Switchgear Market (2022 - 2032)

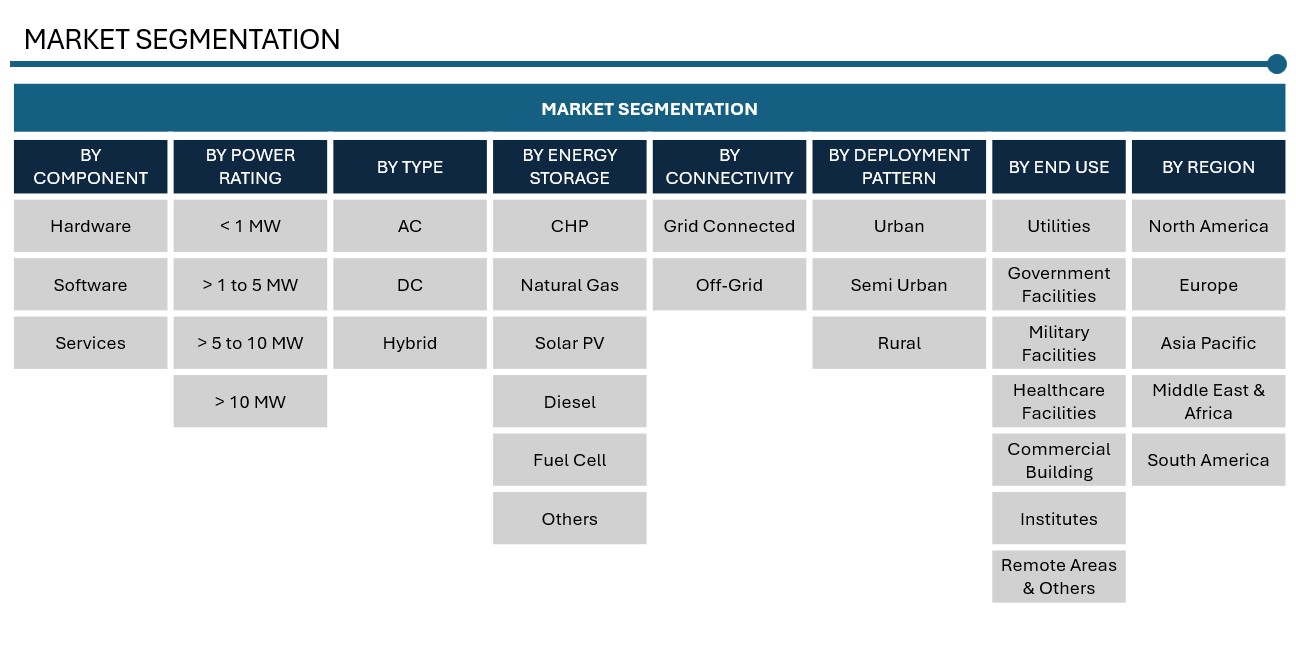

MICROGRID MARKET SIZE & SHARE BY OFFERING (HARDWARE, SOFTWARE, SERVICES), BY POWER RATING (1MW TO 5MW, >5 TO 10 MW, >10 MW), TYPE (AC, DC, HYBRID), BY ENERGY STORAGE (CHP, NATURAL GAS, SOLARPV, DIESEL, FUEL CELL, OTHERS), BY CONNECTIVITY (GRID, OFF-GRID), BY DEPLOYMENT (URBAN, SEMI URBAN, RURAL), BY END USE (UTILITIES, GOVERNMENT FACILITIES, MILITARY FACILITIES, HEALTHCARE FACILITIES, COMMERCIAL BUILDING, INSTITUTES, REMOTE AREAS) AND BY REGION & COUNTRY – FORECAST TO 2032

| Report Code: E&P4018-0203 | Number of Pages: 240 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: SEPTEMBER 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

