Marine Lubricant Market (2022 - 2032)

MARINE LUBRICANTS MARKET SIZE & SHARE BY OIL TYPE (SYNTHETIC OIL, MINERAL OIL, BIO-BASED OIL), BY PRODUCT (ENGINE OIL, COMPRESSOR OIL, HYDRAULIC FLUID, OTHERS), BY TIER (BASIC, INTERMEDIATE, ADVANCE), BY SHIP (CONTAINER SHIPS, BULK CARRIER, TANKERS, OTHER SHIPS) AND BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: C&M-3010-0204 | Number of Pages: 300+ | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: SEPTEMBER 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

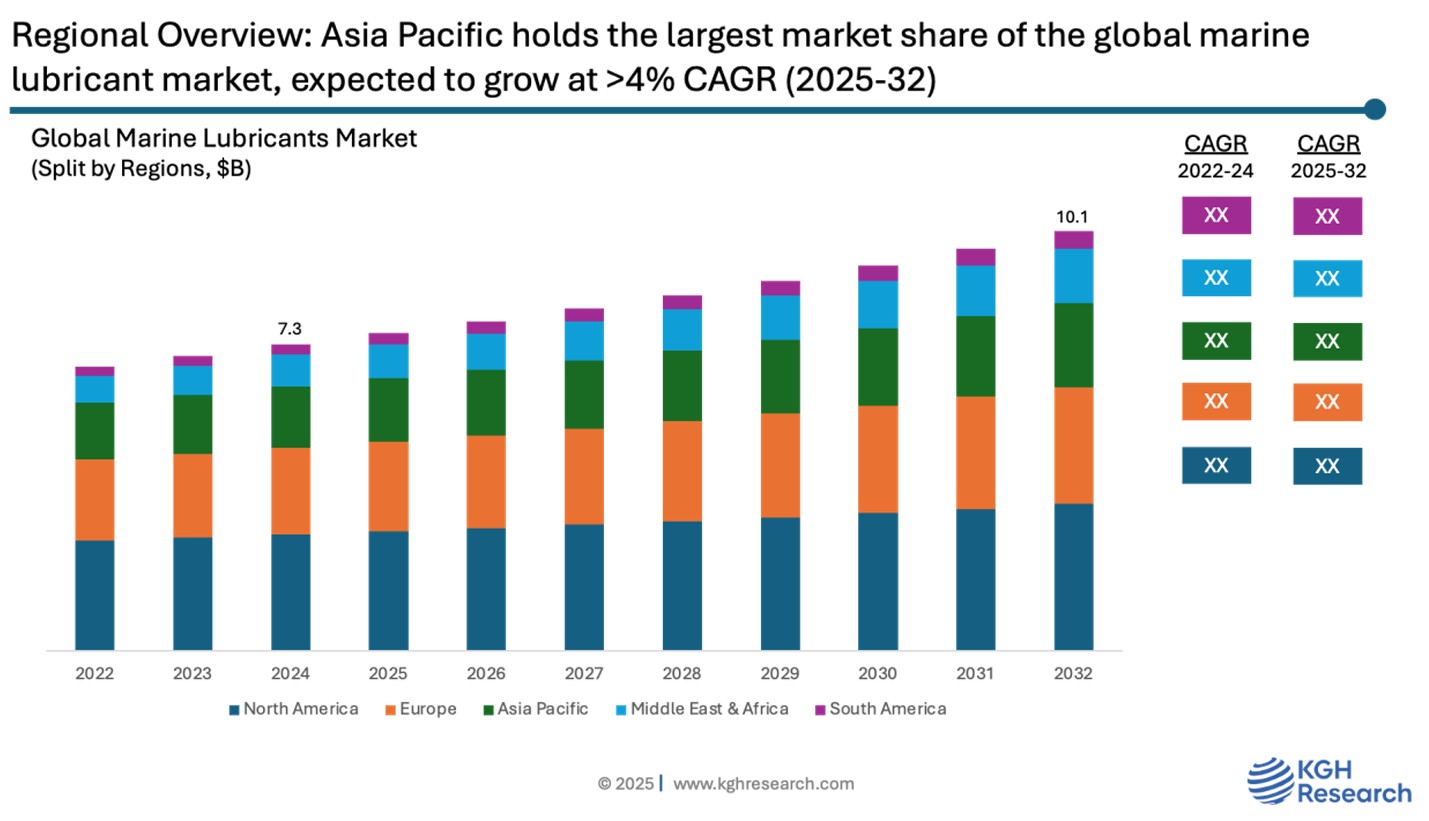

Market Overview: The global marine lubricants market was valued at approximately USD 7.3 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 4.1% from 2025 to 2032. The market is growing mainly because of the rise in global shipping activities and the push for cleaner, more fuel-efficient ships. As the volume of goods transported by sea increases, there’s a higher demand for reliable lubricants that help keep marine engines running smoothly and efficiently. At the same time, stricter environmental rules especially those from the International Maritime Organization (IMO) targeting sulfur emissions are encouraging ship operators to switch to advanced lubricants that not only reduce emissions but also protect engines

MARKET DYNAMIC

GROWTH DRIVERS:

- The continued growth in international maritime trade

- Growth of commercial shipping and naval fleets

- Technological advancements in marine engines

- Growth in offshore exploration and production activities

NEW GROWTH OPPORTUNITIES:

- Volatility in crude oil prices

- Transition to alternative fuels marine vessels, such as methanol powered vessels, hydrogen powered vessels

- Environmental risks & disposal issues

MARKET RESTRAINTS:

- High upfront costs & integration complexity

- Data privacy & cybersecurity concerns

- Lack of interoperability standards

- Skilled talent shortage

GROWTH HURDLES:

- Compliance with varied regional regulations

- High R&D costs for eco-friendly lubricants

- Supply chain disruptions

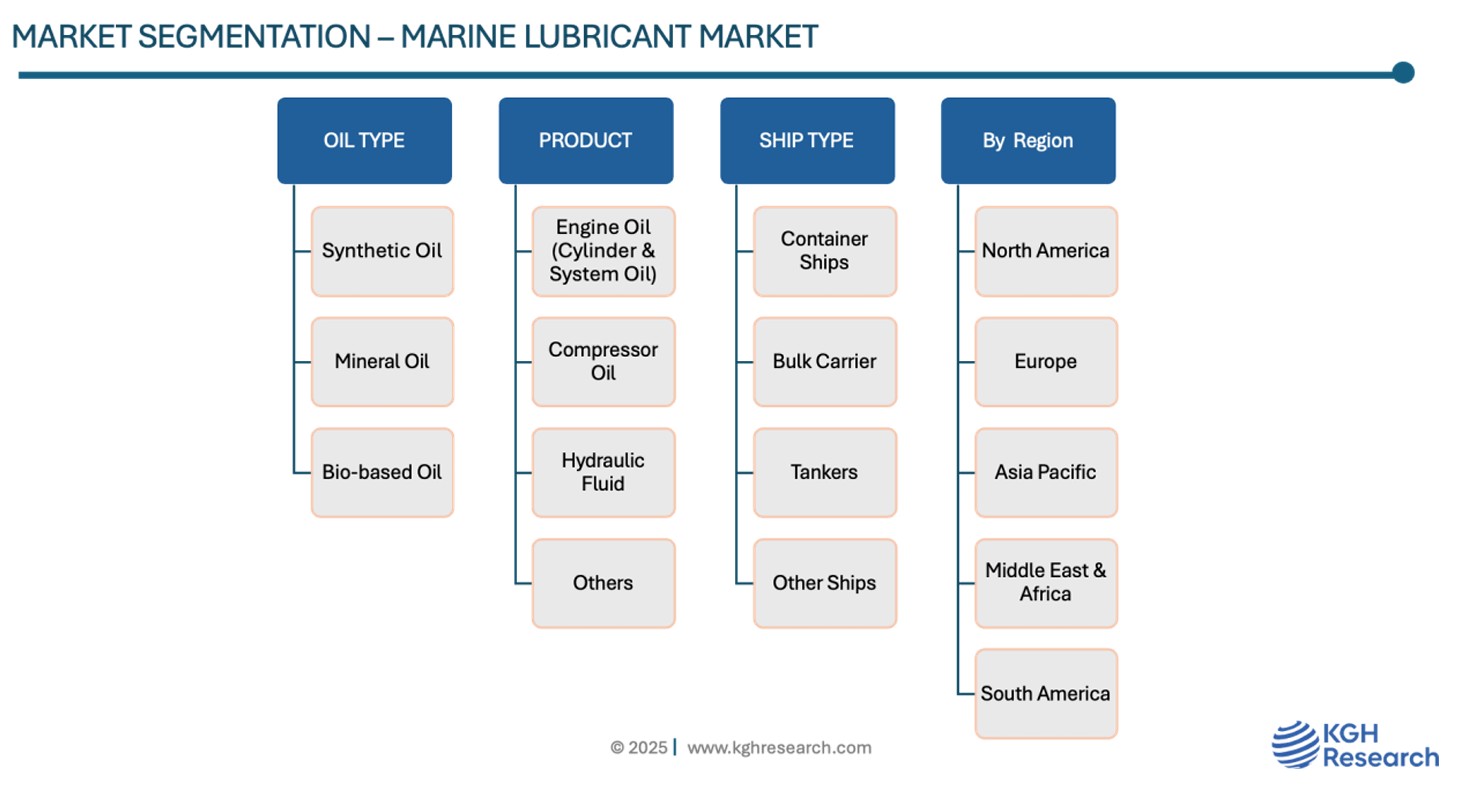

Oil Type: Market Insights

By oil type, the marine lubricants market is mainly categorized into the mineral oil, synthetic oil and bio-based oil. The mineral oil segment holds the largest share of the global marine lubricant market. This dominance is mainly due to its widespread availability, lower cost compared to synthetic and bio-based oils, and proven performance in a variety of marine applications. Mineral oil-based lubricants are commonly used across both older and newer vessel fleets for engine, gear, and system lubrication. While there is a growing interest in synthetic and environmentally acceptable lubricants (EALs), especially in environmentally regulated zones, mineral oils continue to be the preferred choice for many shipping operators due to their cost-effectiveness and compatibility with conventional marine engines.

Product: Market Insights

Engine oil represents the largest product segment in the marine lubricants market. This is mainly due to the vital role it plays in maintaining the performance of marine engines, particularly those in large commercial vessels and cargo ships that operate under intense pressure and harsh conditions. Engine oil is crucial for reducing friction, preventing wear, and ensuring smooth, long-term engine operation. As propulsion systems are central to vessel functionality, the consistent need for reliable and high-performance engine oils has made this category the most widely used in the marine lubricants market.

Ship Type: Market Insights

By ship type, bulk carriers are expected to lead the marine lubricants market in terms of value during the forecast period. This growth is driven by the large global fleet of bulk carriers and their consistent need for engine and machinery lubrication. These vessels play a critical role in transporting unpackaged bulk materials such as coal, grain, over long distances, which place substantial demands on their engines. Due to the heavy-duty nature of their operations, bulk carriers require frequent maintenance and high volumes of lubricants to ensure reliable performance, protect engine components, and meet environmental standards, making them the dominant consumer segment in the market.

