GCC DATA CENTER MARKET SIZE & SHARE BY INFRASTRUCTURE TYPE (NETWORK & IT EQUIPMENT, COOLING COMPONENTS, POWER COMPONENTS, AND OTHER GENERAL INFRASTRUCTURE), BY DATA CENTER TYPE (HYPERSCALER, COLOCATION, ENTERPRISE, AND CRYPTO), BY WORKLOAD (AI BASED, NON-AI BASED, AND CRYPTOCURRENCY MINING), BY SOLUTION & SERVICES, BY END USE, BY HARDWARE, SOFTWARE, AND SERVICE, AND BY KEY COUNTRIES – FORECAST TO 2032

Report Code: ICT7004-0603

Number of Pages: 300

Report Format: PDF, EXCEL, PPT

Trend Year: 2022 – 2024

Forecast Period: 2025 – 2032

Publish Date: FEBRUARY 2026

Report Summary

Tables of Content

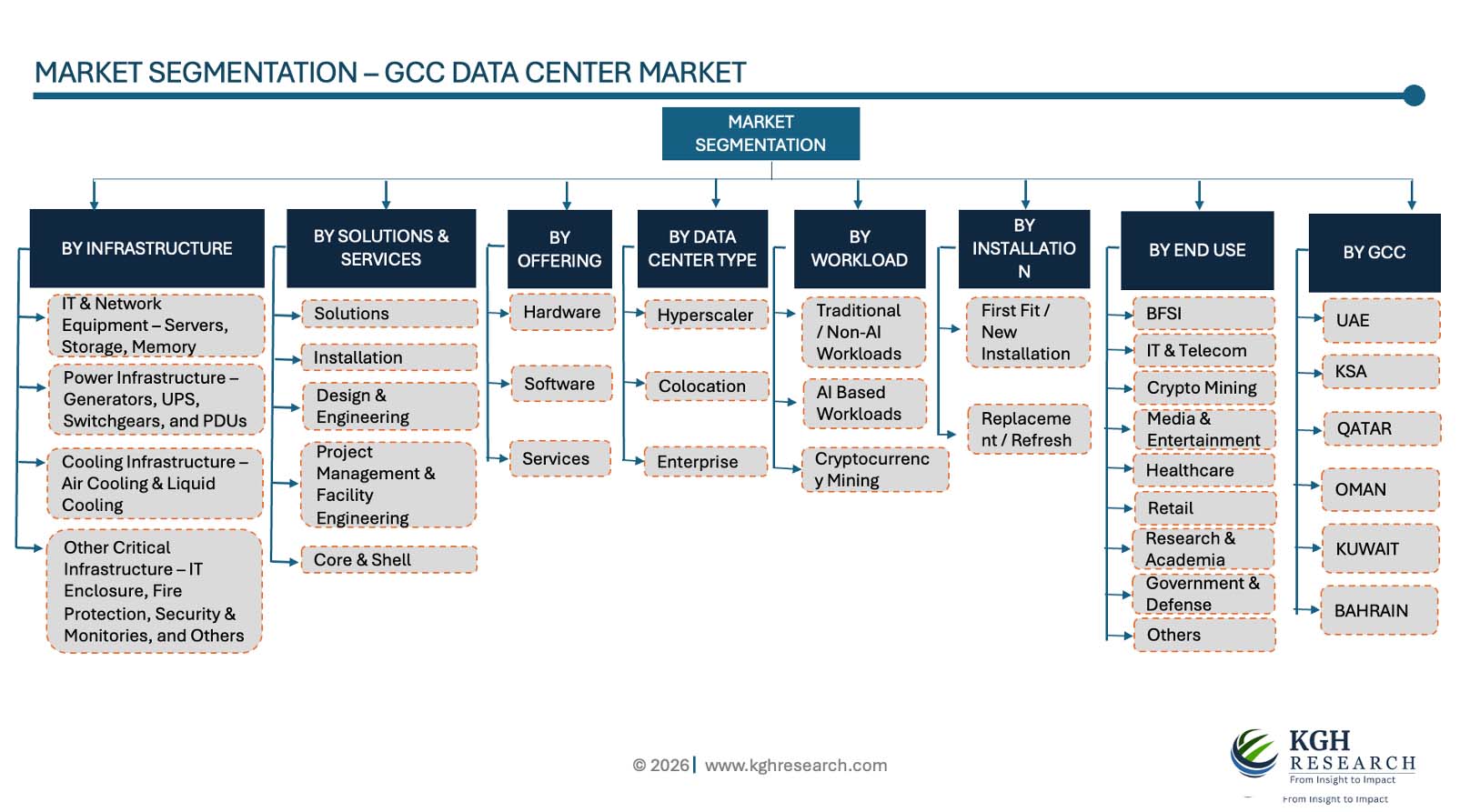

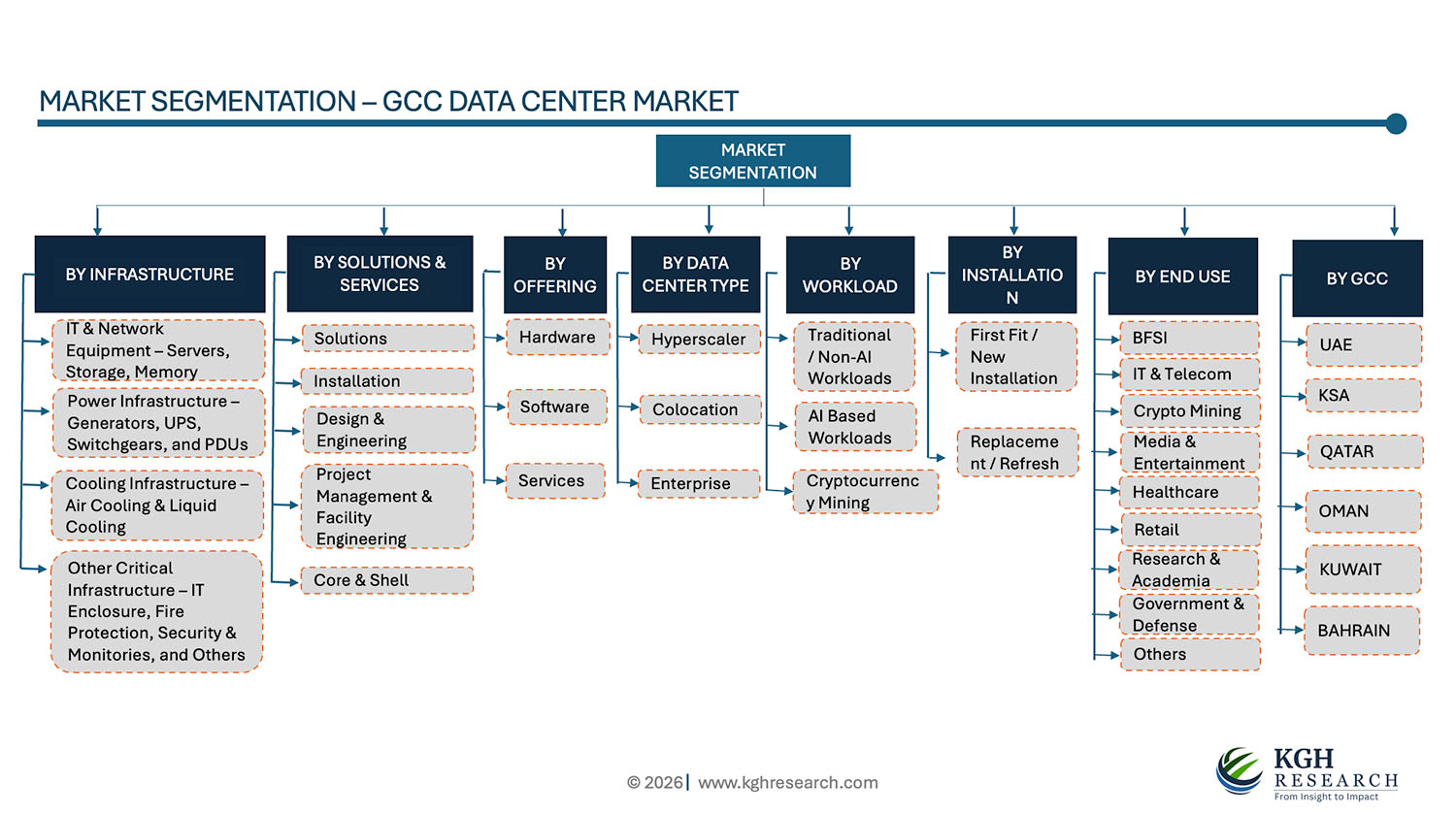

Segmentation

Methodology

User License & Pricing

Sample Copy

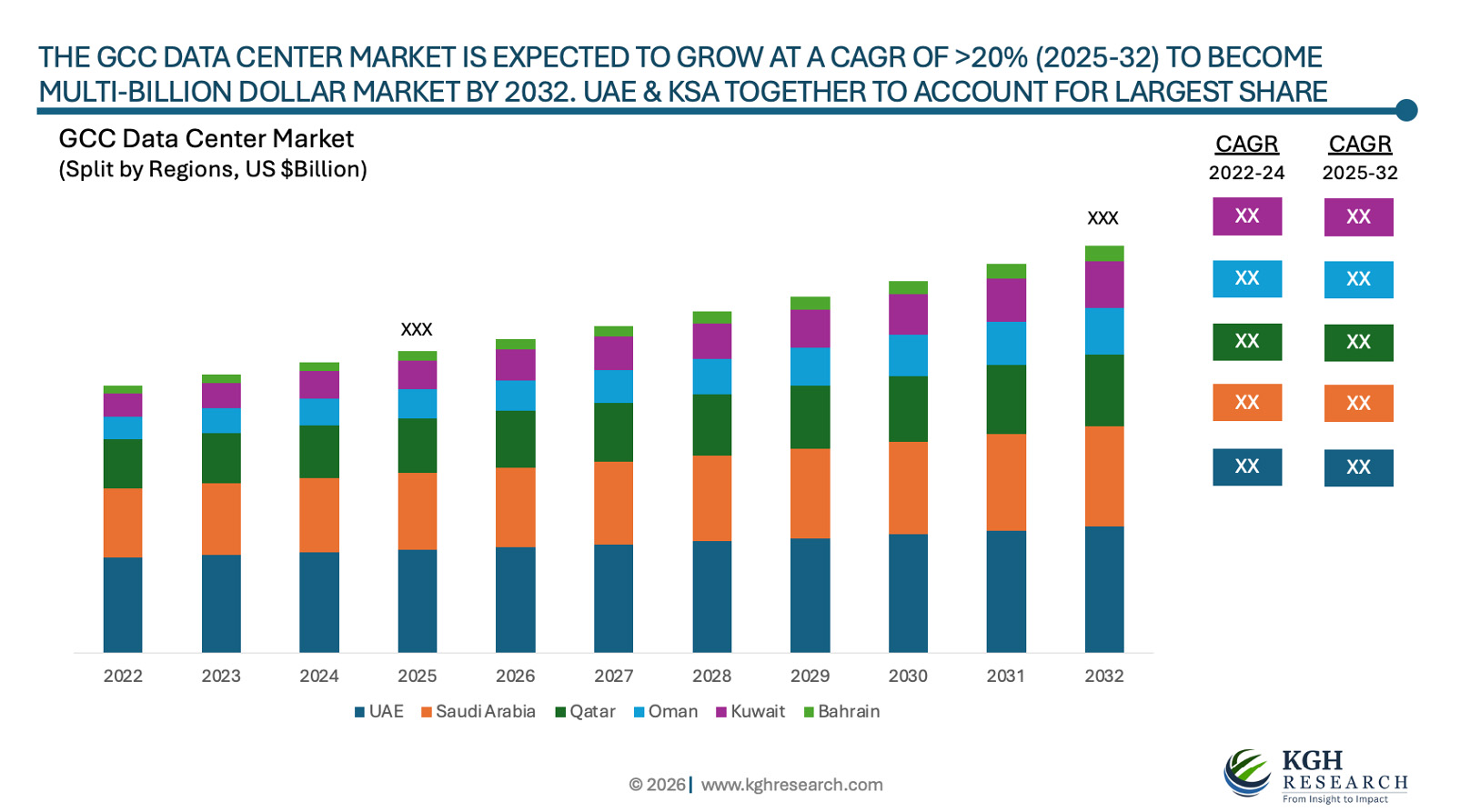

