Recycled Plastics (2022 - 2032)

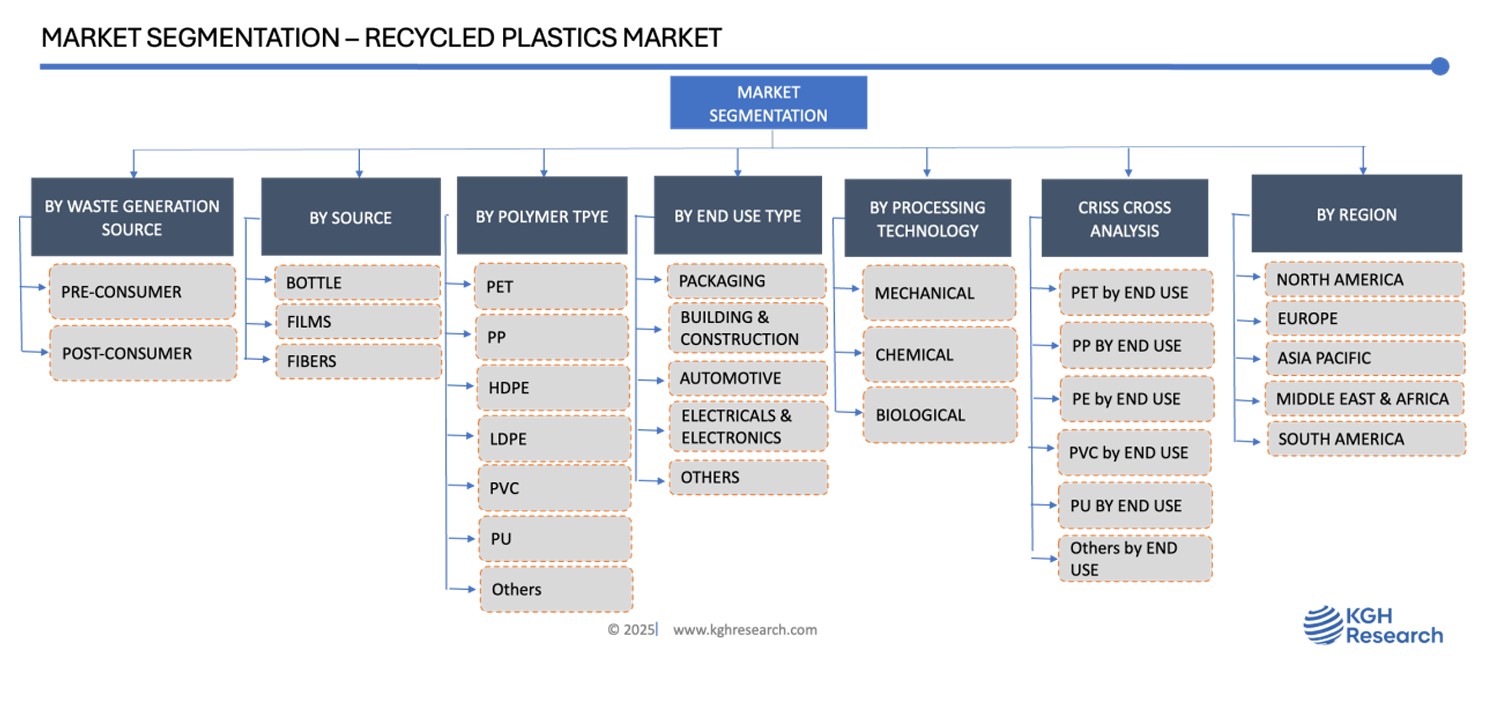

RECYCLED PLASTICS MARKET SIZE & SHARE BY WASTE GENERATION (PRE CONSUMER AND POST CONSUMER), BY SOURCE TYPE (BOTTLE, FIBERS, AND FILMS), BY POLYMER TYPE (PET, PP, LDPE, HDPE, PVC, PU, AND OTHERS), BY END USE (PACKGING, BUILDING & CONSTRUCTION, AUTOMOTIVE, ELECTRICAL & ELECTRONICS, AND OTHERS), BY PROCESSING TECHNOLOGIES (MECHANICAL, CHEMICAL, AND BIOLOGICAL RECYCLING), CRISS-CROSS ANALYSIS (END USE BY POLYMER TYPE), AND BY REGION & COUNTRY–FORECAST TO 2032

| Report Code: C&M8007-0801 | Number of Pages: 400 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: JULY 2025 |

