Fall Protection Equipment Market (2022 - 2032)

FALL PROTECTION EQUIPMENT MARKET SIZE & SHARE BY TYPE (SOFT GOODS, HARD GOODS, ACCESS SYSTEMS, RESCUE EQUIPMENT, INSTALLED SYSTEMS, SERVICES & OTHERS), BY END USE (BUILDING & CONSTRUCTION, MANUFACTURING, POWER & UTILITY, MINING, TELECOM, TRANSPORTATION, OIL & GAS, WIND ENERGY AND, OTHERS) AND BY REGION & COUNTRY–FORECAST TO 2032

| Report Code: CONS&M9001-0101 | Number of Pages: 300 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: AUGUST 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

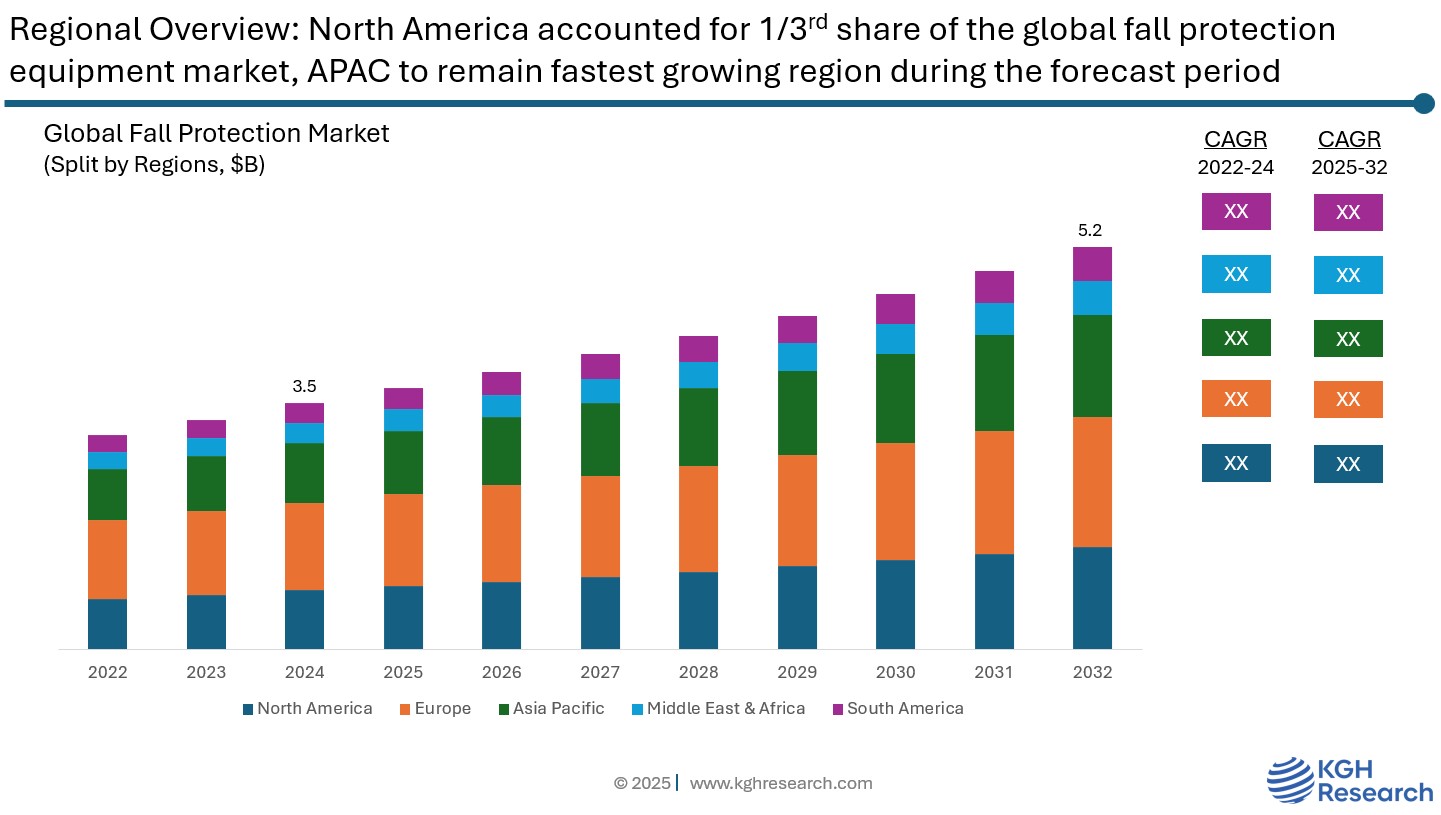

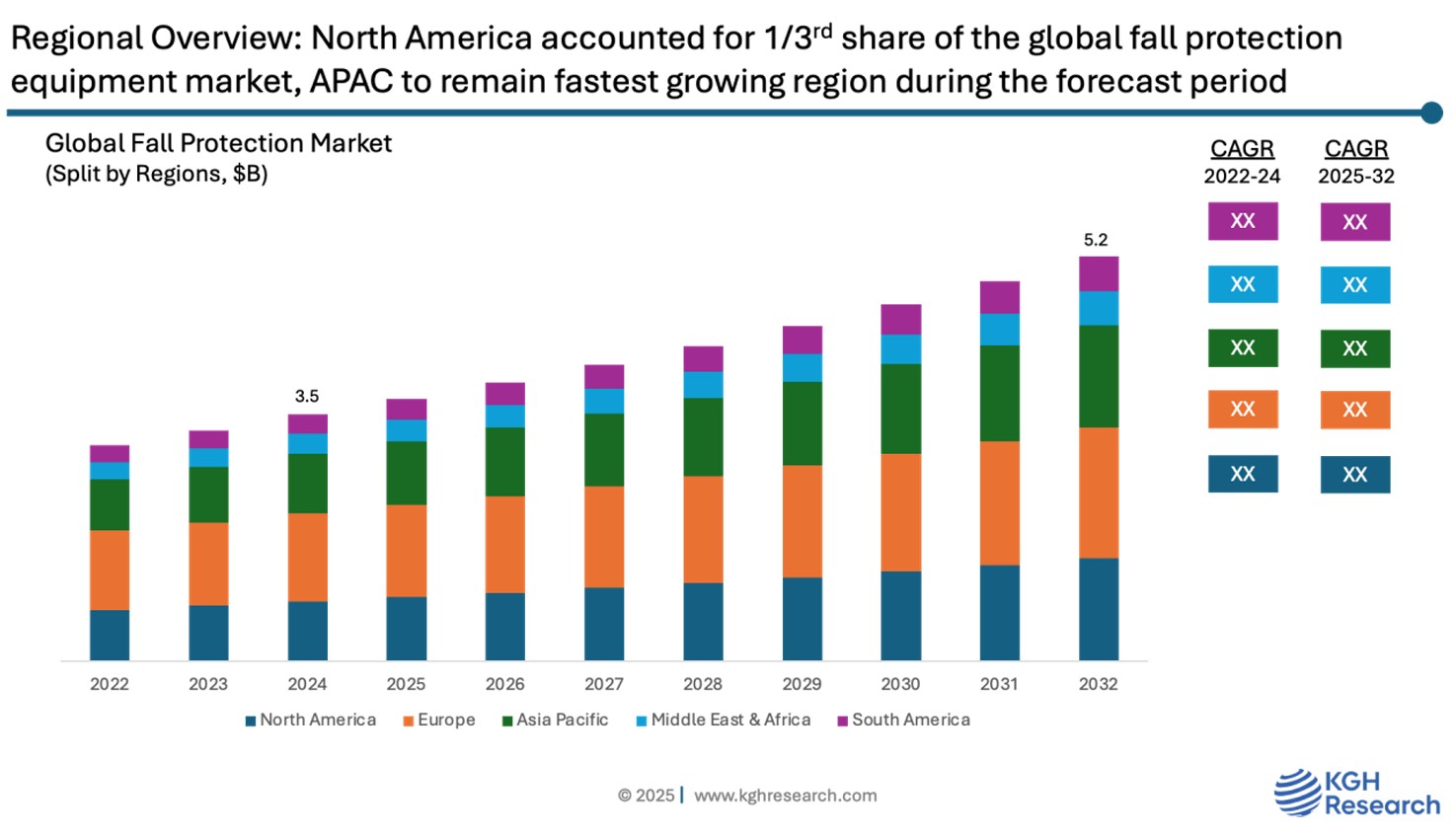

Market Overview: The global fall protection equipment market was estimated at US $3.5 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 5.0% from 2025 to 2032 to reach $5.2 billion by 2032. The market is driven by stricter regulations, a growing focus on worker safety, and an increase in workplace injuries, especially in high-risk sectors including mining, construction, oil and gas, manufacturing, and utilities. Organizations are being pushed to use certified fall prevention systems and equipment by governments and regulatory agencies such as the American National Standards Institute (ANSI), the Occupational Safety and Health Administration (OSHA), and their international counterparts. Furthermore, the need for dependable and creative fall prevention solutions is being fuelled by the growing infrastructure construction activities in emerging economies as well as the fast industrialization and urbanization of these regions. By improving product efficacy and user safety, technological innovations including smart harnesses, self-retracting lifelines, and IoT-integrated systems are also fuelling market expansion.

MARKET DYNAMIC

GROWTH DRIVERS:

- Stringent safety regulations (such as OSHA, ANSI, EN, ISO) and compliance requirements

- Rising awareness of worker safety and reduce workplace accidents

- Growth in oil & gas, telecom, construction renewable energy, and mining sectors are driving demand for fall protection systems

- Driver 4

NEW GROWTH OPPORTUNITIES:

- Rapid urban expansion and infrastructure projects, especially in developing regions

- Innovations like wearable tech, AI, and data analytics offer scope for smart safety solutions and predictive risk assessment

- Development of application-specific products

- Opportunity 4

MARKET RESTRAINTS:

- Lack of skilled labour for installation and training

- Lack of awareness in developing regions

- Product quality issues and counterfeit equipment

GROWTH HURDLES:

- Fragmented safety standards and compliance requirements across regions

- Reluctance to adopt modern safety practices and equipment may slow market growth