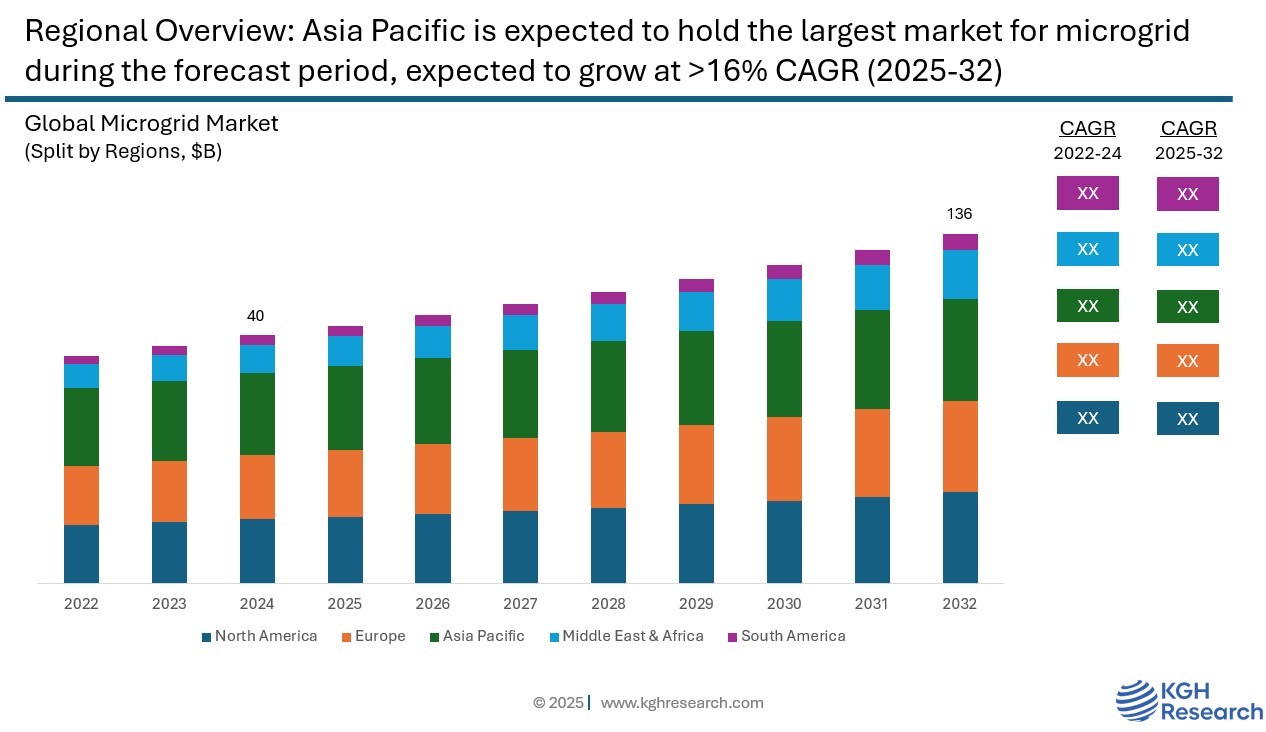

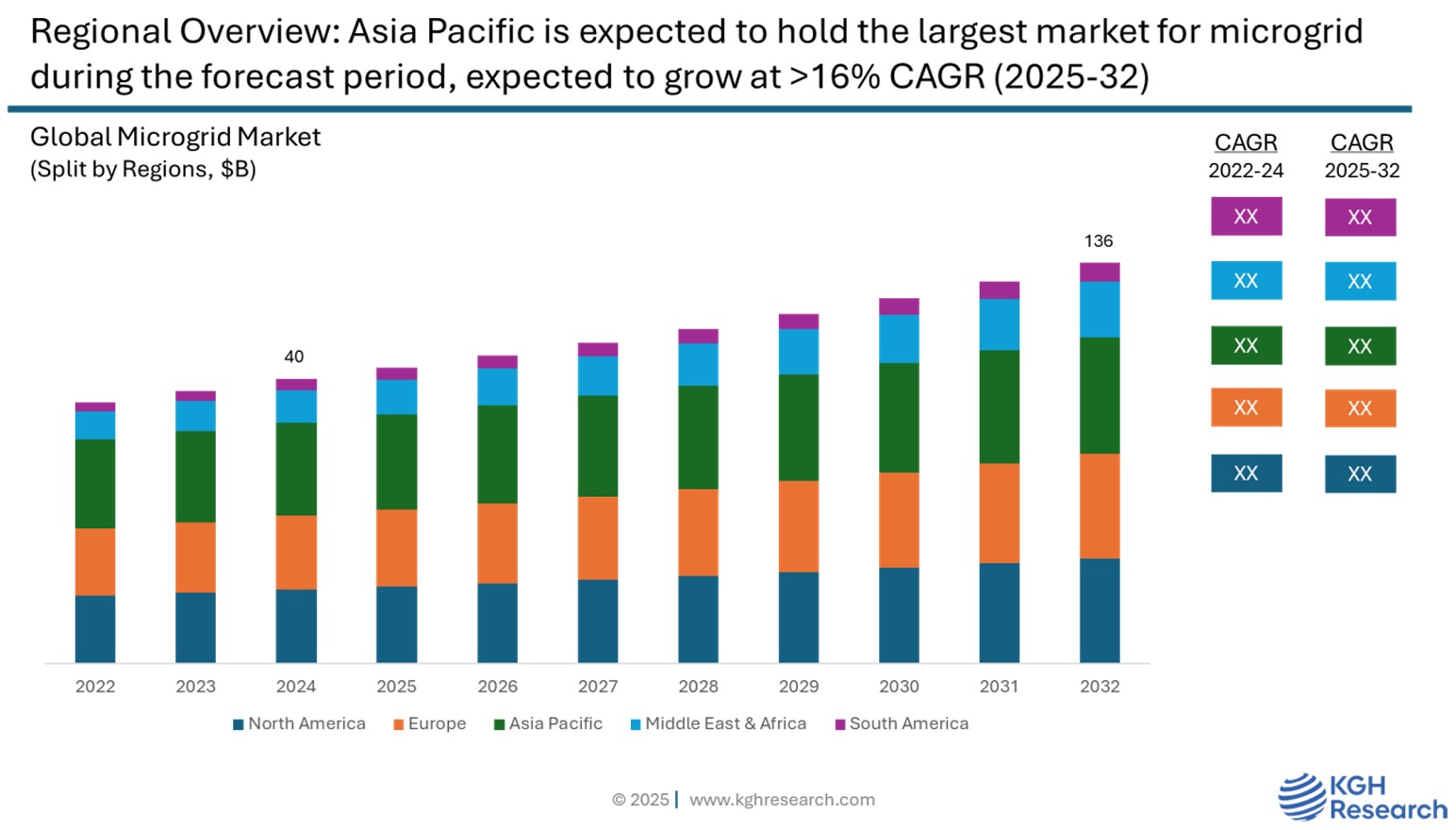

Market Overview: The global microgrid market was valued at approximately USD 40 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 16.7% from 2025 to 2032. The microgrid market is driven by increasing need for reliable, resilient, and decentralized energy systems. One of the primary drivers is the rising frequency of power outages and natural disasters, which has intensified the need for energy resilience, especially for critical infrastructure like hospitals, military bases, and data centres. Microgrids offer the ability to operate independently from the main grid, ensuring continuous power supply during emergencies. the global push toward clean energy and decarbonization is fuelling microgrid adoption, as they efficiently integrate renewable energy sources such as solar and wind, along with energy storage systems.

MARKET DYNAMIC

GROWTH DRIVERS:

- Growing demand for uninterrupted and reliable energy supply

- Microgrids enable efficient management and integration of renewable energy into the power network

- Electrification of remote and off-grid areas

- Supportive government policies, incentives, and regulatory mandates are accelerating microgrid adoption globally

- Advancement in communication & automation technologies

NEW GROWTH OPPORTUNITIES:

- Rapid urban growth and electrification in regions like Asia-Pacific, South America, Africa present significant growth potential

- Growing industrial and commercial sector adoption

- Demand for secure, reliable power for military and healthcare sector deployments

- Integration with EV Charging and smart cities

MARKET RESTRAINTS:

- High initial costs of setting up microgrids, especially with storage, remain significant

- Lack of standardized policies, especially in developing countries, complicates deployment

- Complex system design and integration

GROWTH HURDLES:

- Lack of skilled workforce and technical know-how

- Cybersecurity risks

- Grid compatibility and interoperability issues

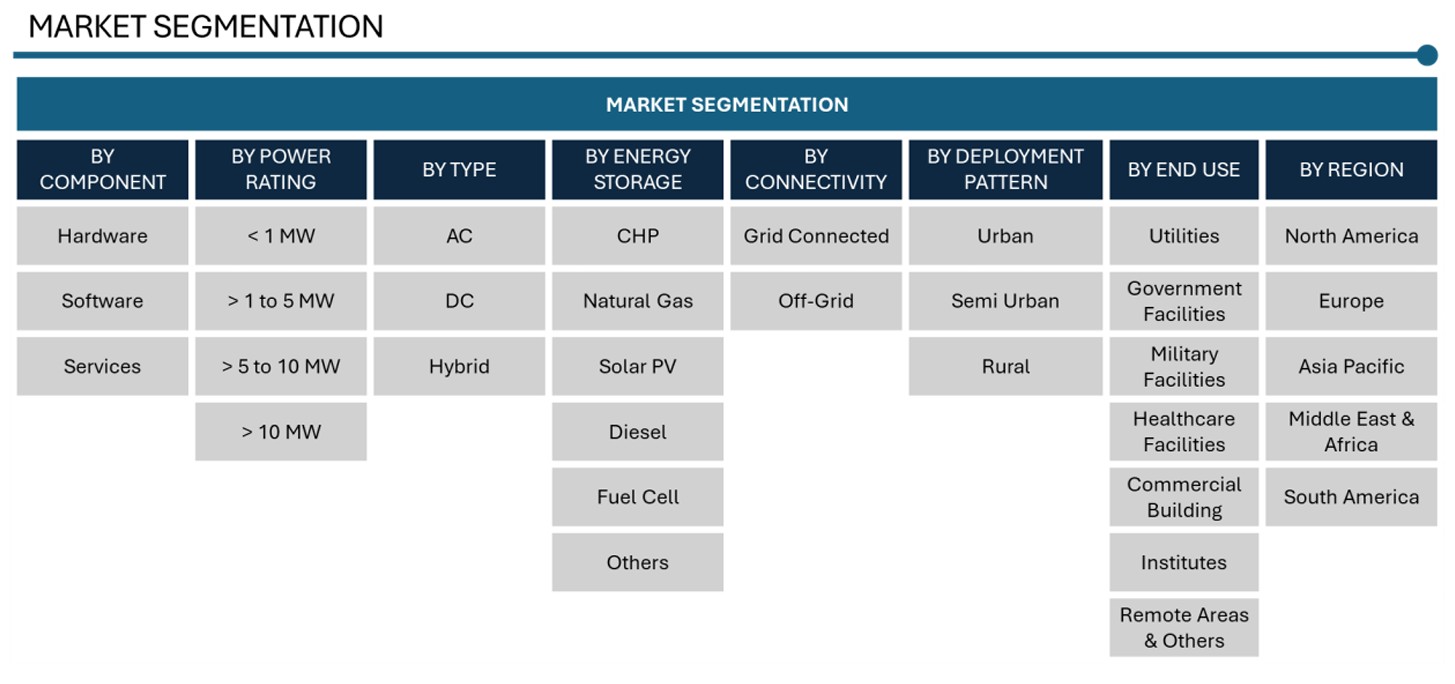

Component: Market Insights

In the global microgrid market, the component segment is categorized into hardware, software, and services. Among these, the hardware segment holds the largest market share, primarily due to the significant capital investment required for essential physical components such as power generation units (solar panels, wind turbines, diesel generators), energy storage systems (batteries), control systems, and other power distribution infrastructures.

Power Rating: Market Insights

The microgrid market, when segmented by power rating, is generally categorized into four main segments: less than 1 MW, 1 to 5 MW, 5 to 10 MW, and more than 10 MW. Microgrids with a power rating of less than 1 MW are typically used in remote aeras, small communities, or isolated facilities where energy demand is minimal. The 1 to 5 MW segment is widely adopted in commercial buildings, educational institutions, and small industrial facilities due to its balance of capacity and affordability. Microgrids in the 5 to 10 MW range are suited for larger industrial operations or clusters of buildings requiring higher loads. Systems above 10 MW are designed for large-scale applications such as utility-scale projects, military bases, and critical infrastructure with high energy demand. Each power rating category addresses different operational needs, making this segmentation crucial for deployment planning and investment decisions in the microgrid market.

