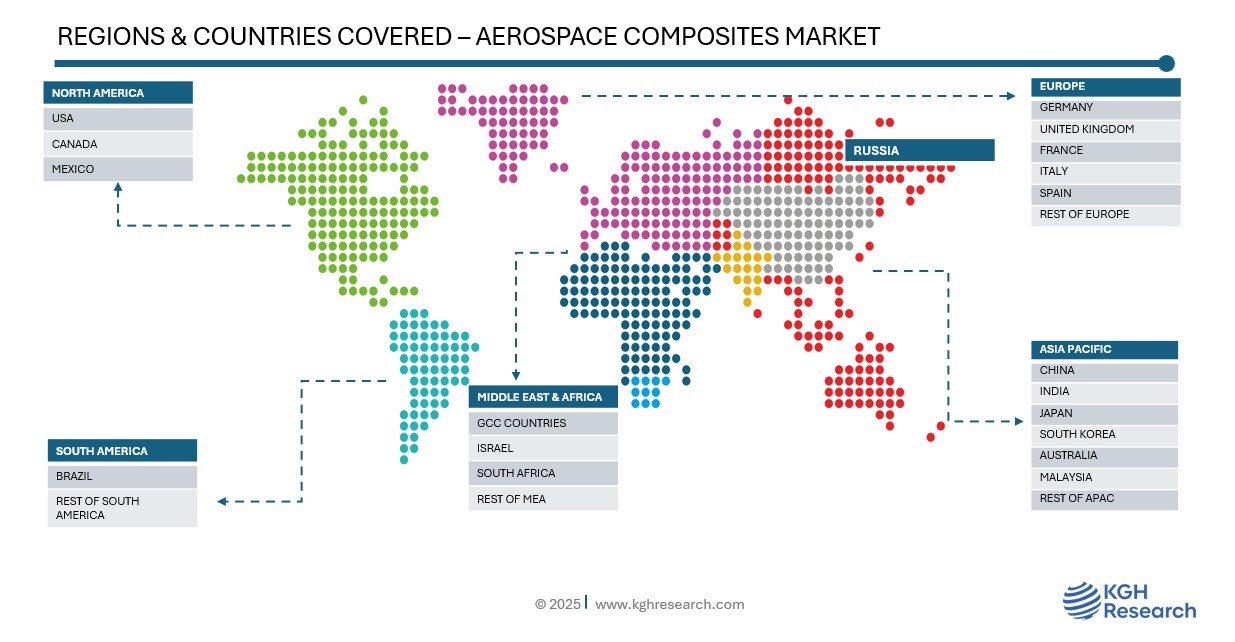

Regional: Market Insights

The global aerospace composites market exhibits strong regional dynamics driven mainly by increasing production and deliveries of commercial and military aircraft. Based on Airbus Analysis, 42,430 new commercial aircraft deliveries are expected between 2024 and 2043 in which 33,510 (nearly 80%) of the aircraft deliveries would be for single aisle and 8920 (20%) deliveries would be for composites intensive widebody aircrafts (Source: Airbus). A vast majority of these demand are expected to be generated by Asia Pacific region i.e., nearly 46% (19,510 deliveries), mainly due to increasing air passenger traffic, growing per capita income, and other economic factors, followed by Europe & CIS countries, and North America. Middle East & Africa is expected to generate a total demand of more than 5000 aircraft during this period.

In the composites market, North America leading the charge, driven by its well-established aerospace manufacturing base, significant defence expenditure, and the presence of major players, such as Boeing, Lockheed Martin, and Northrop Grumman. The U.S. continues to dominate the regional demand for composite materials owing to rapid advancements in commercial and military aircraft programs and robust investments in R&D for lightweight and high-performance materials.

Europe follows closely, fuelled by the aerospace innovation ecosystem in countries, such as Germany, France, and the UK. Airbus, a major contributor to the region’s composites demand, is actively integrating advanced composites in its aircraft platforms like the A320neo and A350XWB. Regional initiatives like Clean Sky 2 and the EU’s aggressive carbon reduction goals are further boosting the development of recyclable and sustainable composite materials.

In Asia-Pacific, countries such as China, Japan, and India are emerging as key growth engines. China’s expanding domestic aviation market and rising defence budget are creating strong demand for aerospace-grade composites. Japan continues to contribute with its technical prowess in carbon fibre production, while India is investing in indigenous aircraft and defence programs, catalysing future demand. Meanwhile, the Middle East and Latin America, though smaller in current market share, are poised for future growth due to increasing airline fleet expansions and emerging MRO (maintenance, repair, and overhaul) hubs.