Type: Market Insights

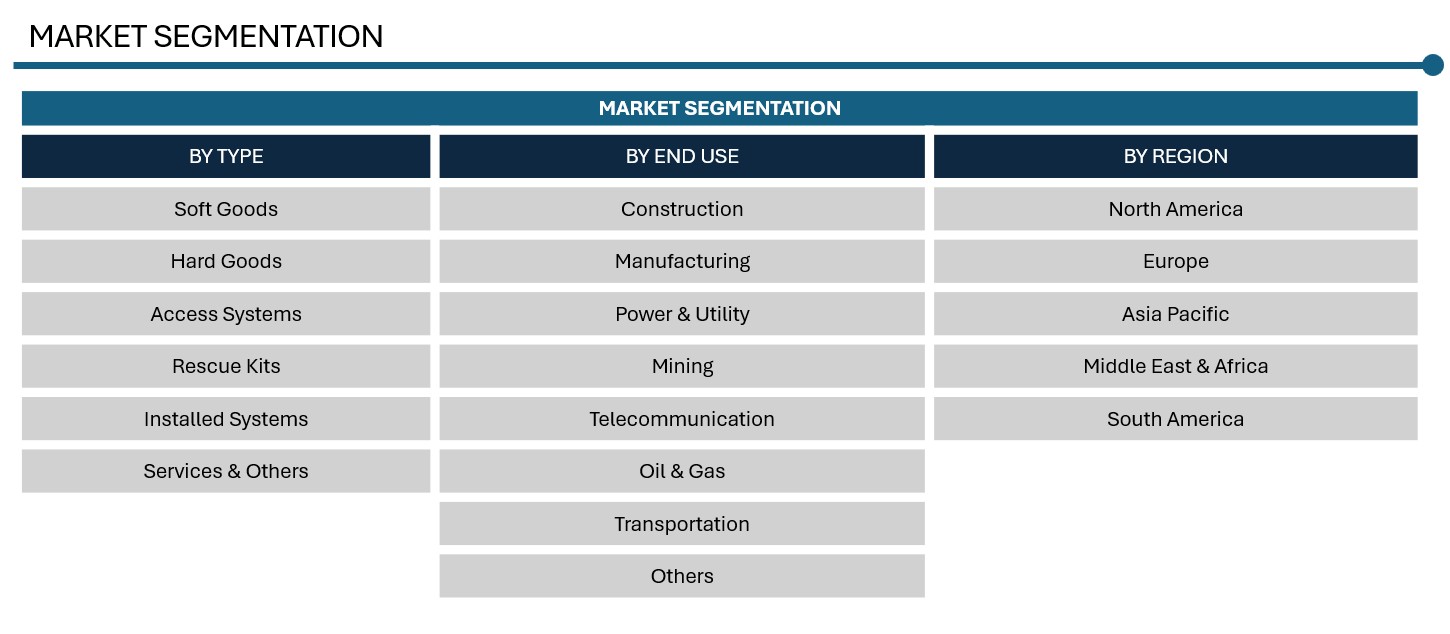

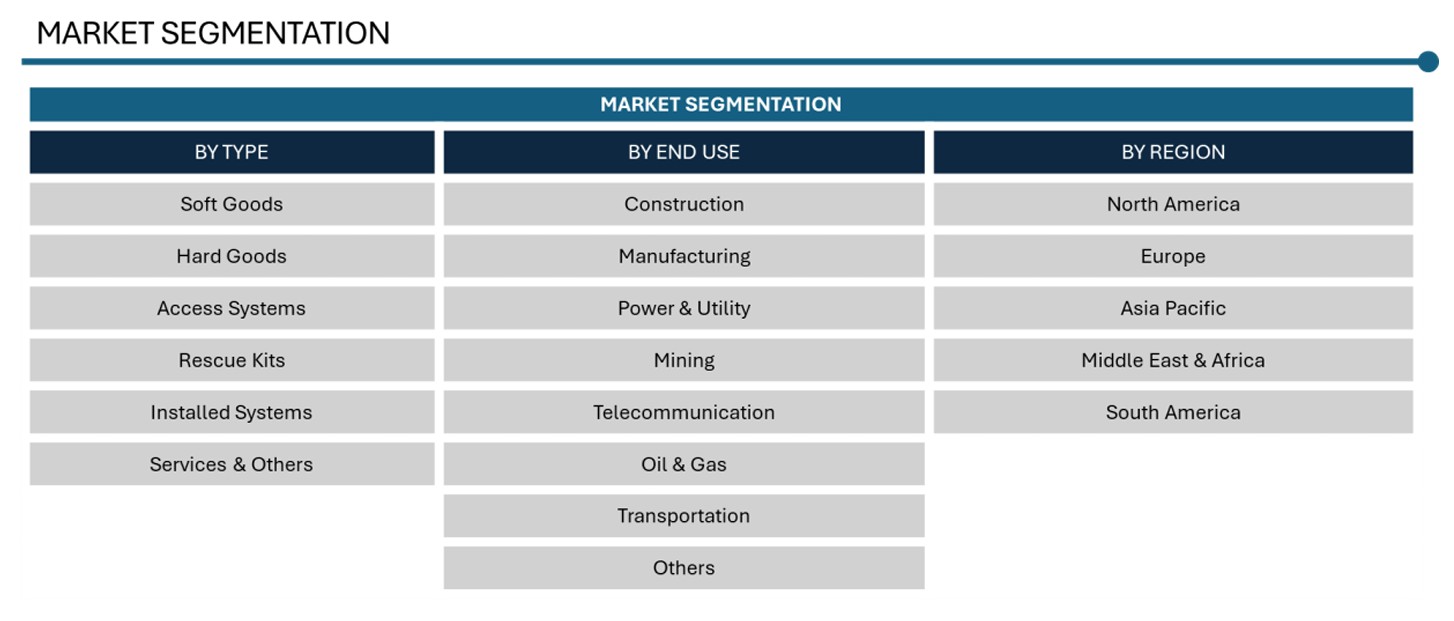

Soft goods, hard goods, access systems, rescue kits, installed systems, and services & others are the several categories into which the worldwide fall protection market is divided. The Hard Goods segment is regarded as the leading category and has the biggest market share among them. Important parts including body support systems, connectors, anchorage connectors, lanyards, and self-retracting lifelines (SRLs) are examples of hard goods. These items are crucial for guaranteeing the physical restraint and fall arrest of workers at heights and constitute the fundamental structural components of fall prevention systems. The extensive use of hard products in sectors like construction, oil and gas, utilities, and general manufacturing where there is a high risk of falls and stringent regulations is what fuels the huge demand for them. This segment’s dominance is also greatly influenced by the frequent need to replace worn-out hardware, the increasing use of technologically advanced devices (such RFID tracking or SRLs with built-in sensors), and their crucial function in personal fall arrest systems. Because they directly affect safety and regulatory compliance, hard products are frequently more capital-intensive and given priority for procurement as compared to soft goods, such as harnesses and belts, or services, such as inspection and training. The segment’s growth is further supported by the fact that, in order to guarantee the safety of sizable on-site workforces, employers usually make significant investments in strong, long-lasting hard products in large-scale infrastructure projects.

End Use: Market Insights