Type: Market Insights

By type, the global microgrid market is segmented into AC, DC, and hybrid types, each catering to specific application requirements and technical setups. AC microgrids dominate the market, primarily because they align well with existing grid infrastructure and the widespread use of AC-powered devices. They are commonly deployed in both grid-connected and off-grid scenarios, especially where seamless integration with conventional utility systems is needed. DC microgrids, on the other hand, are gaining popularity in specialized applications such as data centres, telecommunication infrastructure, EV charging stations, and systems that heavily rely on DC-based renewable sources like solar PV. These microgrids offer greater energy efficiency and streamlined control by avoiding frequent AC-DC conversions. Hybrid microgrids, which integrate both AC and DC networks, are emerging as a versatile and effective solution, leveraging the strengths of both systems. They are particularly valuable in complex settings that involve diverse loads and multiple energy sources. With advancements in renewable energy technologies, storage systems, and digital control solutions, hybrid microgrids are expected to experience significant growth in the coming years.

Energy Storage: Market Insights

By energy storage, the global microgrid market is segmented into CHP, natural gas, diesel, solar PV, fuel cell and others. The Combined Heat & Power segment is expected to dominate the global market during the forecast period. This dominance is largely driven by a growing shift away from traditional Separate Heat & Power systems toward more efficient energy generation using a single fuel source. Looking ahead, the fuel cell segment is projected to witness significant growth, supported by its ability to operate at high temperatures and deliver energy with minimal electrolytic losses factors that are expected to expand its adoption in various applications.

Connectivity: Market Insights

Grid-connected microgrids are expected to dominate the market during the forecast period. This dominance is primarily driven by their ability to seamlessly integrate with the main utility grid while offering enhanced energy efficiency, stability, and cost savings. Grid-connected systems are widely adopted in urban and industrial areas where reliable power supply and load optimization are critical. They support the integration of renewable energy sources, enable energy trading, and reduce peak demand charges, making them an attractive option for utilities, commercial establishments, and campuses. As governments and utilities continue to modernize grid infrastructure, the adoption of grid-connected microgrids is projected to grow significantly.

End Use: Market Insights

By end use, commercial buildings are expected to hold the largest share of the microgrid market during the forecast period. This growth is driven by the increasing need for reliable and uninterrupted power supply in sectors such as offices, shopping malls, hospitals, data centers, and educational institutions. These facilities often have high energy demands and are increasingly adopting microgrids to improve energy efficiency, reduce operational costs, and meet sustainability goals. The ability of microgrids to ensure energy resilience during grid outages and their compatibility with renewable energy integration make them an ideal solution for commercial applications. As awareness of energy independence and carbon footprint reduction grows, the adoption of microgrids in commercial buildings is projected to rise significantly.

Regional: Market Insights

Asia Pacific is expected to hold the largest share of the global microgrid market during the forecast period, driven by rapid urbanization, industrial growth, and increasing demand for reliable and sustainable energy solutions across the region. Countries like China, India, Japan, South Korea, and several Southeast Asian nations are investing heavily in modernizing their power infrastructure, integrating renewable energy, and enhancing energy access in remote and underserved areas. Government initiatives promoting rural electrification, renewable deployment, and clean energy transitions are further fueling the adoption of microgrid systems. Additionally, the presence of a large population, coupled with rising energy consumption and frequent grid stability issues in certain areas, is creating a favorable environment for microgrid development. Technological advancements, declining costs of solar PV and battery storage, and the increasing involvement of both public and private players are also contributing to the region’s leadership in the microgrid market. As a result, Asia Pacific is poised to remain a key growth engine for the global microgrid industry during the forecast period.