Competitive Landscape

The competitive landscape of the aerospace composites market is characterized by a strong presence of established global players who command significant technological prowess, vertical integration, and long-term supply agreements with leading aerospace OEMs & part fabricators, such as Boeing, Airbus, Lockheed Martin, Spirit, Northrop Grumman, Embraer and many more. Companies like Hexcel Corporation, Toray Industries, Solvay, Teijin Limited, and Mitsubishi Chemical Group have emerged as dominant forces by offering a wide portfolio of advanced composite materials, including carbon fiber-reinforced polymers (CFRPs), aramid fibers, and high-performance thermoset and thermoplastic resins. These players continuously invest in R&D to develop lighter, stronger, and more sustainable composite solutions that meet the evolving demands of both commercial and military aircraft platforms. Strategic collaborations, M&A activity, and localization of manufacturing to support rising global aircraft production are key trends shaping the competitive strategies of these firms.

In addition to scale and global reach, innovation is a core competitive differentiator. For instance, leading companies are focusing on next-gen materials for applications in Urban Air Mobility (UAM), electric aircraft, and hypersonic defence systems. The integration of automation and digital technologies into composite manufacturing, such as AFP (Automated Fiber Placement), resin infusion techniques, and digital twins is allowing companies to scale production efficiently while maintaining stringent aerospace quality standards. Furthermore, the shift toward sustainability is prompting major suppliers to explore recyclable thermoplastics and bio-based resins, positioning themselves ahead of environmental regulations and airline sustainability mandates.

Recent Developments by Major Aerospace Composite Material Suppliers

- Hexcel Corporation

- In 2024, Hexcel inaugurated a new Center of Excellence for thermoplastic composites in Utah, focusing on next-gen aerospace applications including UAM and eVTOL platforms.

- Signed a long-term supply agreement with Dassault Aviation to provide carbon prepregs for the Falcon business jet series.

- Partnered with Spirit AeroSystems to develop lightweight wing and fuselage components using high-rate resin infusion technologies.

- Toray Industries

- In 2023, Toray introduced Torayca™ T1200, a new generation of ultra-high modulus carbon fiber designed for advanced structural parts in space and supersonic aircraft.

- Expanded its carbon fiber manufacturing capacity in France to support Airbus’s growing demand under the A320neo and A350 programs.

- Solvay

- Launched Veradel® HC, a sustainable thermoplastic resin for high-heat aerospace applications.

- In 2024, collaborated with Safran to co-develop recyclable composite materials for future engines and nacelle structures.

- Partnered with Vertical Aerospace to supply composite materials for their VX4 electric aircraft.

- Teijin Limited

- Acquired Renegade Materials Corporation to strengthen its aerospace thermoset prepreg capabilities.

- Introduced a carbon fiber with 30% reduced CO₂ footprint aimed at meeting new environmental criteria for aircraft manufacturers.

- Continued its supply of materials for Boeing and Lockheed Martin’s commercial and defense platforms.

- Mitsubishi Chemical Group

- Enhanced its thermoplastic composites portfolio by launching new prepregs compatible with automated manufacturing systems.

- Signed a MoU with Embraer to explore bio-based resins and circular economy practices in aircraft interiors and secondary structures.

- TenCate Advanced Composites (now part of Toray)

- Continued supply of advanced thermoplastic composites for UAVs and rotorcraft applications.

- Expanded presence in Europe by partnering with OEMs for lightweighting initiatives in regional aircraft programs.

These developments indicate a market in flux driven by the twin imperatives of innovation and sustainability with companies racing to redefine material technologies that will shape the next era of aerospace engineering.

AEROSPACE COMPOSITES MARKET SNAPSHOT | |

Market size in 2024 | USD 30 Billion |

Market forecast in 2032 | USD 69 Billion |

Compound Annual Growth Rate (2025-2032) | 11%+ |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Region Dominance (Regional Share %) | North America: >40% Share |

Country Dominance (Share %) | US: >35% Share |

Growth Drivers & Emerging Trends | Increasing New Aircraft Deliveries, Replacement of Ageing Commercial & Military Aircraft, Lightweighting Trend, Sustainability & Circularity Trends, Regulatory Pressure, Innovations, Development of composites intensive UAMs / UAVs, such as eVTOL. |

Segments Covered | By Fiber Type, Matrix Type, Composites Type, Aircraft Type, Applications, Manufacturing Technologies, and by Regions & Countries |