Market Overview: The GCC data center (infrastructure) market is estimated at US $XX Billion (incl. replacement/refresh spending) in 2025, and this market is expected to grow at a CAGR (2025 – 2032) of >20% to become a US $XX Billion market opportunity by 2032. The growth is attributed to a convergence of structural and technology-led demand drivers across the GCC region. Rapid enterprise migration to cloud environments, combined with the localization strategies of global hyperscalers, is significantly increasing the need for scalable colocation and build-to-suit facilities. At the same time, governments initiatives & support across the region are advancing national digital transformation programs, smart city initiatives, and AI adoption frameworks, all of which require resilient, low-latency data infrastructure within sovereign borders.

MARKET DYNAMIC

GROWTH DRIVERS:

Rapid adoption of AI/ML workloads

Data Sovereignty & Cybersecurity Regulations

Local Government Support and Digital Transformation Program across GCC Region

Driver 4: Refer Report

Driver 5: Refer Report

NEW GROWTH OPPORTUNITIES:

AI-Ready Infrastructure Development

Integration of renewables, district cooling, and energy-efficient architectures

Increasing rack density to meet the demand for compute heavy workloads driving demand for expensive, but highly reliable liquid cooling solutions

Growth Opportunities 4: Refer Report

Growth Opportunities 5: Refer Report

MARKET RESTRAINTS:

Rapid evolution in chip architectures and cooling technologies may shorten infrastructure refresh timelines.

Market Restrainer 2: Refer Report

Market Restrainer 3: Refer Report

GROWTH HURDLES:

Regulatory pressure to reduce excessive heat generation, water usage, and greenhouse gas emission from data center and ancillary industries supporting data centers putting immense pressure on data center owners & operators and infrastructure providers

