Electric Motor (2022 - 2032)

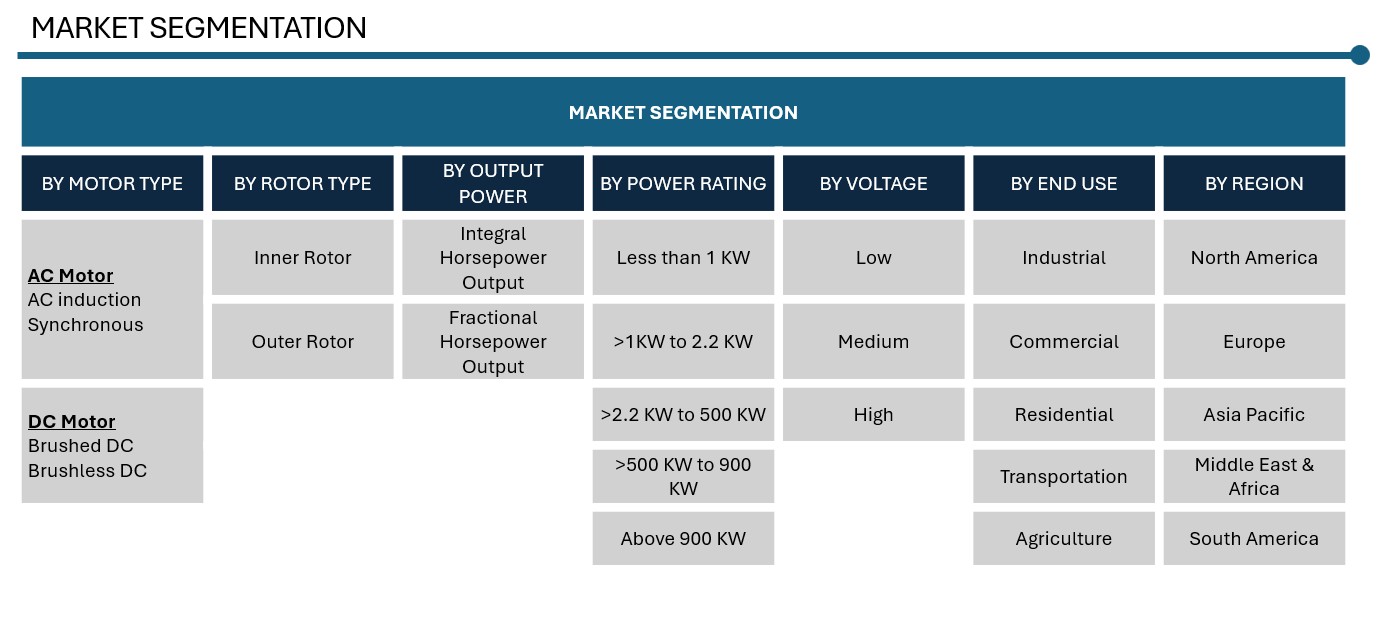

ELECTRIC MOTOR MARKET SIZE & SHARE BY MOTOR TYPE (AC, DC), ROTOR TYPE (INNER ROTOR, OUTER ROTOR), BY POWER RATING (LESS THAN 1 KW, >1KW TO 2.2 KW, >2.2 KW TO 500 KW, >500 KW TO 900 KW, ABOVE 900 KW) BY VOLTAGE (LOW, MEDIUM, HIGH), BY OUTPUT POWER (INTEGRAL HP, FRACTIONAL HP), BY END USE (INDUSTRIAL, COMMERCIAL, RESIDENTIAL, TRANSPORTATION, AGRICULTURE) AND BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: E&P4002-0701 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2019 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: JULY 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