Regional: Market Insights

Asia Pacific stands as the largest and most influential region in the global marine lubricants market, driven by a combination of economic scale, industrial infrastructure, and maritime dominance. The region hosts some of the busiest and most strategic shipping hubs in the world, including ports in China, Singapore, South Korea, and Japan, which handle a massive volume of international cargo traffic daily. This extensive maritime activity fuels a continuous demand for marine lubricants to support the operations of thousands of commercial vessels navigating these waters. Additionally, Asia Pacific is a global powerhouse in shipbuilding, with countries like China, Japan, and South Korea leading in the construction and maintenance of various types of vessels ranging from cargo ships to oil tankers. These ships, both during construction and throughout their operational lifespans, require a steady supply of high-performance lubricants to maintain engine efficiency, reduce wear and tear, and comply with safety and environmental standards. The region also benefits from a high concentration of commercial fleets operating on long-haul routes, which results in greater lubricant consumption due to the constant need for engine, gear, and auxiliary system lubrication. Furthermore, the rapid pace of industrialization, expanding international trade, and increasing dependence on marine transportation across emerging economies like India, Indonesia, and Vietnam are further propelling market growth. Regulatory developments, such as the implementation of IMO 2020 regulations to reduce sulfur emissions from ships, have also accelerated the demand for low-sulfur and environmentally acceptable lubricants across Asia Pacific ports, prompting a shift toward more advanced formulations. Supporting this demand is the presence of robust local production and distribution networks, as many global lubricant manufacturers have established regional facilities to efficiently serve the needs of Asia’s maritime sector. Collectively, these factors make Asia Pacific not only the largest but also one of the most dynamic and strategically important regions in the global marine lubricants market.