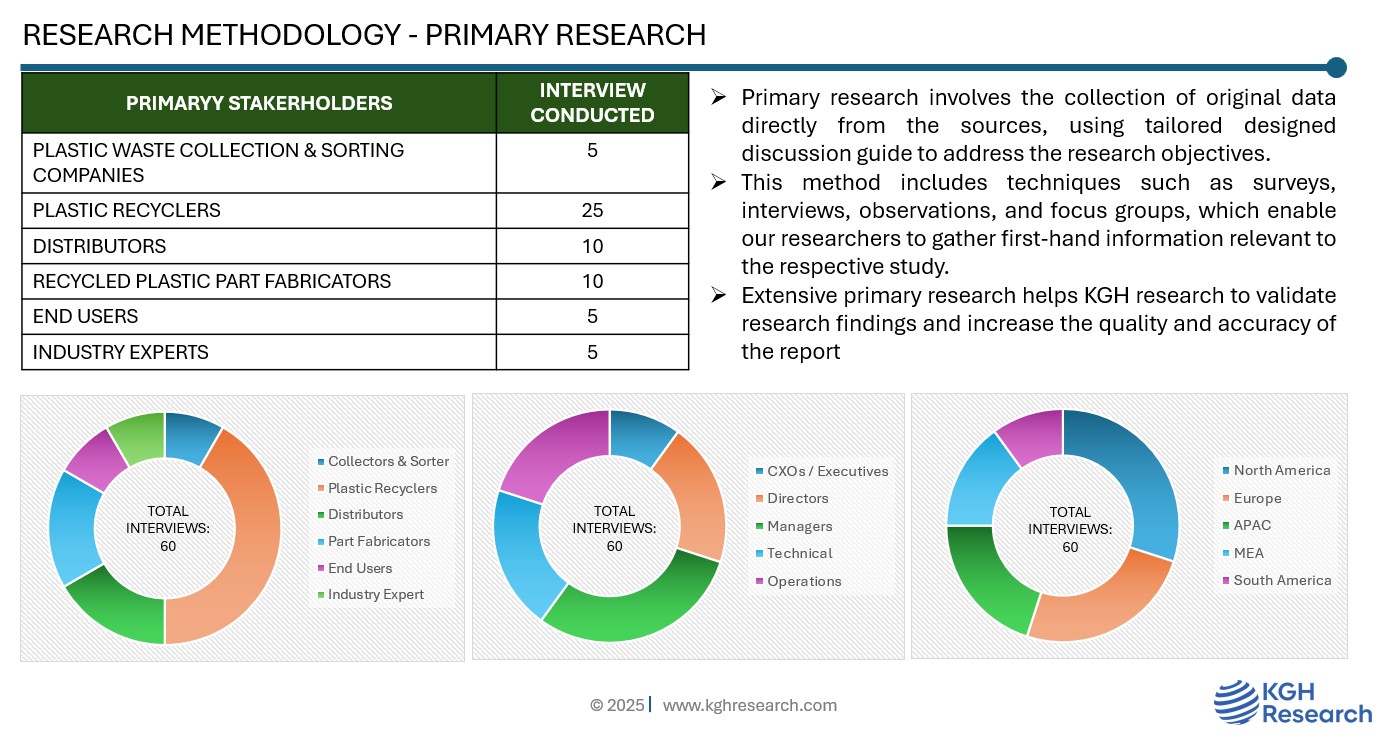

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

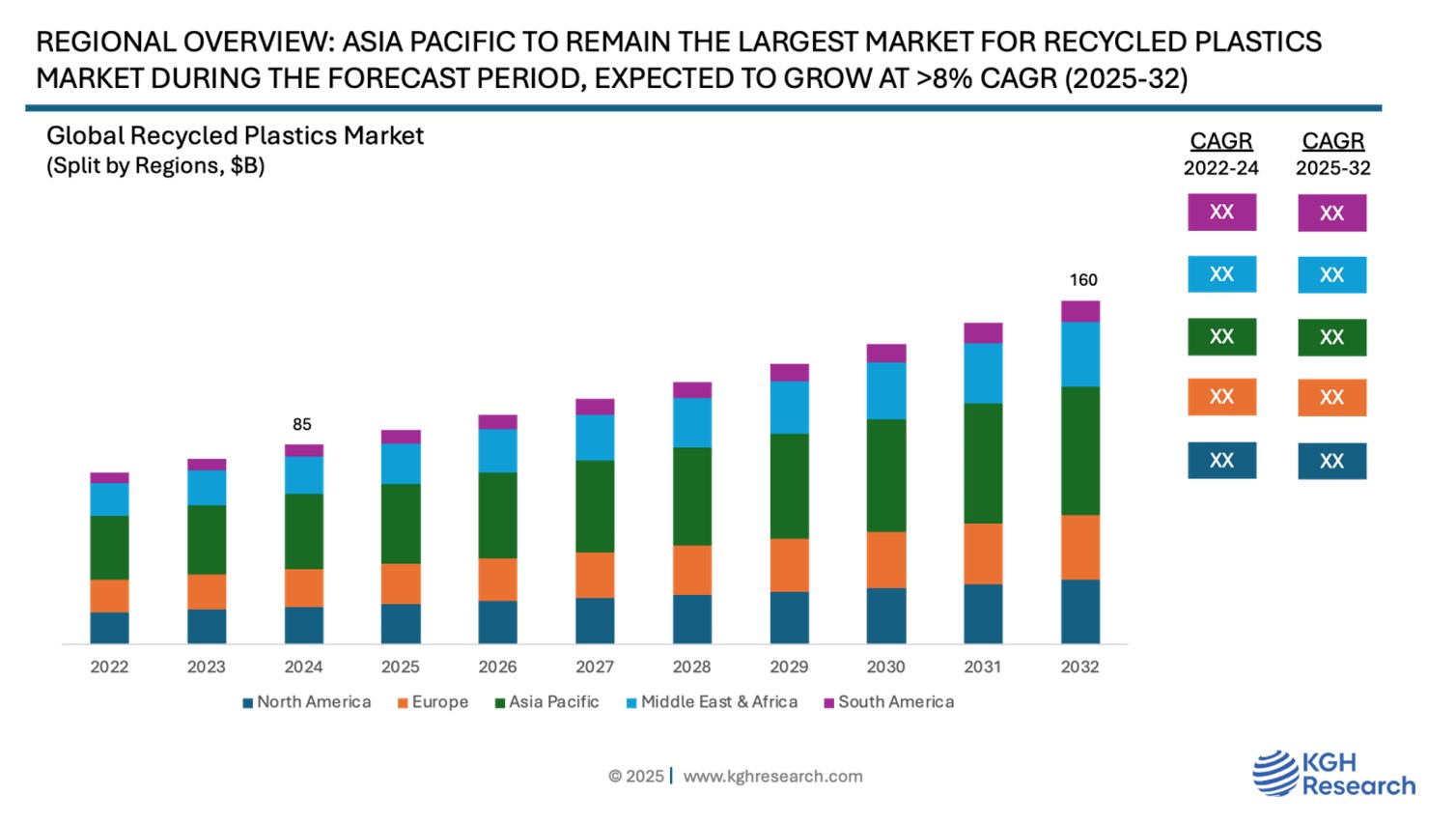

Market Overview: The global recycled plastics market was estimated at US $85 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of more than 8% from 2025 to 2032 to reach US $160 billion by 2032. The global recycled plastics market has experienced substantial growth over the last decade, driven by increasing awareness around environmental sustainability and escalating concerns regarding plastic pollution. Regulatory mandates imposed by various governments to curtail single-use plastics and promote recycling initiatives are among the primary forces encouraging the widespread adoption of recycled plastic materials. Industries such as packaging, automotive, consumer goods, and construction are increasingly integrating recycled plastics into their manufacturing processes and final parts to meet sustainability targets while reducing dependence on virgin polymers.

MARKET DYNAMIC

GROWTH DRIVERS:

- Stricter government mandates and global consumer preference for sustainable products are compelling brands to incorporate recycled plastics content into their product lines. Packaging giants and consumer goods companies, like Unilever and Coca-Cola, are setting ambitious recycled plastic usage targets, creating strong demand.

- Driver 2

- Driver 3

- Driver 4

NEW GROWTH OPPORTUNITIES:

- Innovations, technological advancements and improvements in sorting, cleaning, and pelletizing are improving the quality, usability and scalability of recycled

- Increasing adoption of recycled content in industries, such as automotive, consumer electronics, and others

- Opportunity 3

- Opportunity 4

MARKET RESTRAINTS:

- Key challenge lies in the inconsistent quality and supply of recycled plastics feedstock. Contamination during the collection phase often leads to downgraded plastic quality, which is unsuitable for high-performance or food-contact applications.

GROWTH HURDLES:

- High costs associated with sorting and decontamination remain high, limiting competitiveness with virgin plastics in regions with lower landfill tipping fees or energy recovery options.

- Trade tensions, tariffs, and geopolitical instability may impact global supply chains, demand, production costs, and profitability.