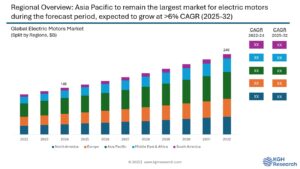

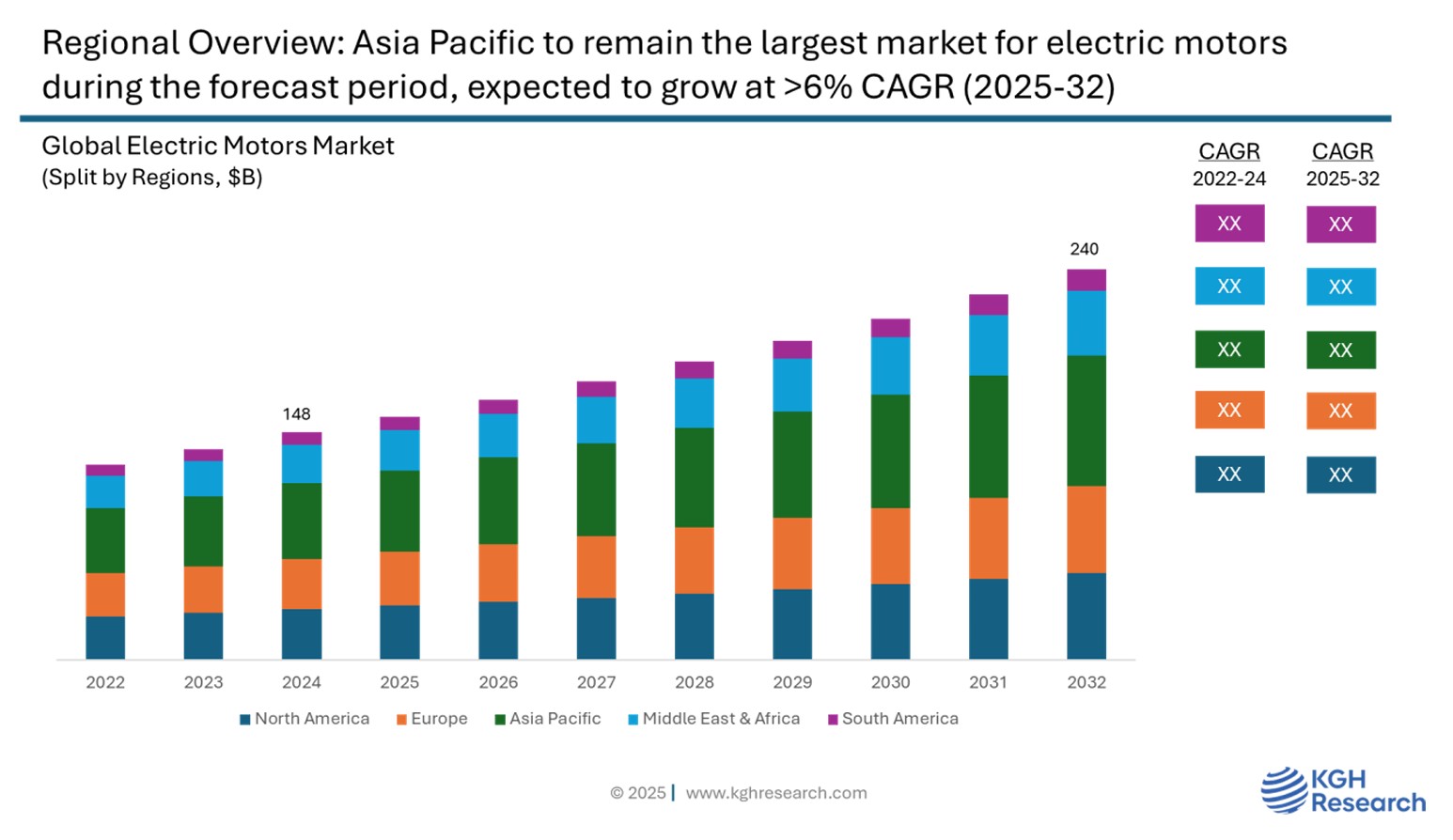

Market Overview: The global electric motors market was valued at approximately USD 148 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 6.2% from 2025 to 2032 to reach USD 240 billion by 2032. The global electric motors market is experiencing significant growth due to the rising need for energy-efficient solutions, the surge in electric vehicle (EV) adoption, and the acceleration of industrial automation. Rapid industrialization and broader use of these motors across industrial, commercial, residential, transportation, and agriculture sectors continue to support market expansion. Supportive government policies, including incentives and regulations promoting sustainable technologies, are further propelling market development.