The global fall protection market, by end use is segmented into construction, manufacturing, mining, power & utilities, telecommunication, oil & gas, transportation and others. The construction end use is the dominant end-use industry in the global fall protection market. This is primarily due to the inherently hazardous nature of construction work, where employees regularly operate at elevated heights on scaffolding, rooftops, towers, and unfinished structures. Falls are one of the leading causes of occupational injuries and fatalities in construction, making fall protection equipment not just essential, but mandatory in most countries under stringent safety regulations such as OSHA (Occupational Safety and Health Administration) in the U.S. and EU-OSHA in Europe. Governments and industry bodies across the globe mandate the use of fall arrest systems, body harnesses, anchorage connectors, and other fall protection solutions on construction sites. With the global increase in urbanization and large-scale infrastructure projects especially in Asia-Pacific, the Middle East, and South America the construction industry continues to experience substantial growth, directly boosting demand for fall protection systems.

Power & utility and telecommunication sectors demand fall protection for workers operating on towers, poles, and turbines, particularly with the growth of renewable energy and 5G infrastructure. In mining, harsh and hazardous environments necessitate rugged safety gear for work at heights and in confined spaces. The transportation segment, including railways, aviation, and ports, uses fall protection for cargo handling and vehicle maintenance. The oil & gas industry also contributes significantly, given the elevated work environments on rigs and refineries, where stringent safety standards are critical.

Regional: Market Insights