Growth Hurdle 2: Refer Report

Growth Hurdle 3: Refer Report

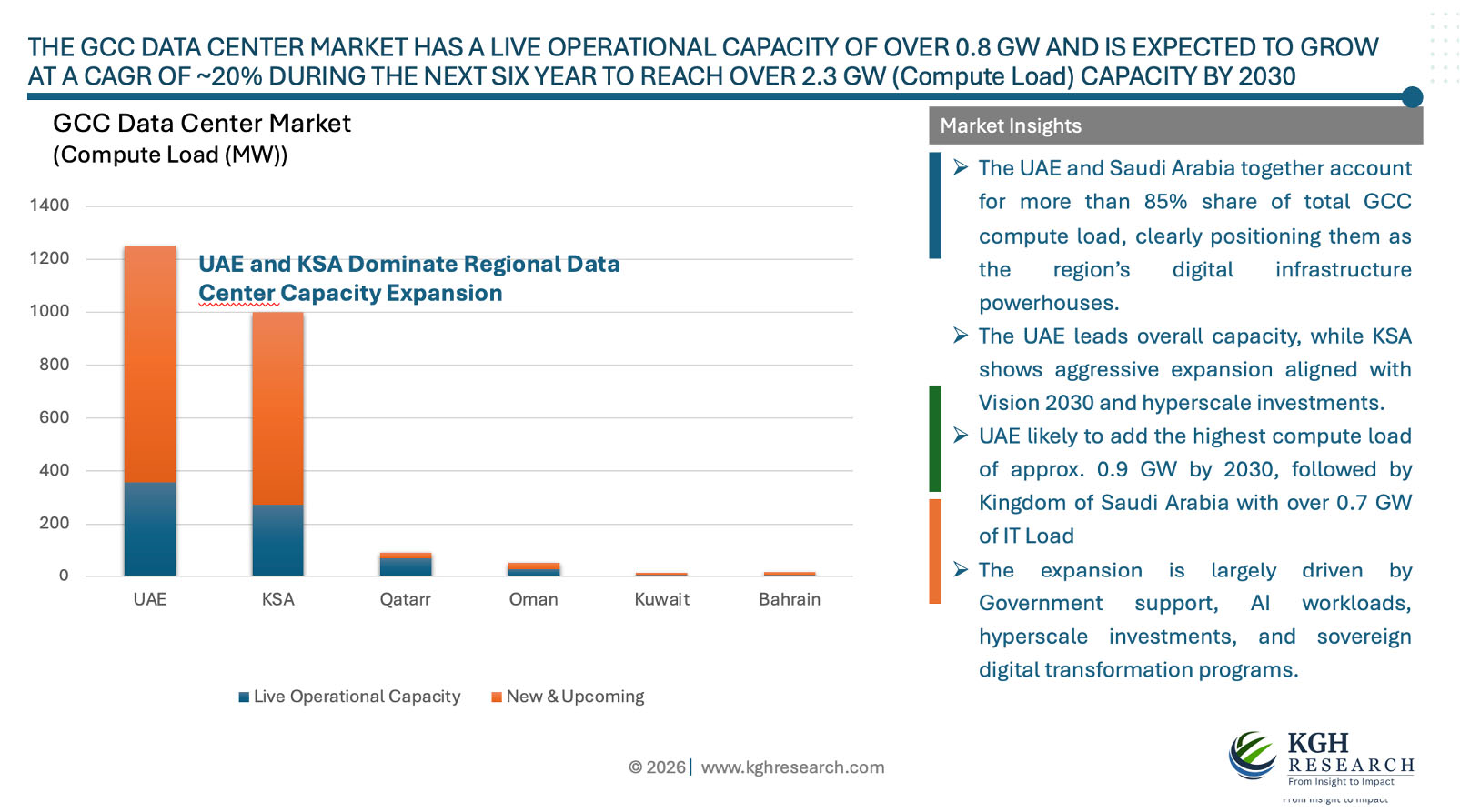

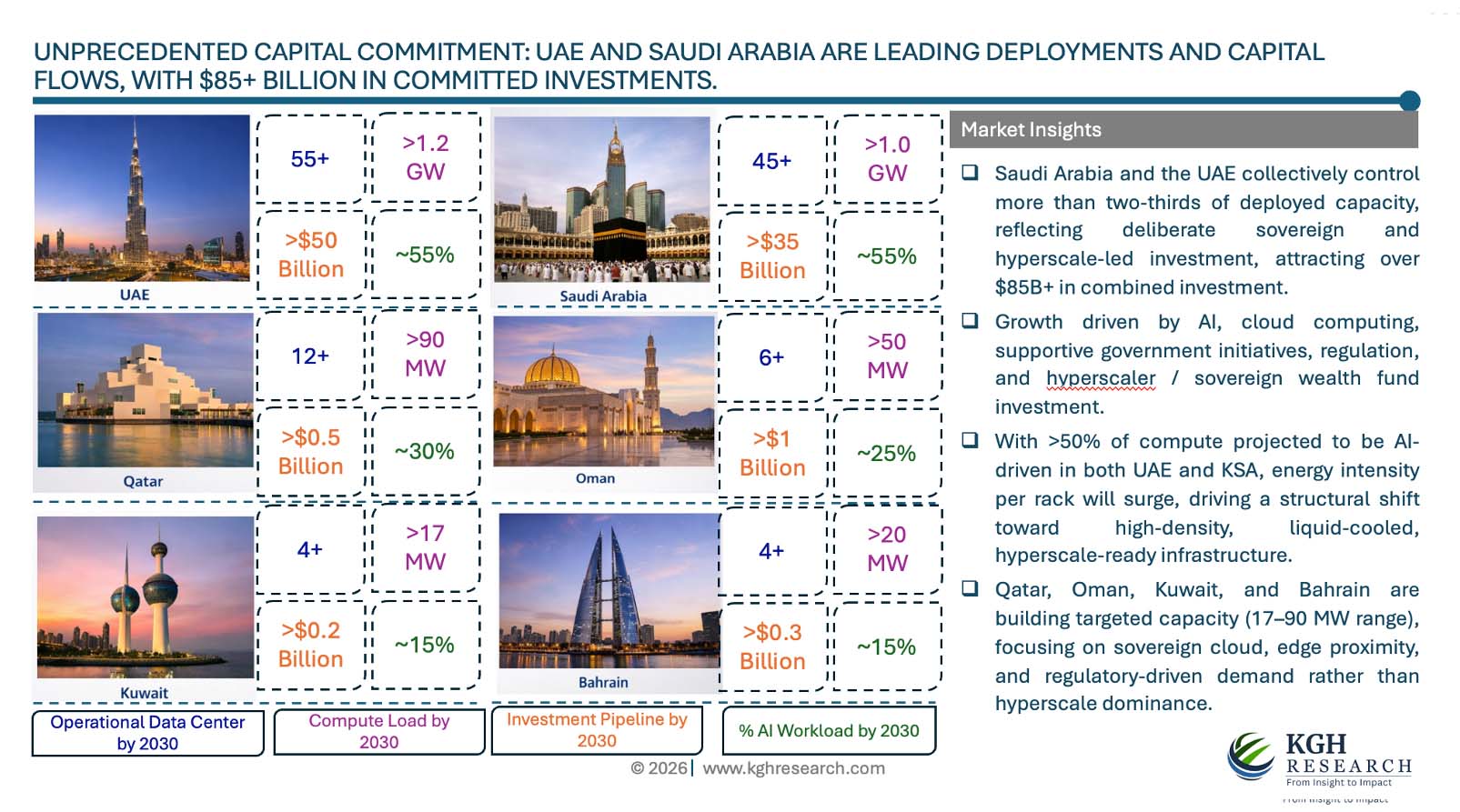

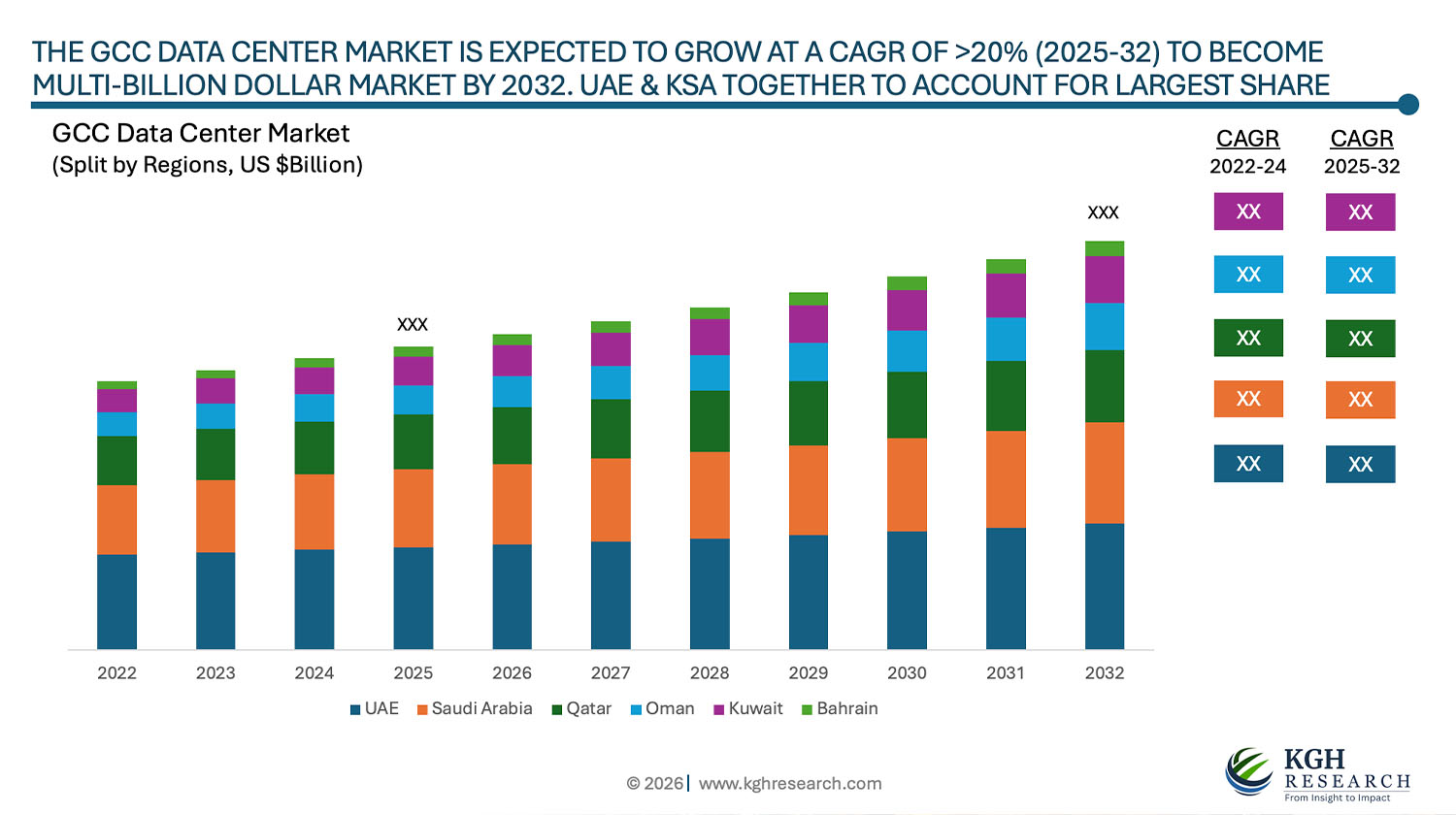

The UAE and Saudi Arabia together account for more than 85% share of total GCC compute load, clearly positioning them as the region’s digital infrastructure powerhouses.

The UAE leads overall capacity, while KSA shows aggressive expansion aligned with Vision 2030 and hyperscale investments.

UAE likely to add the highest compute load of approx. 0.9 GW by 2030, followed by Kingdom of Saudi Arabia with over 0.7 GW of IT Load

The expansion is largely driven by Government support, AI workloads, hyperscale investments, and sovereign digital transformation programs.

Saudi Arabia and the UAE collectively control more than two-thirds of deployed capacity, reflecting deliberate sovereign and hyperscale-led investment, attracting over $85B+ in combined investment. Growth driven by AI, cloud computing, supportive government initiatives, regulation, and hyperscaler / sovereign wealth fund investment.

With >50% of compute projected to be AI-driven in both UAE and KSA, energy intensity per rack will surge, driving a structural shift toward high-density, liquid-cooled, hyperscale-ready infrastructure.Qatar, Oman, Kuwait, and Bahrain are building targeted capacity (17–90 MW range), focusing on sovereign cloud, edge proximity, and regulatory-driven demand rather than hyperscale dominance.

By Data Center Type: Market Insights

Colocation deployments in terms of GW of IT load was the highest in 2025 accounted for at least XX% share, while in terms of CAPEX in Hyperscaler accounted for approx. XX% share and is likely to grow faster than Colocation and Enterprise based data centers during the forecast period in the GCC region.

By Workload: Market Insights

AI based workloads within the data center are likely to grow at around 30% CAGR, while the traditional data center installation to grow at approx. 10% CAGR during the forecast period. An AI-enabled data centre can easily cost 2X more than a conventional one. In 2032, AI based data centers accounted for more than 50% share of the GCC Data Centre deployment