MARKET DYNAMIC

GROWTH DRIVERS:

- Rising need for energy-efficient solutions

- Rising demand across manufacturing sectors

- Surge in electric vehicle (EV) adoption

- Acceleration of industrial automation

- Rising demand for HVAC across sectors

NEW GROWTH OPPORTUNITIES:

- Rapid industrialization and electrification in emerging economies, such as India, Brazil, and ASEAN nations offer untapped potential

- Growing demand for renewable energy systems

- Demand for smart and connected devices offers massive growth opportunities

MARKET RESTRAINTS:

- High initial cost

- Supply chain constraints

- Complex design & control requirements

GROWTH HURDLES:

- Trade tensions, tariffs, and geopolitical instability likely to strain global supply chain and impact electric motor manufacturing cost

- Intense competition as many players in the market are from the low-cost economies

- Recessions or downturns likely to impact industrial and consumer spending, likely to affect demand

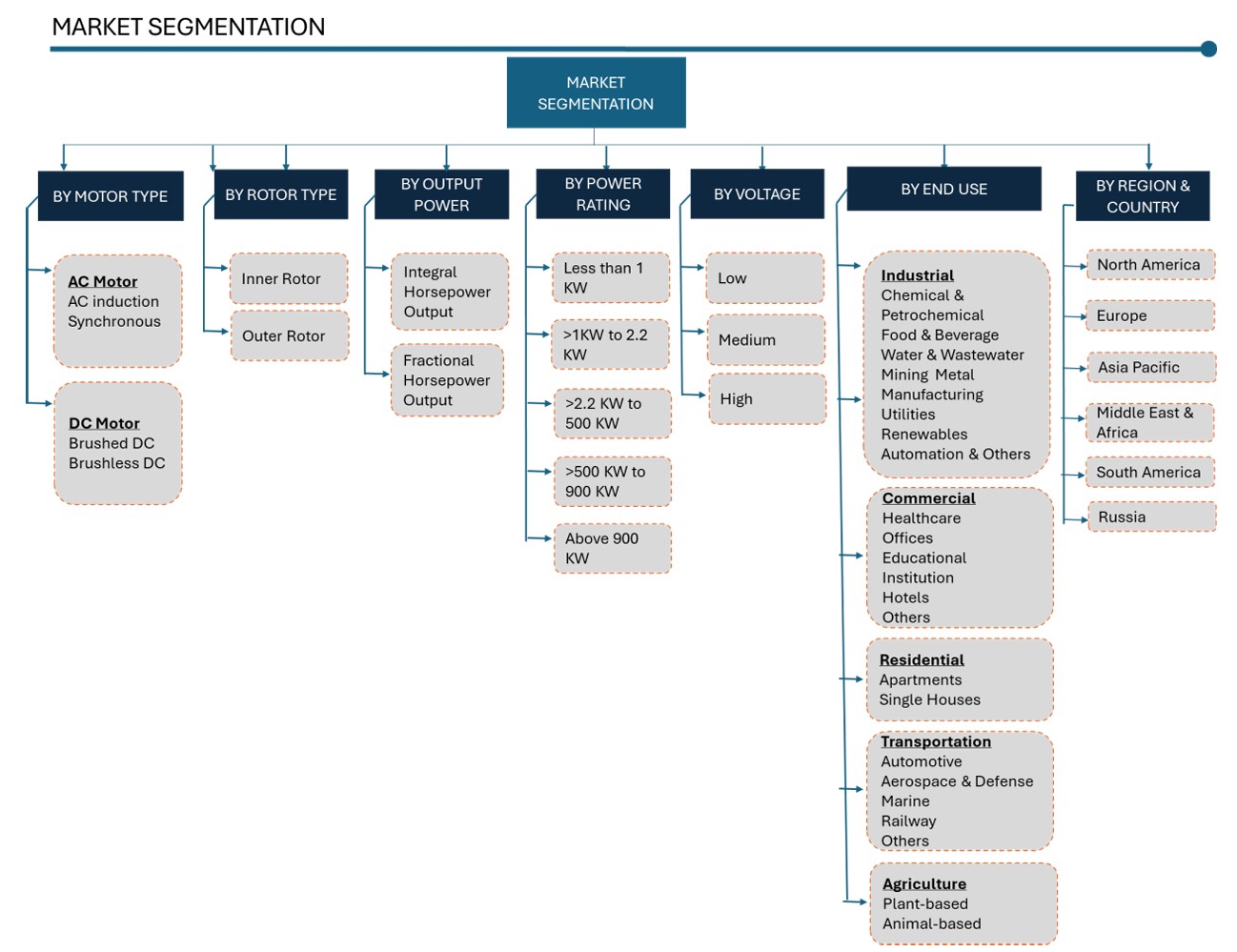

Motor Type: Market Insights

AC motors dominate the market by motor type owing to their broad range of applications, high efficiency, and straightforward design. They are widely utilized across industrial, commercial, and residential sectors due to their dependability, low maintenance needs, and compatibility with standard power supplies. In the industrial sector, AC motors are especially prevalent, driving equipment such as pumps, fans, conveyors, and various types of machinery. Their capability to maintain stable performance under both fixed and variable speed conditions makes them exceptionally adaptable. Moreover, technological advancements like variable frequency drives have significantly improved their efficiency and control, reinforcing their status as the most widely adopted and preferred motor type in the market.

Rotor Type: Market Insights

Inner rotor motors take the lead in the market when it comes to rotor types. Their compact design, impressive efficiency, and strong all-around performance make them a go-to choice for many applications. With the rotor positioned inside the stator, these motors are great at managing heat and delivering higher torque in a smaller footprint. This setup is especially useful in areas like industrial automation, robotics, and CNC machines where precision, speed, and space-saving matter most. Inner rotor motors also respond quickly and handle high speeds well, making them perfect for demanding tasks.

Power Rating: Market Insights

Electric motors with a power rating of less than 1 kW currently lead the market, due to their widespread use in low-power applications across residential, commercial, and light industrial sectors. These motors are used in everyday items like appliances, fans, pumps, small tools, and office equipment where high power is not essential, but efficiency and dependability are. Their small size, cost-effectiveness, and energy-saving benefits make them a popular choice among both manufacturers and consumers. With the ongoing rise of automation and smart technologies, especially in homes and small businesses, the demand for motors less than 1 kW continues to grow, firmly establishing them as the leading segment by power rating.