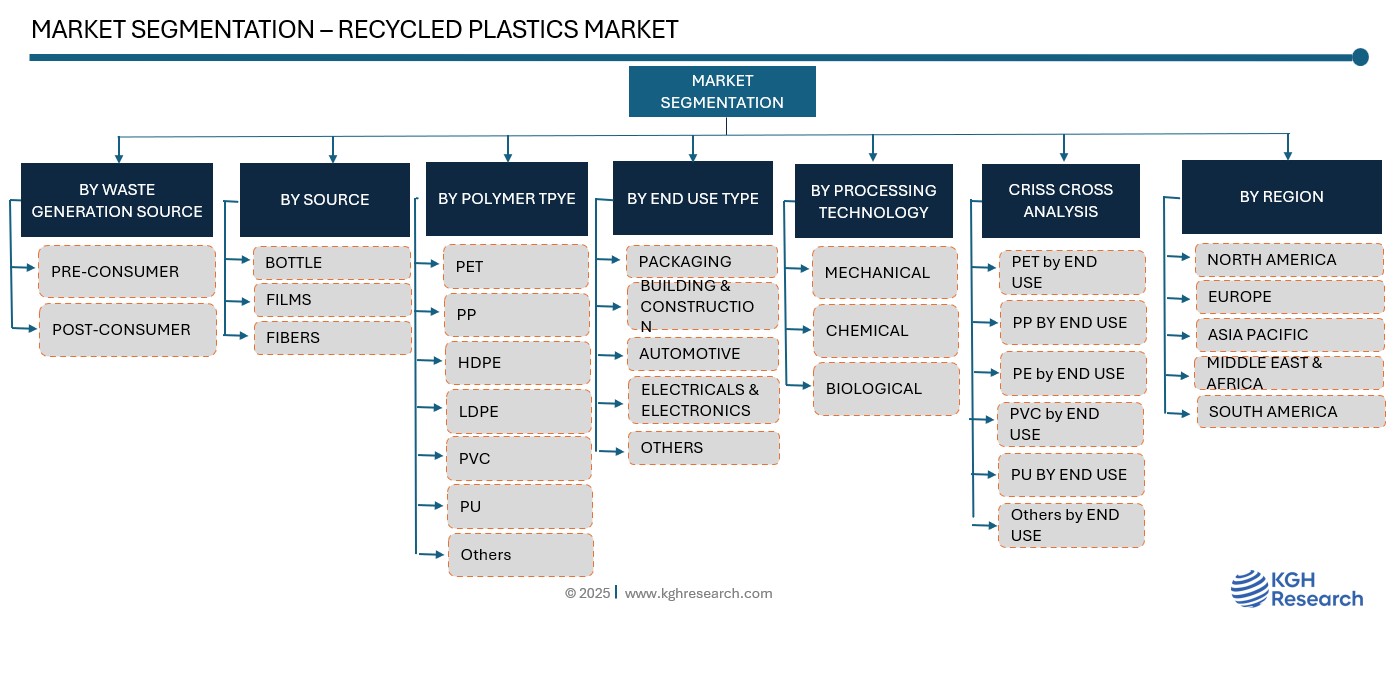

Waste Generation Source: Market Insights

The inner rotor segment dominated the market with a share of more than 60% in 2024. The dominance is due to its excellent performance and wide usage in a variety of industries. Inner rotor motors are perfect for applications that need quick acceleration and deceleration, like robotics, automation, and CNC machines. Their compact and sturdy design fits well in tight spaces. Plus, their lower rotor inertia allows for a fast response, which is essential for precise control. Inner rotor BLDC motors are also widely used in industrial automation, automotive systems (such as fans, pumps, and power steering), HVAC, and consumer electronics. Their popularity has led to economies of scale, which lower production costs and strengthen their leading position in the market.

Source Type: Market Insights

Plastic bottles and rigid containers form the most prominent source segment in the market. These sources are mainly PET and HDPE bottles—offer cleaner, high-quality streams that are relatively easier to process through mechanical recycling. Their widespread collection through curb side programs makes them a reliable feedstock for industries producing recycled food-grade packaging, textiles, and household goods. This segment also benefits from high recovery rates and targeted collection schemes implemented by local governments and corporate reverse logistics networks.

In contrast, films and fibres—such as LDPE films, plastic wraps, and synthetic textiles—pose significant recycling challenges due to their lightweight nature and high contamination levels. These materials often require specialized machinery and pre-treatment processes to make recycling feasible. However, advances in chemical recycling and innovations in plastic-to-fuel and plastic-to-monomer technologies are gradually unlocking new end-use opportunities for these complex waste streams.