Asia Pacific stands at the forefront of the global fall protection market, driven by a powerful mix of economic growth, industrial progress, evolving safety regulations, and a rising focus on worker well-being. Nations like China, India, Japan, South Korea, and others across Southeast Asia are during massive infrastructure development spanning housing, commercial spaces, transport systems, airports, and smart city initiatives and developments. As construction activity strengthens, the need to protect workers operating at height is also increasing, making fall protection systems more crucial than ever. Beyond construction, the region’s manufacturing sector especially in China and India is expanding rapidly. With global firms setting up production hubs to tap into cost-effective labour and large markets, there’s a growing need for reliable safety gear. Workers are frequently exposed to fall risks during equipment maintenance and factory operations, increasing demand for harnesses, anchorage systems, and access solutions. The telecom sector is also booming, fuelled by widespread 4G/5G rollouts and rural connectivity drives. This has led to more technicians working on towers and elevated platforms, requiring specialized fall protection tools like tower climbing kits and self-retracting lifelines. At the same time, renewable energy projects particularly wind and solar are expanding across the region, pushing the utilities sector to adopt robust fall safety measures for crews handling installations and upkeep on tall structures. Governments are playing a key role too. Regulatory frameworks, such as India’s Factories Act and China’s Work Safety Law, are being strengthened, pushing companies to meet higher safety standards with certified fall protection equipment. Growing attention to ESG goals, employee safety, and the financial risks of workplace injuries are prompting firms to prioritize investment in safety solutions. Together, these trends supported by a thriving base of local manufacturers, safety trainers, and service providers are solidifying Asia Pacific’s position as the most active and influential region in the global fall protection landscape.