Voltage: Market Insights

Medium voltage electric motors lead the market in terms of voltage classification due to their efficiency in managing high power demands across industrial and heavy-duty operations. These motors, suited for large-scale industries like metal & mining, oil and gas, water treatment, chemical & petrochemical, and manufacturing. Medium voltage motors are valued for their ability to deliver high torque and maintain reliable performance. They provide key benefits such as enhanced energy efficiency, minimized current losses, and lower long-term operating costs, particularly in applications that require continuous and intensive operation. Their capability to handle substantial loads and operate effectively under tough conditions makes them the preferred option for many industrial applications, securing their dominant position in the market.

Output Power: Market Insights

When categorized by output power, fractional horsepower (HP) motors dominate the market, largely because of their widespread use in low-power applications. These motors, typically rated below 1 horsepower, are essential devices and equipment such as household appliances, HVAC systems, office machinery, and small industrial tools. Their compact size, energy efficiency, and cost-effectiveness make them ideal for tasks that don’t require high power but still need reliable performance. The growing demand for automation in small devices and the increasing use of compact energy-saving technologies have further boosted the popularity of fraction HP motors, making them the leading segment in terms of output power.

End Use: Market Insights

The industrial sector is the largest user of electric motors, primarily because these motors are integral to a wide range of manufacturing and processing activities. They play a crucial role in powering machinery involved in production, material transport, pumping, ventilation, and other mechanical functions. Industries such as chemical & petrochemical, food & beverage, aerospace & defense, water & wastewater, mining & metal, manufacturing, utilities, renewables, automation & others heavily depend on electric motors to operate equipment like conveyors, compressors, and mixers. The need for high efficiency, automation, and continuous operation makes electric motors essential in industrial settings, leading to much greater usage compared to residential or commercial sectors. Furthermore, industrial motors typically run at higher power levels and for extended periods, contributing significantly to total electricity consumption.