China is emerging as a global leader in the microgrid market, driven by its aggressive push toward clean energy, energy storage, and grid modernization. The country is investing heavily in integrating renewable energy sources such as solar and wind with advanced storage systems, including lithium-ion and grid-forming sodium-ion batteries. These technologies are increasingly being deployed in remote areas, industrial parks, and urban infrastructure like EV charging stations and smart buildings. China’s vast deployment of energy storage—over 42 GW in 2024 alone—enhances microgrid efficiency and resilience. However, challenges such as grid curtailment and uneven utilization of battery assets persist due to infrastructure lag. To address this, the government has committed over USD 800 billion toward grid upgrades over six years. With continued policy support, rural electrification efforts, and innovations in smart grid technology, China is poised to remain a dominant force in the global microgrid landscape.

Japan is also witnessing robust growth in its microgrid market, driven by a strong focus on energy resilience, sustainability, and smart city development. Japan’s vulnerability to natural disasters like earthquakes and typhoons has made it clear how essential microgrids are for maintaining power during emergencies. Projects such as Higashi-Matsushima and Fujisawa Smart Town highlight Japan’s forward-thinking approach to building resilient energy systems. The country is quickly adopting advanced energy storage technologies—like lithium-ion and redox-flow batteries to make its microgrids more stable and better equipped to handle renewable energy. Backed by significant public and private investment, including large-scale battery networks from Sumitomo and virtual power plant initiatives by Tesla, Japan’s microgrid market is expanding rapidly. Although high setup costs and integration in densely populated areas pose challenges, the government is tackling these through supportive policies and innovation. What began as a strategy for disaster response is now evolving into a broader shift toward smart, sustainable energy systems across the country.

Competition: Microgrid

The Microgrid market is highly competitive, with key players focusing on innovation, product efficiency, and strategic partnerships to strengthen their market position. Major companies include General Electric Company, Schneider Electric, Siemens, ABB, and Eaton. These players are investing in R&D to develop products & services tailored for applications in utility, industrial, commercial, residential sectors, driving ongoing competition and technological advancement in the market.

General Electric Company, Schneider Electric, Siemens, ABB, and Eaton are among the leading companies active in the market.

Schneider Electric is a leading global player in the microgrid market, known for its comprehensive and integrated solutions that span hardware, software, and services. The company has been consistently ranked among the top microgrid integrators globally, thanks to its innovative EcoStruxure platform, which includes modular offerings like EcoStruxure Microgrid Flex, Microgrid Advisor, and Energy Control Center. These systems enable real-time optimization, seamless integration of distributed energy resources, and enhanced energy resilience. Schneider Electric has deployed over 300 microgrid projects across North America alone, with applications ranging from commercial and industrial sites to military bases and smart cities. Notable projects include advanced hybrid systems combining solar, battery storage, fuel cells, and microturbines, all controlled via their smart energy management platforms. The company is also at the forefront of Energy-as-a-Service (EaaS) through initiatives like AlphaStruxure and GreenStruxure, allowing clients to adopt microgrid solutions without upfront capital investment. With a strong focus on decarbonization, energy efficiency, and digital innovation, Schneider Electric continues to drive the global microgrid market forward.

General Electric (GE) is another key player in the global microgrid market, leveraging its deep expertise in power generation, grid infrastructure, and digital solutions. Through its energy business divisions—primarily GE Vernova and GE Grid Solutions—GE offers end-to-end microgrid solutions that integrate renewable energy, conventional power sources, and energy storage systems. Its advanced grid automation technologies, such as intelligent control systems, protection relays, and digital substations, enable real-time monitoring, optimization, and seamless transition between grid-connected and islanded modes. GE has implemented numerous microgrid projects across industrial facilities, military installations, and remote communities, particularly in regions with unreliable grid infrastructure. The company also utilizes predictive analytics and AI-driven platforms to enhance grid stability, manage distributed energy resources, and improve energy resilience. With a strong global presence and focus on innovation, GE continues to support the modernization of power systems through smart, scalable microgrid solutions tailored to evolving energy needs and sustainability goals.