Polymer Type: Market Insights

In terms of polymer type, PET and HDPE dominate the recycled plastics landscape, accounting for over 60% of the global recycled plastic volume. PET is favoured for beverage bottles and textile fibres, while HDPE finds applications in containers, piping, and construction materials. Polypropylene (PP) and low-density polyethylene (LDPE) are emerging segments gaining traction, particularly in automotive and packaging uses. However, PVC and polystyrene remain under-represented in recycling due to toxic additives and limited recycling infrastructure.

End-Use: Market Insights

Packaging is the largest end-use sector for recycled plastics, driven by stringent packaging directives and demand for sustainable alternatives. Food-grade rPET, for example, is widely used in beverage containers, trays, and films. Beyond consumer packaging, industrial and flexible packaging also represent growth areas, particularly in logistics and agriculture. Major FMCG players are mandating minimum recycled content, reinforcing demand across supply chains.

The automotive and construction industries are fast-growing consumers of recycled plastics due to their focus on lightweighting and green building certifications. Recycled PP, PE, and composites are increasingly used in bumpers, dashboards, cable insulation, pipes, and roofing applications within the automotive industry. Electronics manufacturers are also integrating recycled plastics into components like casings, while textiles utilize rPET fibers in garments, upholstery, and carpets. This diversification of demand is instrumental in supporting a robust and resilient market.

