Waterproofing Membrane (2022 - 2032)

WATERPROOFING MEMBRANES MARKET SIZE & SHARE BY MEMBRANE TYPE (LIQUID APPLIED AND SHEET MEMBRANES), BY PRODUCT TYPE (BITUMEN, PVC, TPO, ACRYLIC, POLYUREA, PU, AND OTHER PRODUCT TYPES), BY APPLICATION TYPE (ROOFING, FOUNDATION & BELOW GRADE, WATER-RETAINING STRUCTURES, INFRASTRUCTURE, AND OTHER APPLICATION TYPES), BY END-USE (RESIDENTIAL, NON-RESIDENTIAL, AND INFRASTRUCTURE), BY CONSTRUCTION (NEW CONSTRUCTION AND RENOVATION), AND BY REGION & COUNTRY–FORECAST TO 2032

| Report Code: C&M3003-1103 | Number of Pages: 500 | Report Format: PDF, EXCEL, PPT |

|---|---|---|

|

Trend Year: 2022 – 2024 |

Forecast Period: 2025 – 2032 |

Publish Date: JULY 2025 |

- Report Summary

-

Tables of Content

- Segmentation

- Methodology

- User License & Pricing

- Sample Copy

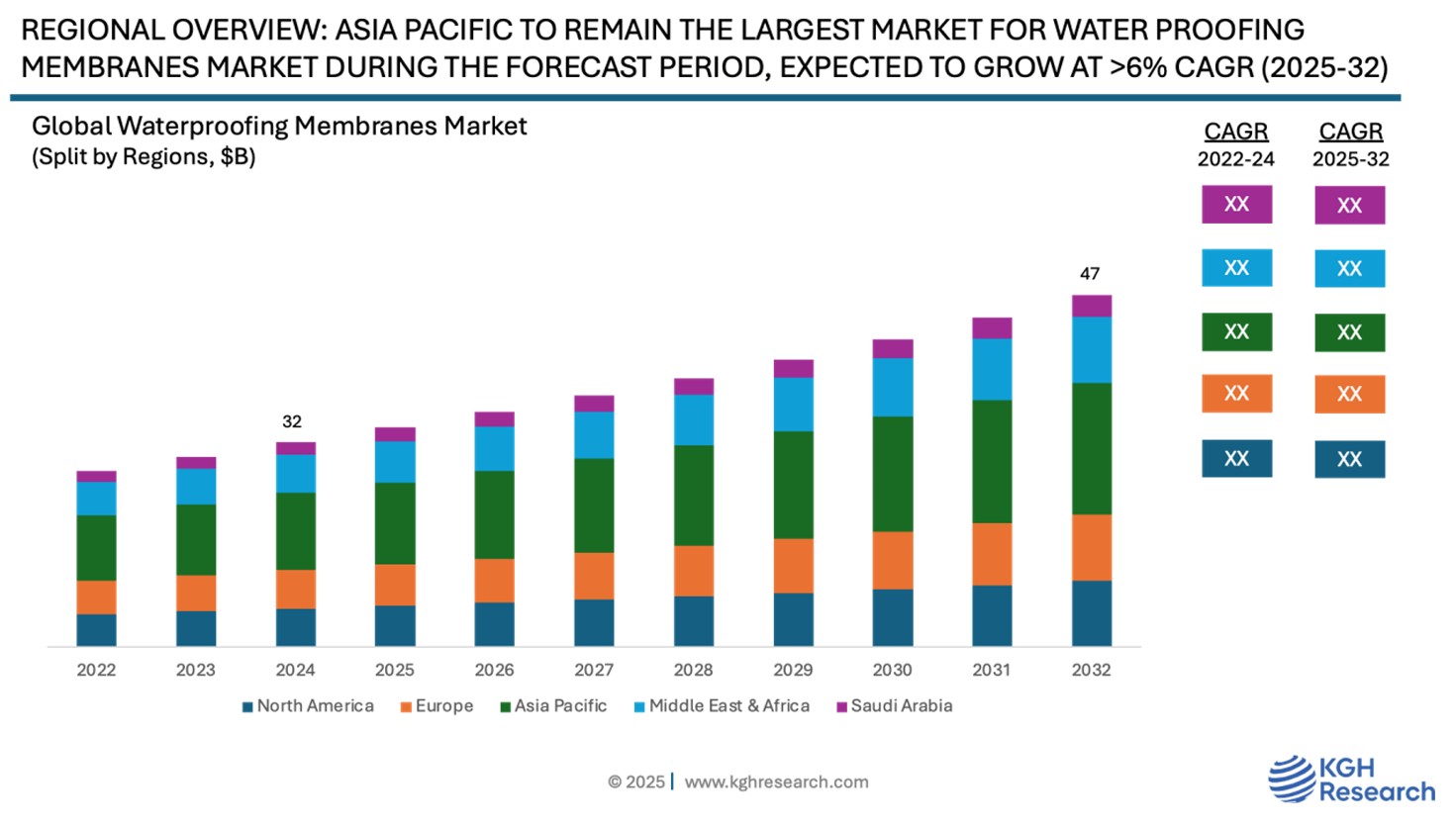

Market Overview: The global waterproofing membranes market was estimated at US $32 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 5.0% from 2025 to 2032 to reach US $47.5 billion by 2032. This growth is attributed to the ongoing urbanization trends, increasing adoption of sustainable waterproofing technologies, growing demand for energy efficient buildings, cost effective waterproofing solutions that offer improved durability and environmental resistance, coupled with sustained construction activity in key regions and countries, globally are the key drivers.

MARKET DYNAMIC

GROWTH DRIVERS:

- Growing Construction Activity

- Rapid Urbanization

- Increasing Renovation Activity

- Growth Driver 3

- Growth Driver 4

- Growth Driver 5

NEW GROWTH OPPORTUNITIES:

- Sustainable Waterproofing Technologies – Membranes with Recycled Content, Bio-Based Polymers, and Other Eco-Friendly Products

- Increasing Demand for Energy Efficient Buildings

- Growing Preference for Liquid Applied Membrane over Traditional Sheet Membrane

- Opportunity 4

- Opportunity 5

- Opportunity 6

MARKET RESTRAINTS:

- Skilled Labor Shortage

- Market Restraint 2

GROWTH HURDLES:

- Recessions or downturns could reduce construction activity, globally and thus the demand for liquid applied membranes

- Trade tensions, tariffs, and geopolitical instability may impact global supply chains, demand, production costs, and profitability.