China plays a pivotal role in driving the fall protection market within Asia Pacific, owing to its massive industrial base, rapid urbanization, and strict enforcement of workplace safety standards. As the world’s largest construction market, China is rapidly investing in large-scale infrastructure projects including high-rise buildings, bridges, railways, and smart cities, all of which require wide-ranging fall protection solutions to ensure worker safety at height. The government has been actively strengthening safety laws, such as the Work Safety Law of the People’s Republic of China, which mandates the use of protective equipment and places accountability on employers to maintain safe working conditions. Beyond construction, China’s manufacturing and energy sectors are also major contributors to fall protection demand. With sprawling industrial facilities and a strong focus on renewable energy development mainly wind and solar power there is a growing need for fall protection gear such as body harnesses, self-retracting lifelines, anchor systems, and rescue equipment. Additionally, China’s telecommunication expansion, fuelled by 5G deployment and rural connectivity programs, is creating new demand for tower safety systems and vertical access solutions. China is not only a major consumer but also a leading manufacturer and exporter of fall protection equipment. Domestic companies and global safety brands alike operate in China, benefiting from cost-effective production and a skilled workforce. The presence of a well-developed supply chain, combined with government-backed safety awareness campaigns and growing adoption of international safety standards, further boosts the nation’s impact in the global fall protection market. As safety continues to move up the agenda in China’s evolving industrial landscape, its leadership position in this market is expected to strengthen even further.

Competition: Fall Protection Equipment Market

The fall protection market is highly competitive, with numerous global and regional players striving to strengthen their market positions through continuous product innovation, technological advancements, and strategic collaborations. Leading manufacturers are increasingly focusing on developing smart safety solutions such as harnesses with sensor technology, self-retracting lifelines with automatic locking systems, and integrated IoT-based monitoring tools to enhance worker safety and real-time risk detection. Moreover, many companies are forming strategic alliances, acquiring niche safety solution providers, and expanding their geographical presence to cater to the rising demand across various end-use industries like construction, oil & gas, utilities, and telecom. These players are also investing heavily in training programs, certification compliance, and customer education to build trust and loyalty in a market where reliability and regulatory compliance are critical. As safety regulations become stricter worldwide, innovation, customization, and service excellence have become key differentiators in this competitive landscape. Leading players are continually innovating to meet the changing needs of the industry. Key companies include, 3M Company, Honeywell International Inc., MSA Safety Inc., Skylotec GmbH, W.W. Grainger, Inc., GF Protection Inc., Guardian Fall Protection Inc., Kee Safety, Inc., FallTech, Delta Plus Group, Gravitec System, Inc., The Petzl Group, Werner Co.

3M Company is a global leader in the fall protection market, it has strong innovation capabilities and diverse product portfolio. After acquiring Capital Safety in 2015, 3M integrated well-known brands such as DBI-SALA® and Protecta®, strengthening its position as the largest player in the global fall protection industry. The company offers a wide range of safety solutions including full-body harnesses, self-retracting lifelines, anchorage systems, rescue devices, and dropped-object prevention equipment, catering to industries like construction, oil & gas, utilities, telecommunications, and transportation. 3M focuses heavily on product innovation, integrating advanced technologies such as RFID-enabled safety gear and smart inspection systems to enhance worker protection and streamline compliance. With a strong global footprint, robust distribution network, and a reputation for quality and reliability, 3M continues to dominate the fall protection space by addressing both premium and cost-conscious market segments through its dual-brand strategy.

FALL PROTECTION EQUIPMENT MARKET SNAPSHOT | |

Market Size In 2025 | USD 3.5 BILLION |

Market Forecast In 2032 | USD 5.2 BILLION |

Compound Annual Growth Rate (2025-2032) | 5.0% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Region Dominance | Asia Pacific |

Country Dominance | China |

Growth Driver | Stringent safety regulations (such as OSHA, ANSI, EN, ISO) and compliance requirements Rising awareness of worker safety and reduce workplace accidents Growth in oil & gas, telecom, construction renewable energy, and mining sectors are driving demand for fall protection systems |