Processing Technology: Market Insights

Mechanical recycling remains the most prevalent technology, involving steps such as collection, sorting, shredding, washing, and pelletizing. Its cost-effectiveness and lower carbon footprint make it suitable for high-volume, lower-contamination waste streams like PET bottles. However, mechanical recycling has limitations in maintaining polymer quality after repeated cycles, particularly in food-grade applications.

Chemical recycling is gaining prominence as a complementary method capable of depolymerizing plastics into monomers or fuels. It enables closed-loop recycling of hard-to-recycle plastics like multi-layer packaging, PP, and polystyrene. Leading companies are investing in pyrolysis, gasification, and solvent-based depolymerization processes to overcome mechanical recycling’s limitations. While capital-intensive and still at pilot scale in many regions, chemical recycling holds potential to significantly expand the spectrum of recyclable plastics.

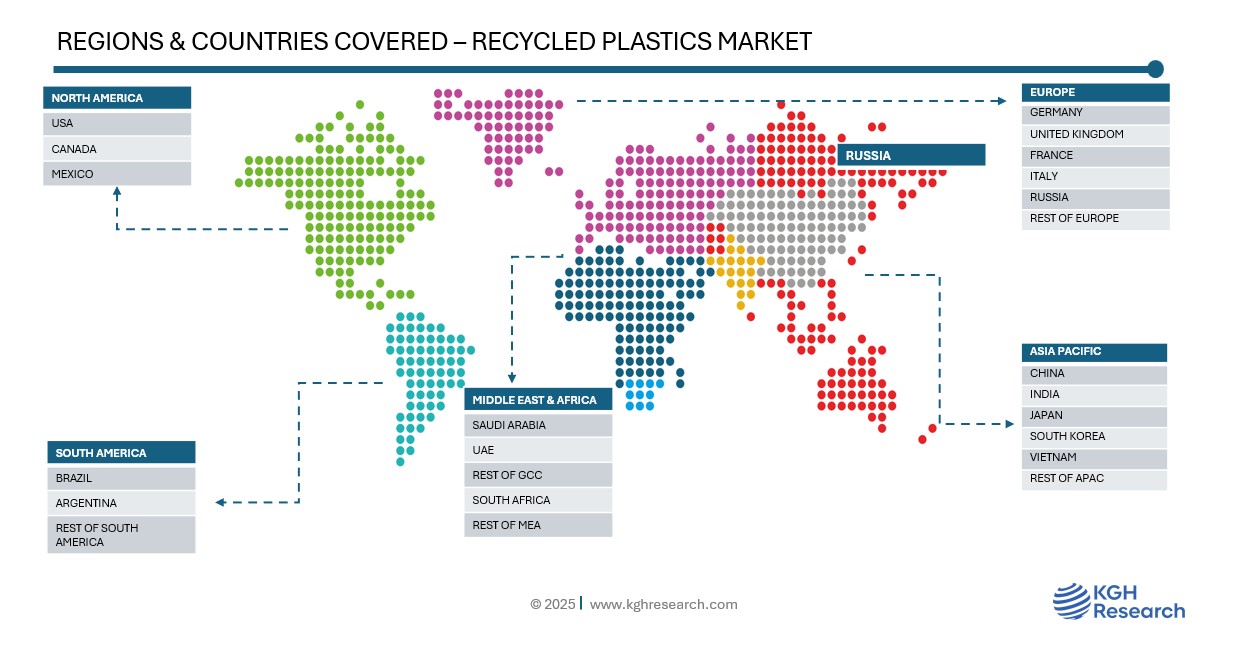

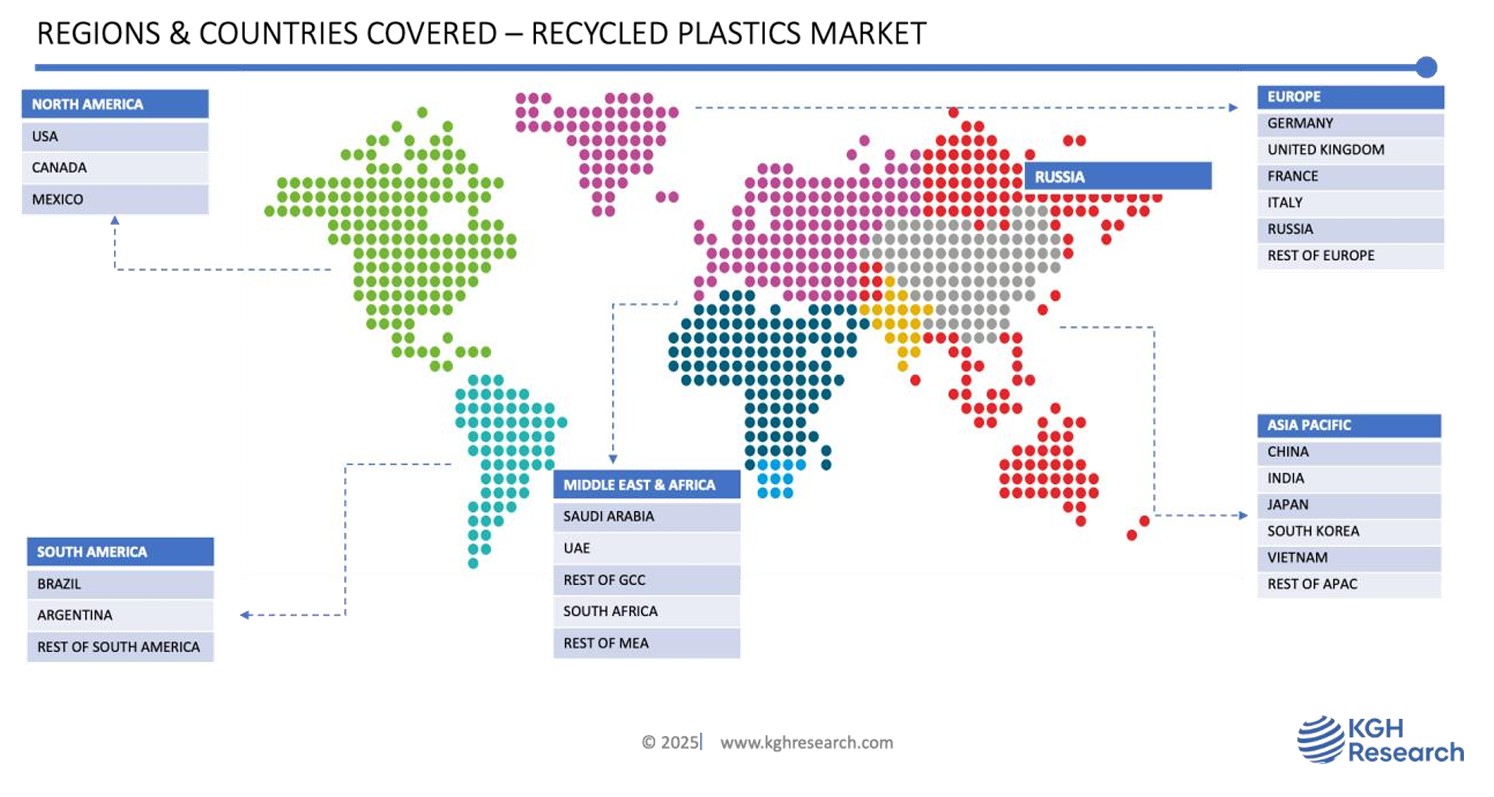

Regional: Market Insights

Asia pacific dominated the recycled plastics market in 2024, particularly China, India, and Southeast Asia, represents a high-growth countries and region due to rapid urbanization and increasing plastic consumption. China’s 2020 ban on imported plastic waste prompted domestic investment in advanced recycling technologies. However, challenges remain due to fragmented collection systems and limited regulatory enforcement.