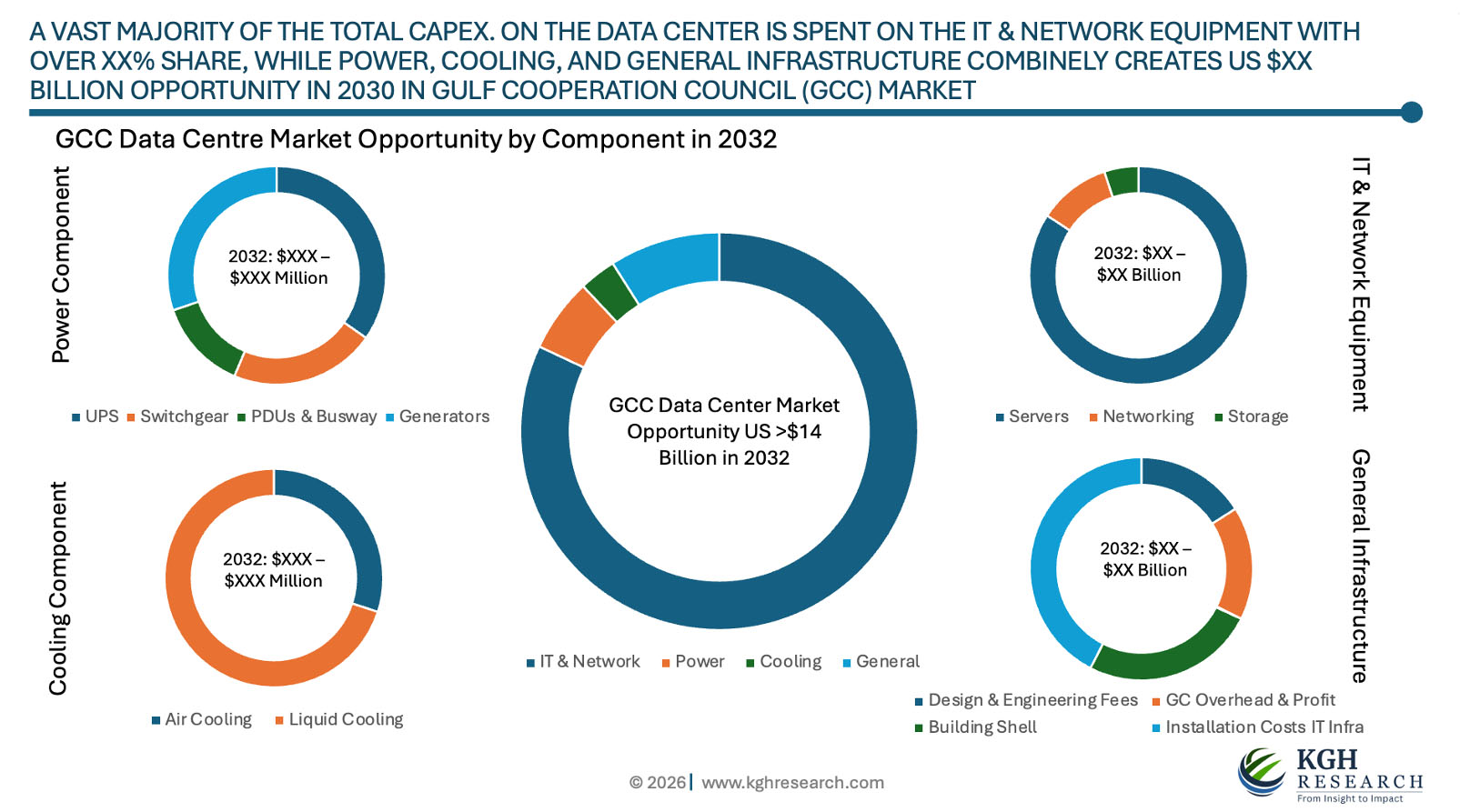

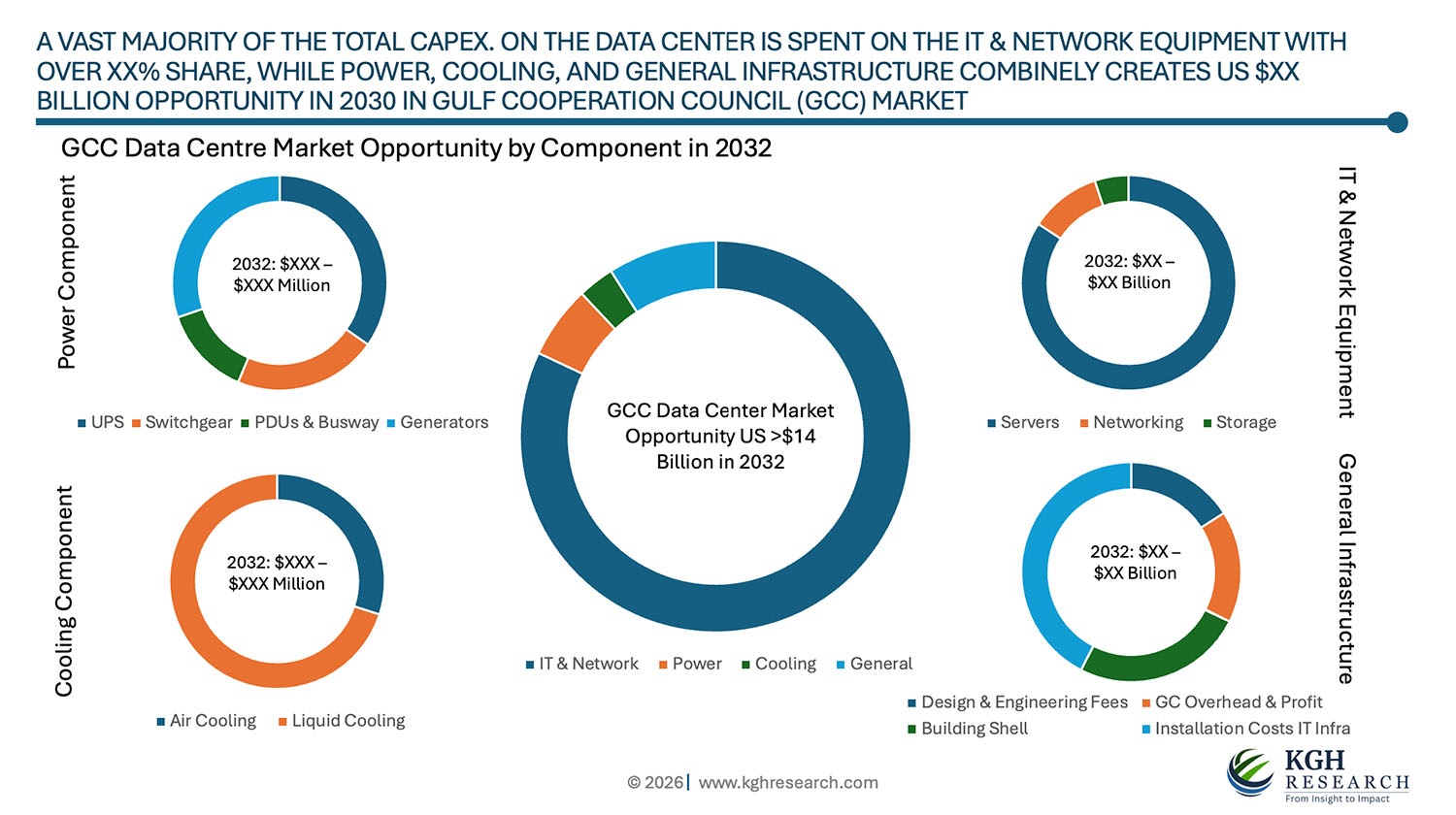

By Infrastructure: An average spent (CAPEX) on establishing a data center with 1 MW of IT load could typically cost in between US $35 to $50 Million incl. Network & IT Equipment, varies due to traditional versus AI based workloads.

Network & IT Equipment includes Servers, Networking, and Storage equipment accounted for more than two-third share of the GCC data center infrastructure CAPEX market. The market is mainly driving by increasing investment on compute heavy AI enabled advanced and expensive GPUs and CPUs within DC and a major portion of the market is replacement / refresh network and IT equipment. Data centre networks and IT equipment are the backbone of modern digital infrastructure, supporting everything from cloud computing to AI applications. The growing demand for data-driven services, cloud migration, AI, and IoT connectivity are key growth drivers, fuelling the need for high-speed, scalable networks and robust IT hardware.

Power equipment, including PDUs (Power Distribution Units), switchgears, generators, and UPS (Uninterruptible Power Supplies), are critical for ensuring reliable, efficient, and uninterrupted power delivery. The rapid growth of cloud computing, big data analytics, and AI-driven applications are key growth drivers, increasing the demand for resilient power solutions to support 24/7 operations. Additionally, the push for energy efficiency and sustainability has led to innovations in advanced UPS systems and smart PDUs