Regional: Market Insights

Asia-Pacific continues to lead the global electric motors market. This position is due to a mix of industrial growth, rapid urbanization, strong manufacturing infrastructure, and supportive government policies. Countries like China, India, Japan, and South Korea, have become a global manufacturing hub with a large automotive, electronics, and industrial production base. These sectors are major users of electric motors. The quick development of infrastructure and the electrification of rural and semi-urban areas also boost demand in sectors, such as water pumping, construction, and transportation. Furthermore, Asia-Pacific’s cost-effective manufacturing environment attracts global companies to establish production units, improving the regional supply chain and availability of electric motors. With ongoing investments in renewable energy, smart grid systems, and industrial IoT, Asia-Pacific is likely to stay the main force in the electric motors market

China emerges as a dominant force, serving as both a major producer and consumer of electric motors, supported by government initiatives aimed at promoting energy efficiency and the widespread adoption of electric vehicles.

China’s large industrial sector and its role as the world’s top producer and consumer of electric vehicles (EVs) significantly drive demand for electric motors. These motors are used in applications such as EV drivetrains, robotics, HVAC systems, and industrial automation. Additionally, government programs that promote energy efficiency and electrification, like China’s “Made in China 2025” and India’s “Make in India” campaigns, encourage local production and adoption of new motor technologies, including brushless DC (BLDC), stepper, and servo motors.

Similarly, India is experiencing notable growth driven by infrastructure expansion and manufacturing-focused programs like “Make in India.” The regional shift toward transportation electrification and the development of smart cities are further accelerating market growth.

Additionally, Asia-Pacific offers advantages such as a vast labor pool, competitive production costs, and growing foreign investment, positioning it as a prime destination for electric motor manufacturing. With continued advancements in automation, clean energy, and sustainable technologies, the region is well-positioned to retain its dominance in the electric motors market during the forecast period.

Competition: Electric Motors

The electric motor market is highly competitive, with key players focusing on innovation, product efficiency, and strategic partnerships to strengthen their market position. Major companies include Nidec Corporation, Johnson Electric, Maxon Motor, ABB Ltd., and AMETEK Inc. These players are investing in R&D to develop advanced motors tailored for applications in industrial, commercial, residential, transportation, agriculture sectors, driving healthy competition and technological advancement in the market.

NIDEC Corporation, Allied Motion, Inc., Siemens, Johnson Electric, Ametek Inc., ABB Ltd. are among the leading companies active in the market.

Nidec Corporation is one of the global leaders in the design, manufacture, and sale of electric motors and related components. Headquartered in Kyoto, Japan, Nidec has established itself as a key player in the industry, particularly in the small precision motors segment. The company’s diverse product portfolio includes motors for hard disk drives, automotive applications, home appliances, industrial equipment, and commercial use. Nidec is known for its innovative technologies and strong emphasis on energy efficiency, which has positioned it at the forefront of the shift toward electrification and automation across industries. With a global network of manufacturing and R&D facilities, Nidec continues to expand its presence and influence as a critical supplier in the electric motor market worldwide.

Allied Motion Technologies Inc. is a global technology leader and a prominent player in the electric motors industry, offering a comprehensive range of motors, generators, and drives for a wide array of industrial and commercial applications. Headquartered in Zurich, Switzerland, ABB leverages its deep expertise in electrification and automation to deliver high-efficiency motor solutions that support industries such as manufacturing, energy, transportation, and infrastructure. The company is known for its focus on digitalization and sustainability, integrating smart technologies and energy-efficient systems to enhance performance and reduce environmental impact. With a strong global footprint and a commitment to innovation, ABB plays a crucial role in driving the transformation toward more sustainable and connected industrial operations.

Recent Developments:

- In 2022, Allied Motion Technologies Inc. acquired ThinGap. ThinGap is a top developer and manufacturer of high-performance, zero cogging slot less motors. These motors are designed for use in applications that demand precise motion in compact, high-torque-to-volume solutions. This acquisition improves Allied’s precision motion capabilities. The addition of ThinGap also supports the company’s plan to offer complete motion solutions in the robotics, semiconductor, and instrumentation markets. ThinGap’s motors are particularly suited for smooth motion and high precision required in these fields.

- In 2024, ABB completed the acquisition of Aurora Motors. Aurora Motors has engineering and operations facilities in Shanghai, China, and a corporate office and distribution center in California. This acquisition is part of ABB’s strategy for profitable growth in its Motion Business Area. It will help the NEMA Motors Division improve its product offering, expand its supply chain, and better support its global customers.