Europe remains at the forefront of the global recycled plastics movement, with some of the highest recycling rates and stringent legislative frameworks promoting circularity. Germany, the Netherlands, and the Nordic countries are notable leaders, with Extended Producer Responsibility (EPR) schemes and deposit-refund systems that incentivize collection and processing. Moreover, EU mandates requiring a minimum percentage of recycled content in packaging are accelerating demand.

In Asia-Pacific, countries like Japan and South Korea have sophisticated recycling systems, while emerging economies like India and Vietnam are scaling up through public-private partnerships. The North American market, led by the U.S. and Canada, is seeing increasing investments from both brands and recyclers. The push for localized, closed-loop systems is helping overcome logistical bottlenecks and strengthen domestic recycling ecosystems. Middle East & Africa are emerging players, with governments exploring waste-to-value models amid rising environmental awareness.

Competition: RECYCLED PLASTICS MARKET

Competitive Landscape

The recycled plastics industry features a mix of global chemical players, regional recyclers, and specialized firms. Leading companies like Veolia, SUEZ, Borealis, and LyondellBasell are expanding capacity through mergers, joint ventures, and greenfield projects. Strategic collaborations with consumer brands such as Coca-Cola, Unilever, and Nestlé are common, aimed at securing supply and enhancing recyclate quality.

Major players include Veolia, Suez, Waste Management Inc., Republic Services, and Plastipak Holdings. These companies are leveraging M&A and joint ventures to expand geographic reach and diversify offerings. Technological partnerships with chemical companies like SABIC and Dow are creating hybrid recycling models.

Startups and mid-sized firms focused on chemical recycling—such as Carbios, Agilyx, and Loop Industries—are gaining traction through proprietary technologies and licensing models. Vertical integration strategies, wherein recyclers also handle sorting and collection, are gaining favour to ensure feedstock security and consistent quality. The competitive landscape is characterized by innovation, consolidation, and sustainability-led differentiation.

Companies are differentiating through innovations in sorting, AI-enabled material recovery facilities (MRFs), and traceability systems that certify recycled content. Certification and supply chain transparency are becoming key competitive levers.

Recent Developments:

- In 2024, Veolia announced the expansion of its mechanical recycling facility in Germany, boosting capacity by 30%.

- Eastman Chemical Company committed $1 billion to a chemical recycling plant in France, aiming for full circularity in PET streams by 2026.

- Unilever and PepsiCo jointly invested in closed-loop recycling systems for their packaging lines in Southeast Asia.

- In 2024, LyondellBasell announced a partnership with 23 Oaks Investments to develop one of Europe’s largest advanced recycling facilities for plastic waste.

- Loop Industries received FDA approval for its Infinite Loop™ depolymerization technology, enabling the production of food-grade PET from low-quality feedstock.

- SUEZ expanded its footprint in Southeast Asia with a joint venture in Indonesia, enhancing its capacity to recycle post-consumer flexible packaging.

- Veolia unveiled a new sorting and washing facility in the U.K., designed to process 50,000 tonnes of mixed plastics annually, aimed at meeting national circular economy goals.

| RECYCLED PLASTICS MARKET SNAPSHOT | |

| Market size in 2024 | USD 85 Billion |

| Market forecast in 2032 | USD 160 Billion |

| Compound Annual Growth Rate (2025-2032) | 8%+ |

| Historical Data (Years) | 2022-2024 |

| Forecast Data (Years) | 2025-2032 |

| Region Dominance (Regional Share %) | Asia Pacific: >50% Share |

| Country Dominance (Share %) | China: >30% Share |