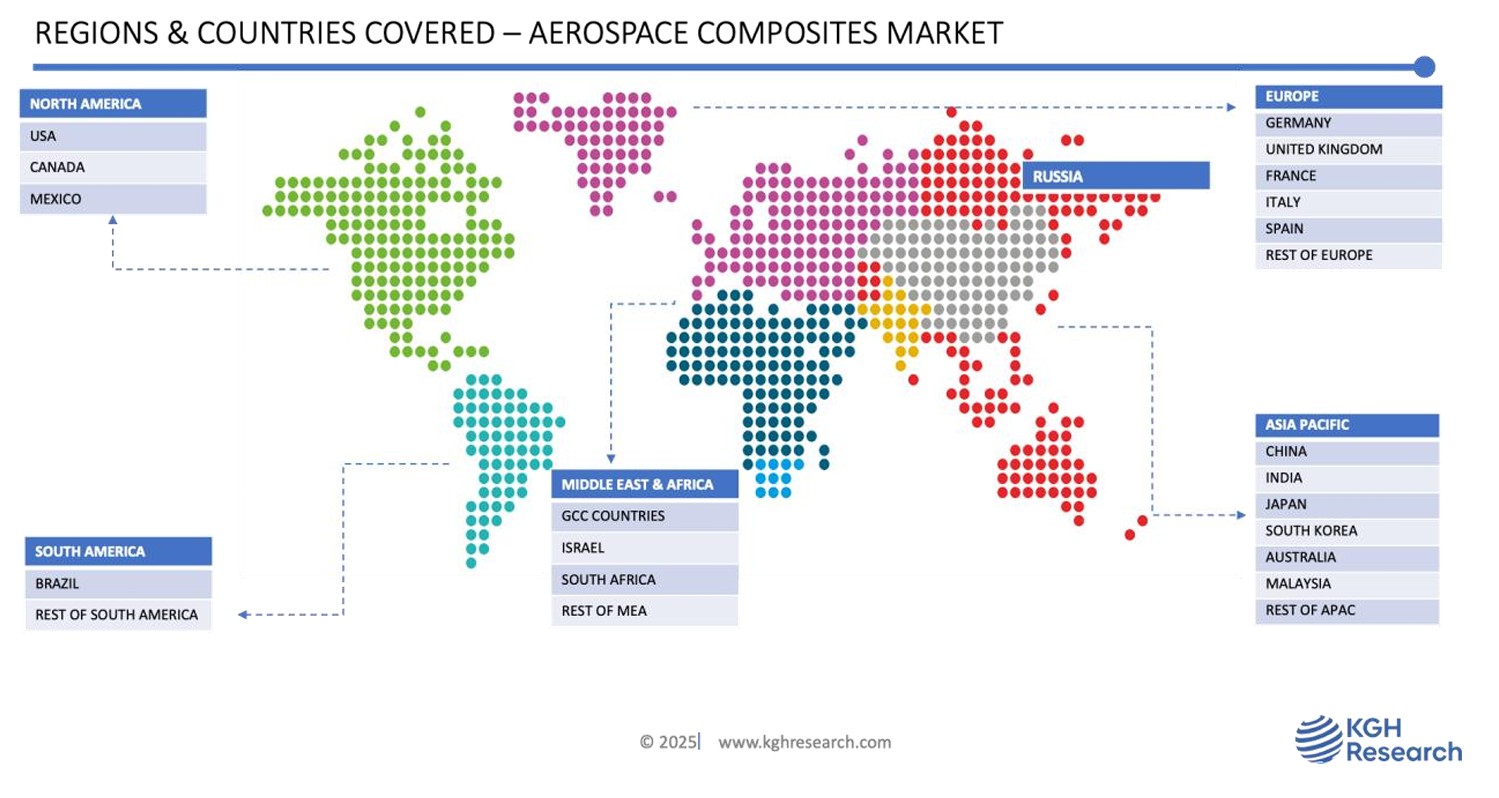

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, The UK, Germany, Italy, France, Spain, Russia, Rest of the Europe, China, India, Japan, South Korea, Malaysia, Australia, and Rest of APAC, GCC Countries, Israel, South Africa and Rest of MEA, Brazil, and Rest of South America |

Companies Profiled (20+) | HEXCEL, SOLVAY GROUP, TORAY INDUSTRIES, TEIJIN, MITSUBISHI, MATERION, RENEGADE, GURIT, OWENSCORNING, TENCATE (TORAY), SGL CARBON, AND MANY MORE |