Segments Covered | BY TYPE, BY END USE, AND BY REGION & COUNTRIES |

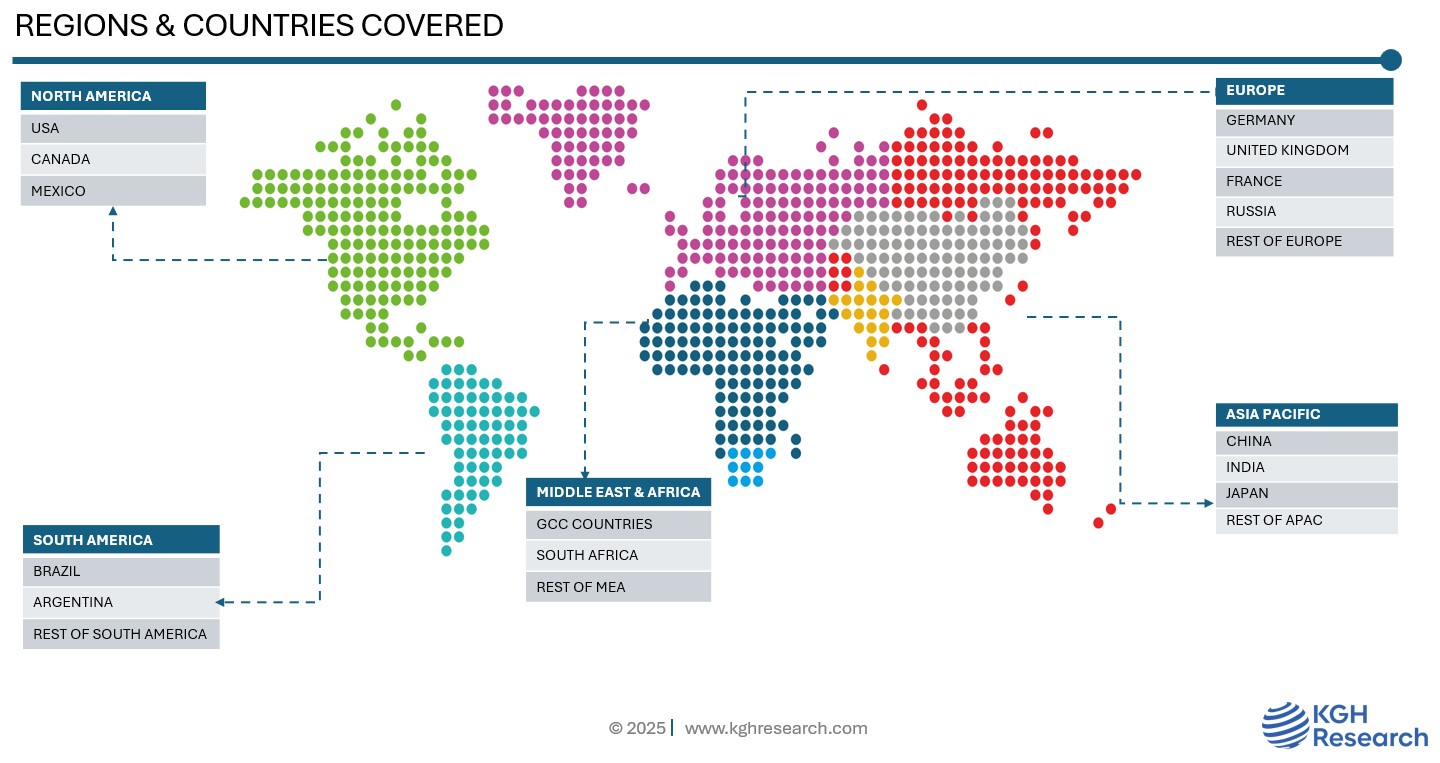

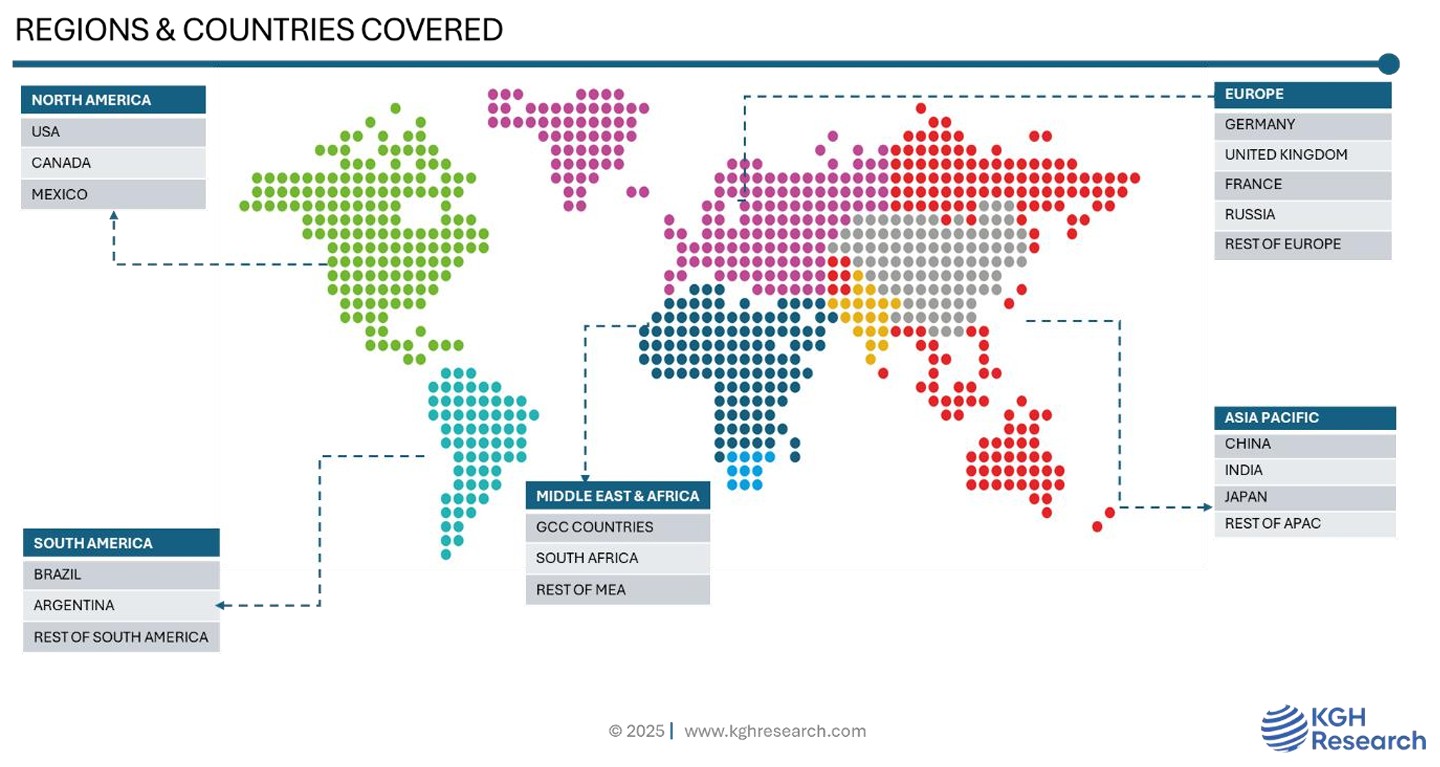

Regions Covered | NORTH AMERICA, EUROPE, ASIA PACIFIC, SOUTH AMERICA, MIDDLE EAST & AFRICA |

Countries Covered | USA, CANADA, MEXICO, UK, GERMANY, FRANCE, RUSSIA, REST OF THE EUROPE, CHINA, INDIA, JAPAN, REST OF APAC, BRAZIL, ARGENTINA, REST OF THE WORLD |

Companies Profiled (20+) | 3M COMPANY, HONEYWELL INTERNATIONAL INC., MSA SAFETY INC., SKYLOTEC GMBH, W.W. GRAINGER, INC., GF PROTECTION INC., GUARDIAN FALL PROTECTION INC., KEE SAFETY, INC., FALLTECH, DELTA PLUS GROUP, GRAVITEC SYSTEM, INC., THE PETZL GROUP, WERNER CO., AND MANY MORE. |