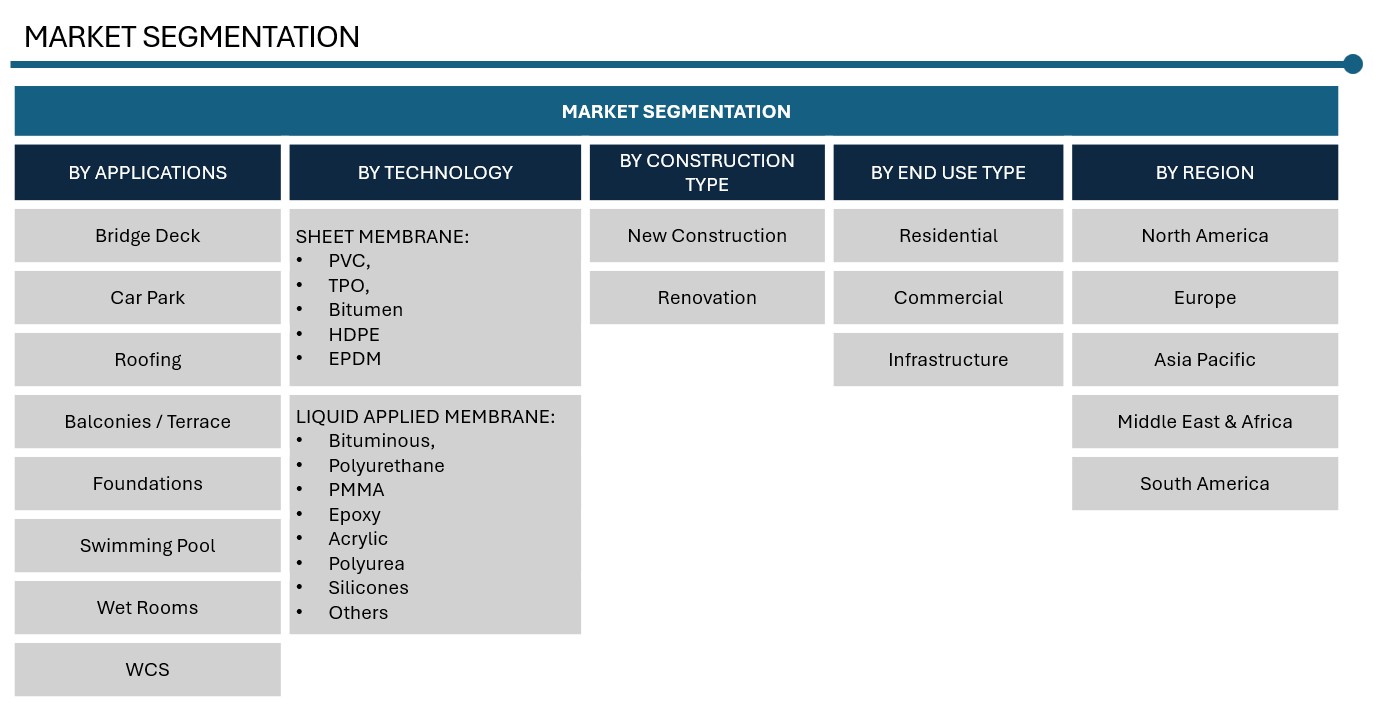

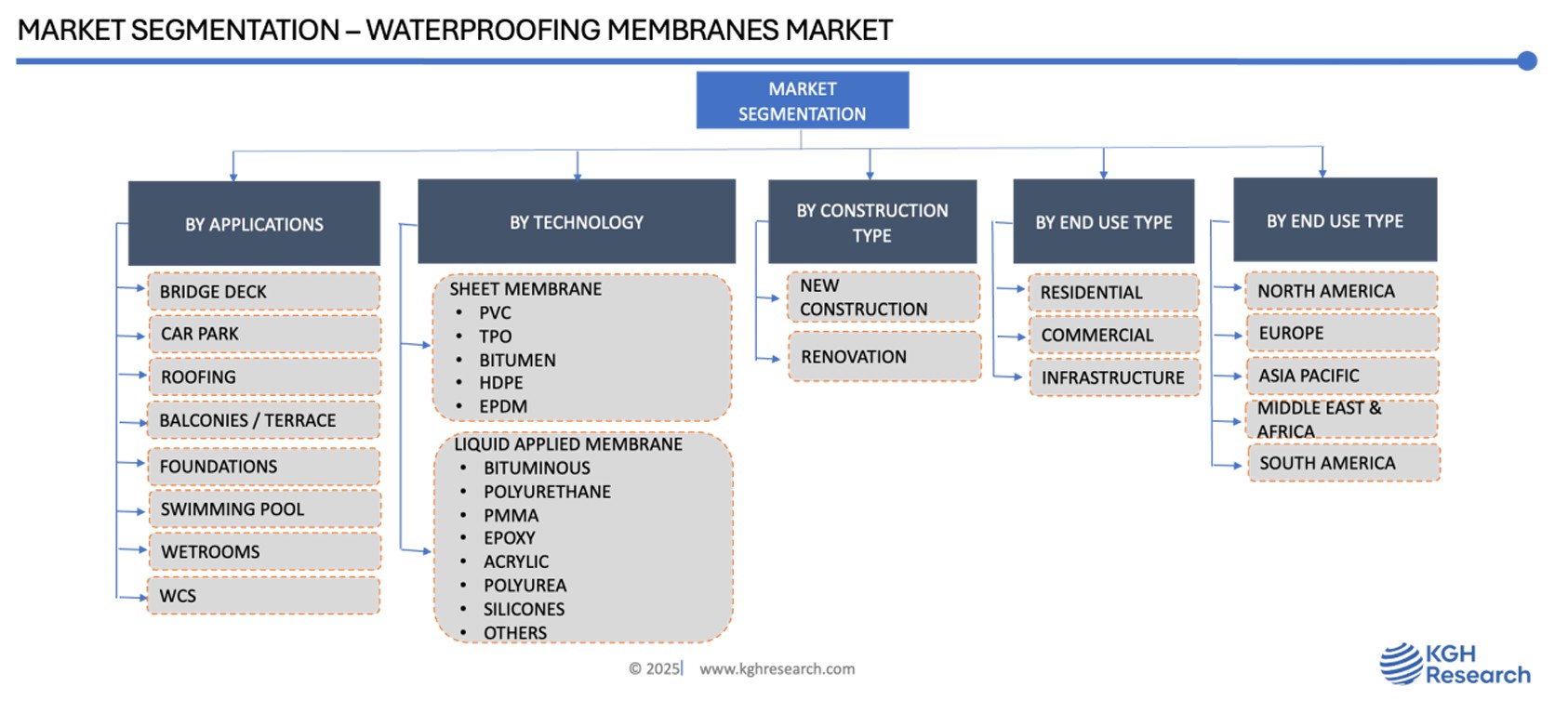

Membrane Type: Market Insights

The global waterproofing membrane market is categorized into sheet membranes and liquid-applied membranes, each serving distinct needs across the construction landscape. Sheet membranes are expected to retain their dominance through the forecast period, driven by their proven durability, long-term performance, and widespread use in commercial and infrastructure projects. Conversely, liquid-applied membranes are projected to be the fastest-growing segment, fuelled by their application flexibility and efficiency in covering complex surfaces. The continued advancement of both membrane types is closely tied to emerging sustainability standards and the rising demand for cool roofing technologies, reflecting the industry’s commitment to energy efficiency and environmental responsibility.

Application Type: Market Insights

Roofing dominates the waterproofing membranes market, accounted for more than 50% share of the market. Roofs play a critical role in protecting buildings from harsh weather conditions and water intrusion. This essential function coupled with the vast number of rooftops worldwide and their constant exposure to environmental stress drives steady, long-term demand for waterproofing membrane solutions for energy efficient buildings

Although roofing applications currently lead the waterproofing market, the foundation and below-grade segment is poised to have the fastest growth. These areas are particularly vulnerable, as water infiltration can severely compromise the structural integrity of foundations and below-grade walls, making advanced waterproofing systems increasingly vital in both new construction and renovation projects.

Product Type: Market Insights

The waterproofing membrane market is segmented by product type into bitumen, PVC, TPO, acrylic, polyurea, polyurethane, and others. Among sheet membranes, bitumen is expected to retain its dominant position throughout the forecast period, owing to its cost-efficiency, proven durability, and broad applicability across commercial and infrastructure projects. In the liquid-applied membrane segment, polyurethane is projected to be the fastest-growing product type, driven by its strong adhesion properties, versatility, and suitability for complex substrates.