- Siemens AG has approved the sale of Innomotics, a top electric motors and large drives company, to KPS Capital Partners, LP (“KPS”). The parties have signed a corresponding agreement. The purchase price is €3.5 billion. The sale to KPS is expected to close in the first half of fiscal 2025 and is subject to regular foreign-investment and merger control approvals. By selling Innomotics to KPS, Siemens has made further significant progress in improving its portfolio.

ELECTRIC MOTORS MARKET SNAPSHOT | |

Market size in 2024 | USD 148 Billion |

Market forecast in 2032 | USD 240 Billion |

Compound Annual Growth Rate (2025-2032) | 6.2% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Growth Drivers | Rising need for energy-efficient solutions, Rising demand across manufacturing sectors, Surge in electric vehicle (EV) production, Acceleration of industrial automation, Rising demand for HVAC across sectors |

Segments Covered | Motor Type, Rotor Type, Power Output, Voltage, Power Rating, End Use, And Region |

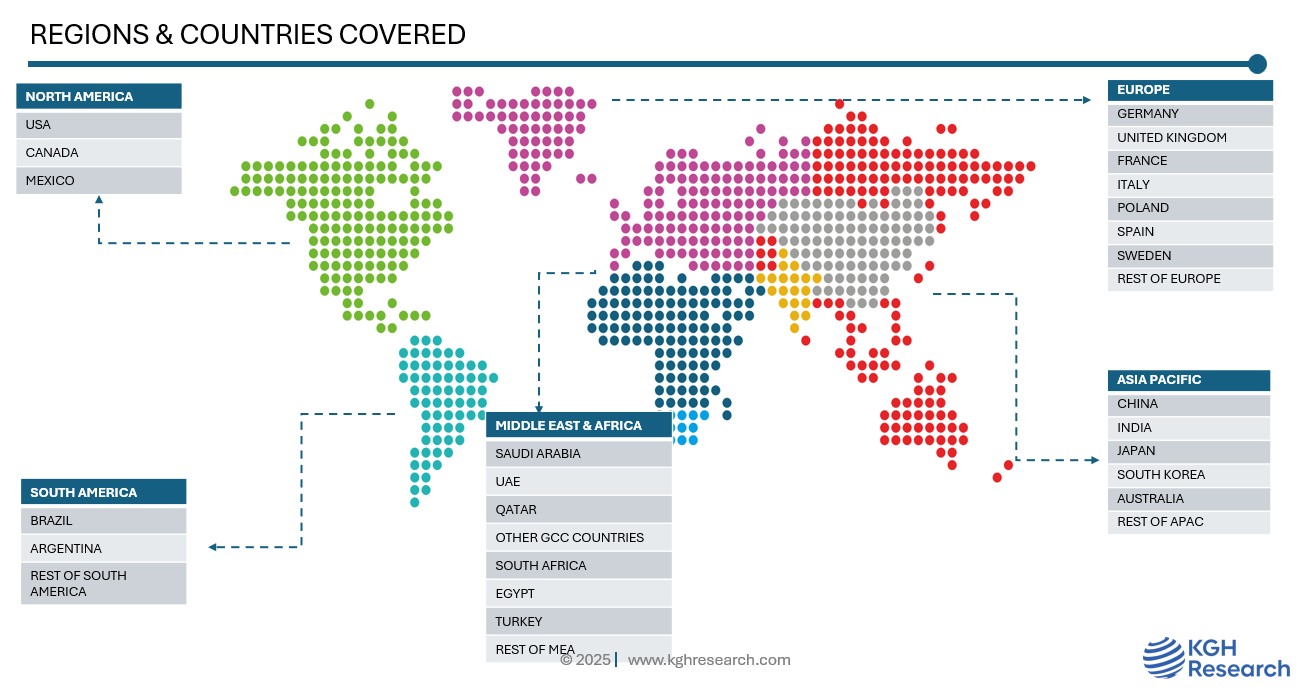

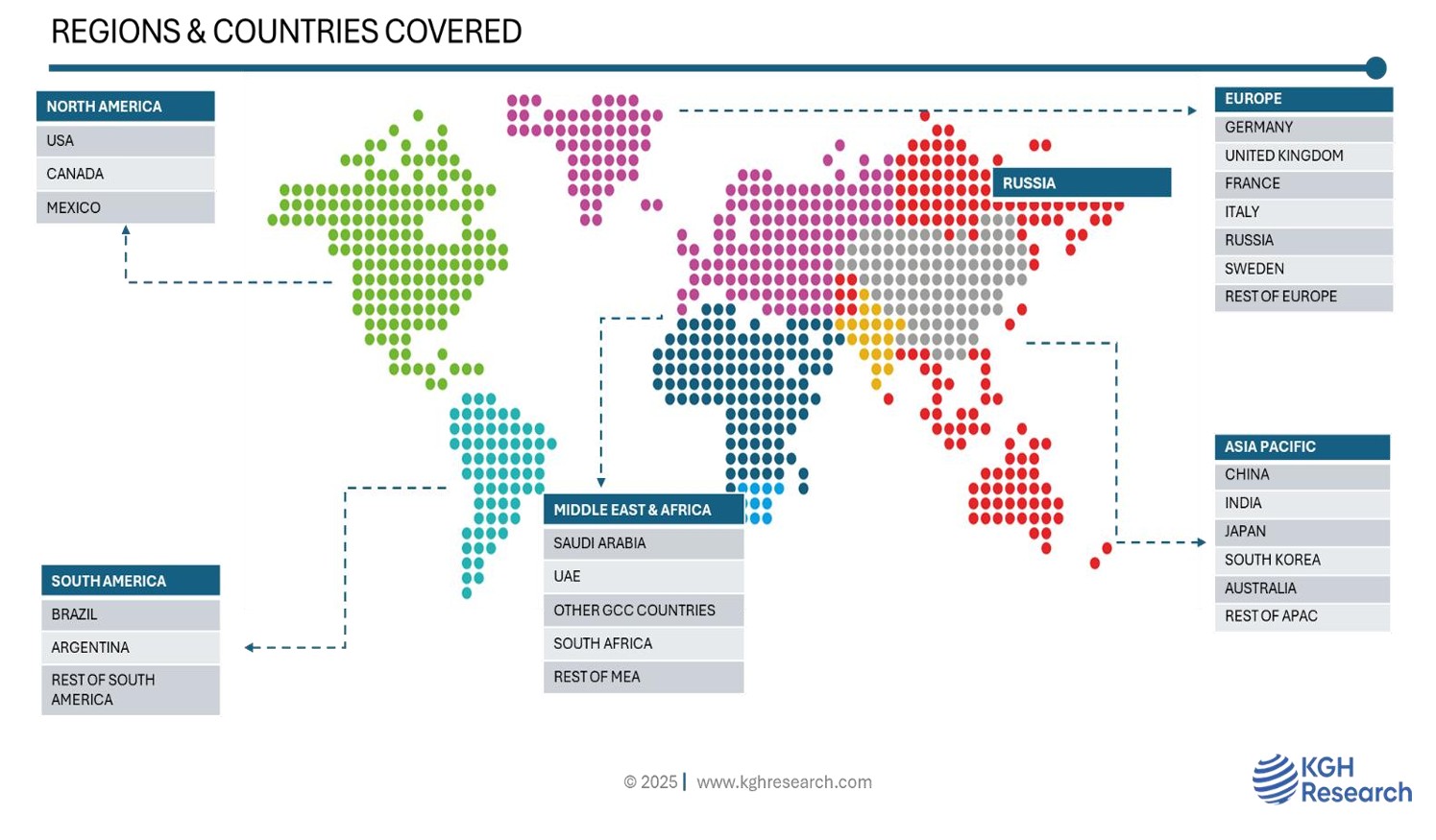

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, France, Sweden, Denmark, Russia, China, India, Japan, South Korea, Australia, UAE, South Africa, Brazil, Argentina |

Companies Profiled | NIDEC CORPORATION, JOHNSON ELECTRIC, SIEMENS, MAXON MOTOR, ABB LTD., AMETEK INC., WOLONG ELECTRIC GROUP, WEG, ALLIED MOTION TECHNOLOGIES, MINEBEAMITSUMI INC., ORIENTAL MOTOR CO., LTD., ELECTROCRAFT, INC., SCHNEIDER ELECTRIC, REGAL REXNORD CORPORATION, MOONS’, PORTESCAP, BÜHLER MOTOR GMBH |