Competition: Marine Lubricants

The Marine Lubricants market is highly competitive, with key players focusing on innovation, product efficiency, and strategic partnerships to strengthen their market position. Major companies include Exxon Mobil Corporation, Shell plc, BP plc., TotalEnergies SE, Chevron Corporation, Lukoil, Petronas, Idemitsu Kosan Co., Ltd.. These players are investing in R&D to develop lubricants tailored for marine applications, driving ongoing competition and technological advancement in the market.

Exxon Mobil Corporation, Shell plc, BP plc, TotalEnergies SE, Chevron Corporation, Lukoil, Petronas, Idemitsu Kosan Co., Ltd., are among the leading companies active in the market.

Exxon Mobil Corporation is one of the world’s leading producers and suppliers of marine lubricants, with a strong global presence and a reputation for technological excellence. Headquartered in Irving, Texas, ExxonMobil operates under the well-known brand name ExxonMobil Marine in the maritime sector, offering a wide range of high-performance lubricants designed to meet the demanding needs of modern shipping fleets. The company provides products such as engine oils, gear oils, and greases for both main engines and auxiliary machinery, with popular marine lubricant brands including MobilGard and Mobil SHC. ExxonMobil places a strong emphasis on innovation and environmental responsibility, offering lubricants that help shipping companies comply with global regulations such as IMO 2020. Its advanced formulations are engineered to enhance fuel efficiency, extend equipment life, and reduce emissions. With a vast supply and distribution network that spans over 650 ports in more than 90 countries, ExxonMobil ensures reliable access to its products and services worldwide. The company also provides technical support and condition monitoring solutions to help ship operators optimize performance and reduce maintenance costs. Through continuous investment in R&D and a strong commitment to sustainability, ExxonMobil remains a key player shaping the future of the marine lubricants market.

BP plc, headquartered in London, UK, is a leading global energy company with extensive operations in oil and gas exploration, refining, marketing, trading, renewable energy, and notably, lubricants including marine applications. Its marine lubricant line is marketed under the renowned Castrol brand (formerly BP Marine), offering products like Castrol cyltech, MHP, HLX, and TLX Xtra, tailored for high-, medium-, and low-speed marine engines. BP acquired Castrol in 2000, consolidating its marine lubricant offerings and leveraging Castrol’s worldwide recognition to simplify its portfolio under one global brand, now available in over 820 ports across 82 countries. Its extensive global network ensures reliable supply and technical backing through BP Shipping and dedicated technical teams, reinforcing its marine fuels and lubricant presence.

MARINE LUNBRICANTS MARKET SNAPSHOT | |

Market size in 2024 | USD 7.3 Billion |

Market forecast in 2032 | USD 10.1 Billion |

Compound Annual Growth Rate (2025-2032) | 4.1% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Segments Covered | Oil Type, Product, Ship Type |