MICROGRID MARKET PURVIEW | |

Market size in 2024 | USD 40 Billion |

Market forecast in 2032 | USD 136 Billion |

Compound Annual Growth Rate (2025-2032) | 16.7% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Market Drivers | Growing demand for uninterrupted and reliable energy supply Microgrids enable efficient management and integration of renewable energy into the power network Electrification of remote and off-grid areas Supportive government policies, incentives, and regulatory mandates are accelerating microgrid adoption globally Advancement in communication & automation technologies |

Segments Covered | Component, Type, Connectivity, Power Rating, Energy Source, Deployment Pattern, End Use |

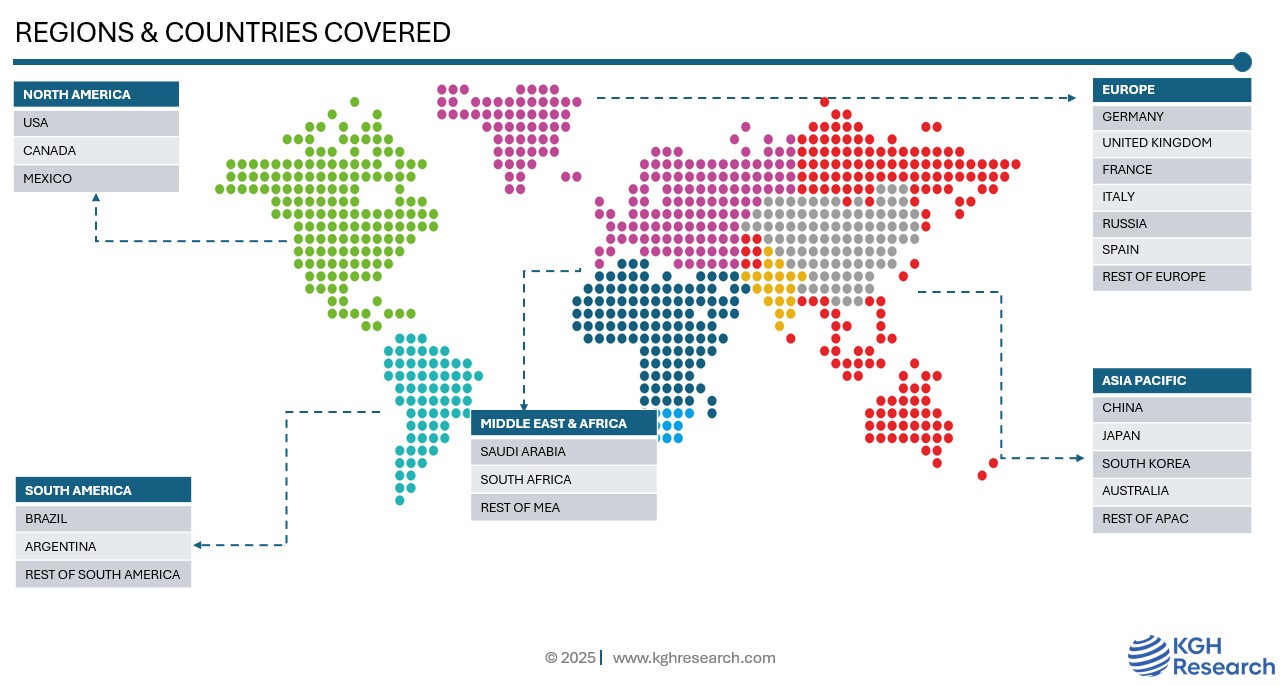

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, UK, Germany, Italy, France, China, Japan, South Korea, Australia, UAE, South Africa, Saudi Arabia, Brazil, Argentina |

Companies Profiled | SCHNIDER ELECTRIC, SIEMENS, ABB, GENERAL ELECTRIC COMPANY, HITACHI ENERGY LTD, EATON, POWER ANALYTICS GLOBAL CORPORATION, S&C ELECTRIC, HOMER ENERGY, HONEYWELL, CATERPILLAR, TESLA ENERGY, SPIRAE LLC, GENERAL MICROGRIDS, PARETO ENERGY, POLARIS INC., HEILA TECHNOLOGIES, AMERESCO, GO ELECTRIC INC., FERROAMP, CANOPY POWER, EMERSON ELECTRIC CO., ANBARIC DEVELOPMENT PARTNERS, LLC., EXELON CORPORATION |