As the industry increasingly prioritizes sustainable construction practices, product innovation is focusing on environmentally friendly, long-lasting, and cost-effective solutions. Membranes that align with green building standards and help reduce the total lifecycle cost of waterproofing systems are expected to gain competitive advantage in the evolving market landscape.

End-Use: Market Insights

The waterproofing membrane market is segmented into residential, non-residential (commercial), and infrastructure applications. The residential sector is projected to remain both the largest and fastest-growing end-use segment throughout the forecast period. This growth is fuelled by rising construction spending, a surge in housing demand, and increased activity in the home improvement and renovation space, particularly in urban and suburban areas.

The commercial segment is expected to continue playing a significant role in market expansion, driven by ongoing infrastructure investments and heightened demand for energy-efficient building solutions. Technologies such as cool roofing systems and reflective membranes are gaining traction in this sector, as building owners and developers seek to comply with sustainability standards and reduce operational energy costs across diverse geographies.

Construction Type: Market Insights

The waterproofing membrane market is segmented into new construction and renovation. While new construction continues to hold a significant share—driven by urbanization in emerging economies and large-scale development projects—renovation is projected to be the faster-growing segment during the forecast period.

This growth is fuelled by the global trend of aging infrastructure, particularly in developed markets, where a rising number of buildings and civil structures require restoration and waterproofing upgrades. Additionally, the increasing adoption of sustainable building practices and a surge in home improvement and repair projects are further accelerating demand for renovation-focused waterproofing solutions.

As governments and private sectors alike prioritize the maintenance and retrofitting of existing assets, the renovation segment is positioned as a key driver of market expansion moving forward.

Regional: Market Insights

The global construction industry and the players within are optimistic about 2025 due to a combination of factors such as widespread government infrastructure initiatives, the ongoing renewable energy revolution, increased capital investment in strategically important industries, and the resumption of post-COVID pipeline projects—presents significant opportunities for industry stakeholders.