that optimize power usage. The rise of edge computing and hyperscale data centres further drives the need for scalable, high-capacity power equipment capable of handling dynamic workloads while minimizing downtime and energy costs. A typical investment on power infrastructure could cost in between US $1.5 to $2.5 Million per MW IT Load within a data centre

Cooling Infrastructure: With the emergence of generative & specialized AI and machine learning place substantial demands on computing resources. This requires specialized high-density semiconductors like GPUs, which in turn generate a lot of heat, driving higher rack densities necessitating more advanced cooling infrastructure in data centers, driving investment in advanced liquid cooling direct to chip and immersion cooling technologies. Liquid cooling offers superior thermal management, lower energy consumption, and the ability to support high-density deployments, making it a key technology for future-proofing data center operations in an era of exponential data growth.

GCC DATA CENTER MARKET SNAPSHOT

Market size in 2025

US$ XX Billion

Market forecast in 2032

US$ XX Billion

Compound Annual Growth Rate (2025-2032)

X.X%

Historical Data (Years)

2022-2024

Forecast Data (Years)

2025-2032

Major Drivers & Trends

Growing Data Centre Market, Increasing Deployments of Generative AI and Specialized AI based Data Centers

Segments Covered

By Infrastructure Type, By Data Center Type, by Component & Services, by Offering, by Workload, by Installation, by End Use, and by Countries