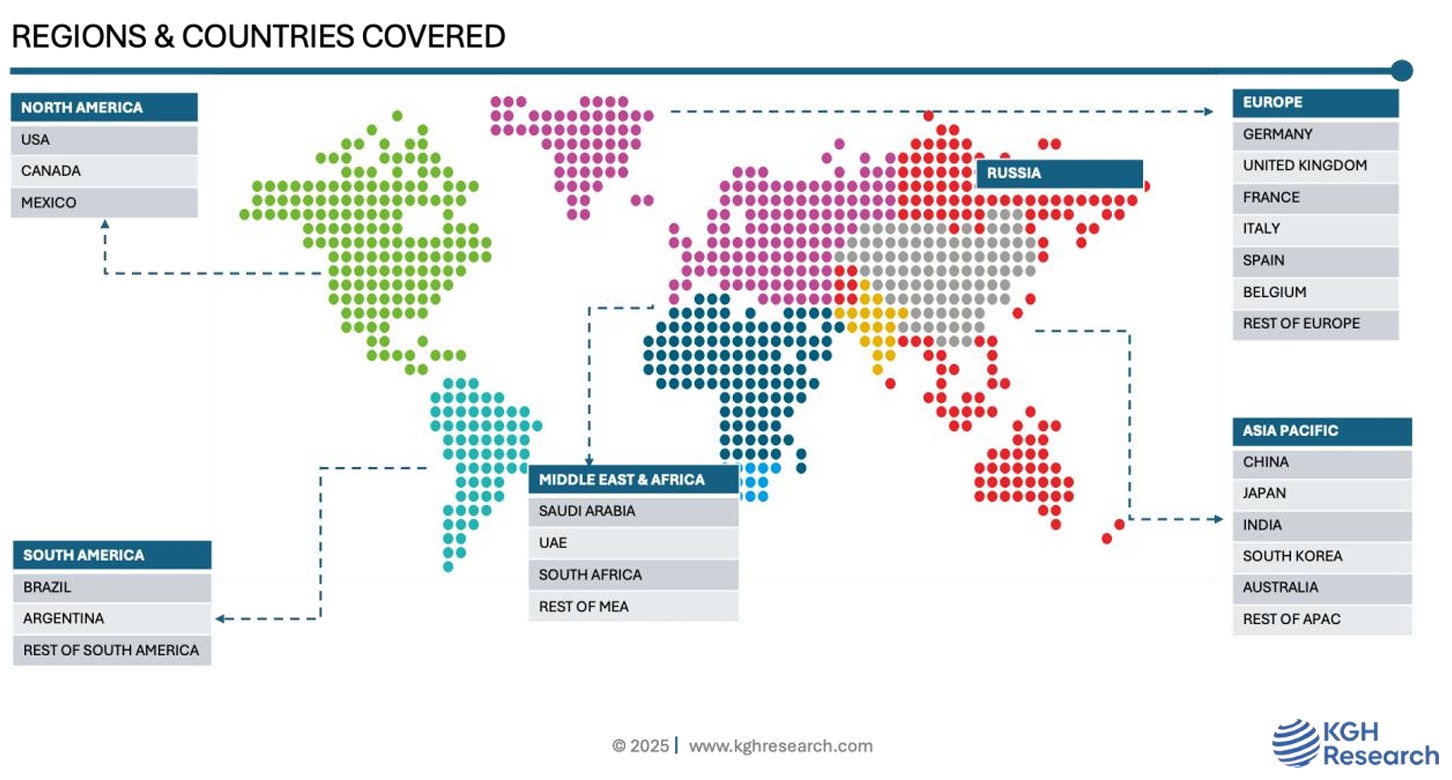

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, France, Belgium, Russia, France, Spain, China, Japan, India, South Korea, Australia, South Africa, UAE, Saudi Arabia, Brazil, Argentina |

Companies Profiled | EXXON MOBIL CORPORATION, SHELL PLC, TOTALENERGIES, CHINA PETROLEUM & CHEMICAL CORPORATION (SINOPEC), BP PLC, CHEVRON CORPORATION, LUKOIL, IDEMITSU KOSAN CO., LTD., ENEOS, GAZPROM NEFT, BEL-RAY CO. INC., QUAKER CHEMICAL CORP., ZELLER+GMELIN GMBH & CO. KG, BLASER SWISSLUBE AG, REPSOL, KLÜBER LUBRICATION, PENNZOIL, PHILLIPS 66, PETROCHINA CO. LTD., JX NIPPON OIL & ENERGY CORP., PETROFER CHEMIE, BUHMWOO CHEMICAL IND. CO. LTD., INNOSPEC, GULF OIL INTERNATIONAL, UNIMARINE INC., QUEPET LUBRICANTS LLC, AND OTHERS |