However, geopolitical tensions, particularly the war in Ukraine, India Pakistan, introduction of US Trade Tariffs, have introduced considerable uncertainty, complicating the industry’s path to sustainable growth. Despite these challenges, the sector has shown resilience, navigating through headwinds with a focus on long-term recovery.

Looking ahead, a gradual recovery is anticipated starting in 2025, driven by the rebounding housing market and an increase in building permits for new homes. This positive shift is expected to have a favourable impact on the waterproofing membrane market, as growing demand for construction materials aligns with expanding infrastructure projects and residential development.

Asia-Pacific dominates the global waterproofing membranes market, accounting for more than 50% share by both value and volume wise market. This leadership is fuelled by rapid urbanization, robust infrastructure development, and stringent government waterproofing regulations across key countries like China, India, Japan, Thailand, Vietnam, and Indonesia. The region’s accelerating shift toward sustainable and high-performance waterproofing solutions further reinforces its commanding position in the industry.

North America is experiencing the most rapid growth in the waterproofing market. This surge is driven by increasing demand for energy-efficient roofing, stringent building regulations, and investments in renovation projects. Notably, the adoption of acrylic and polyurethane-based waterproofing solutions is on the rise, particularly in the U.S. and Canada, where durability and sustainability are major considerations.

Competition: Waterproofing Membrane Market

The global waterproofing membrane market is moderately fragmented with top five players, such as Oriental Yuhong, Sika AG, Carlisle Companies, Standard Industries (BMI Group and GAF Material Corporation), and Soprema Group collectively accounted for 30% to 35% share, followed by more than 200 players participating in the regional and domestic markets.

Mature markets—including North America, Europe, and China—are characterized by intense competition, with well-established companies continually battling for market share. In contrast, emerging regions such as Asia-Pacific (excluding China), the Middle East, and Latin America present robust growth potential, drawing in new players and heightening competitive dynamics.

Innovation remains a key differentiator, especially in the development of sustainable and high-performance materials. Industry leaders are prioritizing investments in eco-conscious technologies—such as recyclable and VOC-free membranes—to meet the rising demand from environmentally aware consumers.

In markets like Asia-Pacific, price sensitivity is a critical factor. To remain competitive and profitable, companies must strategically balance cost efficiency with product quality and innovation.

Carlisle Companies Inc. is a leading manufacturer of high-performance building products and waterproofing solutions, operating through two core business segments: Carlisle Construction Materials (CCM) and Carlisle Weatherproofing Technologies (CWT). The company maintains a strong market presence in North America, where it is recognized as a trusted provider of roofing systems for commercial buildings.

Through its CCM segment, Carlisle delivers single-ply roofing systems and related building envelope products for both commercial and residential applications. A strategic emphasis is placed on sheet membrane waterproofing, offering a comprehensive portfolio engineered for durability, high performance, and ease of installation.

Carlisle Construction Materials experienced notable revenue growth during the first nine months of 2024, driven primarily by a rebound in the non-residential construction sector. This growth was supported by inventory normalization and a significant increase in re-roofing activity, responding to previously pent-up market demand.

The company serves a diverse customer base, including contractors, architects, engineers, and building owners, reinforcing its position as a key partner across the building and construction value chain.

Oriental Yuhong is a global leader in waterproofing systems and building materials, with a diversified presence across the residential, commercial, and infrastructure construction sectors. Leveraging a comprehensive product portfolio and strong R&D capabilities, the company has earned a reputation as a trusted brand in over 100 countries.

Approximately 80% of Oriental Yuhong’s revenue is derived from its waterproofing materials business, highlighting its deep expertise and market leadership in this core segment.

As part of its international expansion strategy, Oriental Yuhong is establishing an integrated production, R&D, and logistics hub in Prairie View, Texas. Phase I, expected to be completed in 2025, will manufacture TPO waterproof membranes and include a North American R&D center, creating approximately 100 local jobs. This investment further reinforces the company’s commitment to the North American market.

In 2023, Oriental Yuhong entered a strategic collaboration with BASF to co-develop solar roofing membranes in response to the growing demand for rooftop solar solutions in China. The integration of BASF’s Tinuvin® and Chimassorb® stabilizers enhances the UV and thermal resistance of TPO membranes, significantly improving product durability, lifespan, and maintenance efficiency.