Countries Covered

UAE, Saudi Arabia, Qatar, Rest of GCC

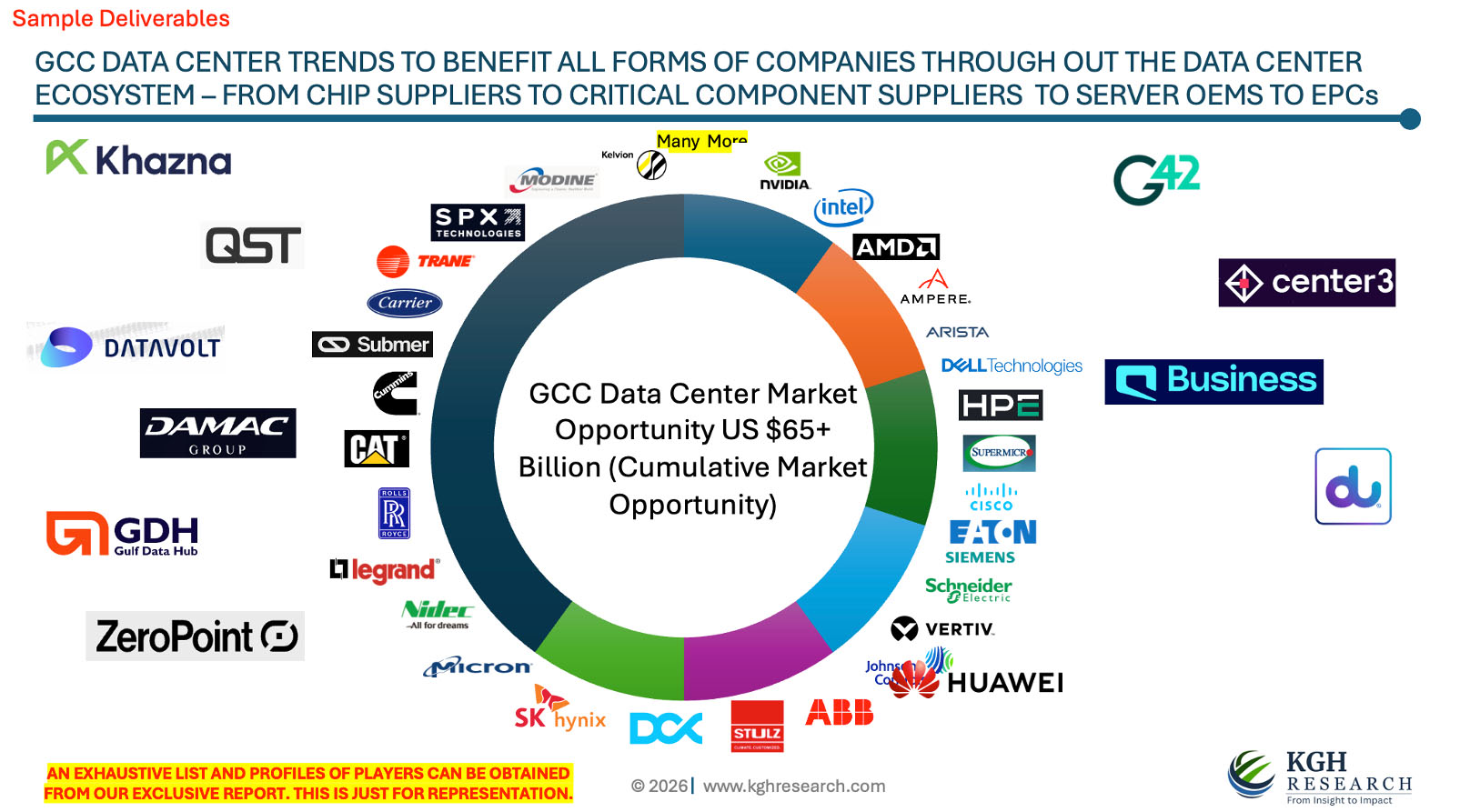

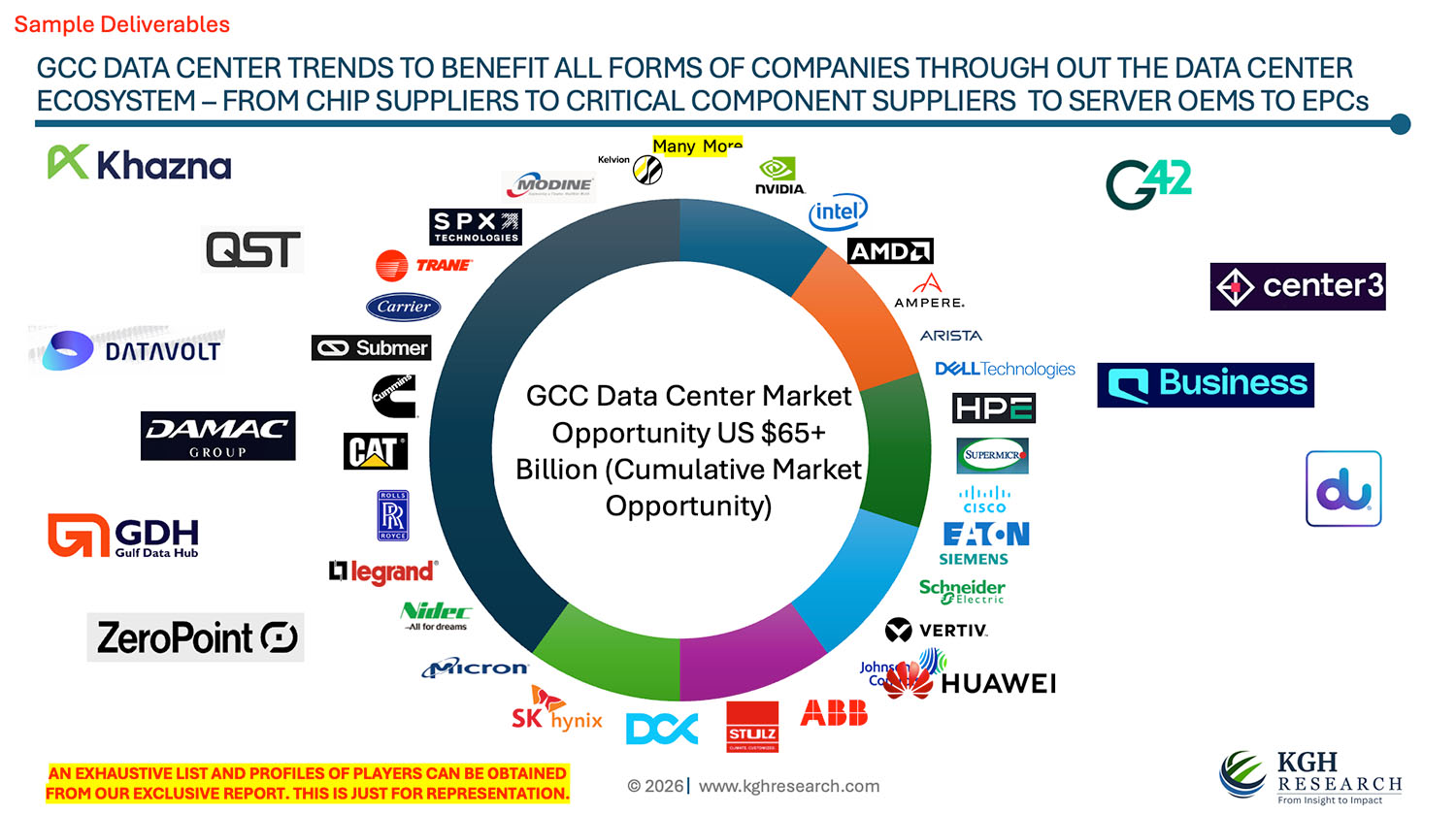

Companies Profiled (30+)

Nvidia, Intel, AMD, Huawei, Arista, Lenovo, Dell, HPE, SuperMicro, IBM, H3C, IEIT Systems, Vertiv, Schneider Electric, Rolls Royce, Johnson Control, , and Many More

License Options :

** Get free access to Next Version applicable only for 12 to 18 months from the date of purchase if we republish it