Oriental Yuhong’s sheet membrane solutions are engineered for critical waterproofing applications, including tunnels, underground structures, basements, reservoirs, and green roofs, providing reliable protection against water ingress in complex environments.

WATERPROOFING MEMBRANES MARKET PURVIEW | |

Market size in 2025 | USD 32 Billion |

Market forecast in 2032 | USD 47.5 Billion |

Compound Annual Growth Rate (2025-2032) | 5.0% |

Historical Data (Years) | 2022-2024 |

Forecast Data (Years) | 2025-2032 |

Region Dominance (Regional Share %) | Asia Pacific: >50% Share |

Country Dominance (Share %) | China: >30% Share |

Growth Driver | Growing Construction Activity and Rapid Urbanization |

Segments Covered | Application Type, Product Type, Construction Type, End Use Type, Installation Type, Product Grade Type, and by Region & Countries |

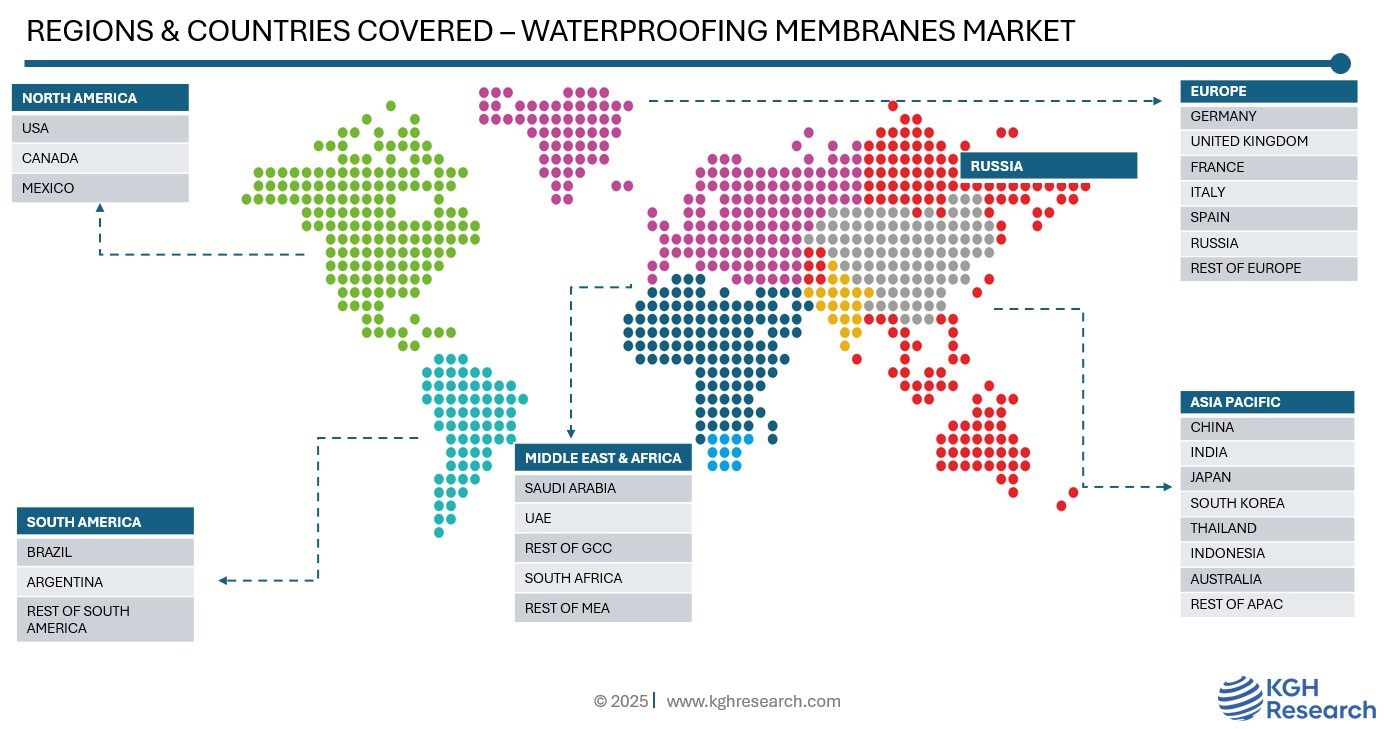

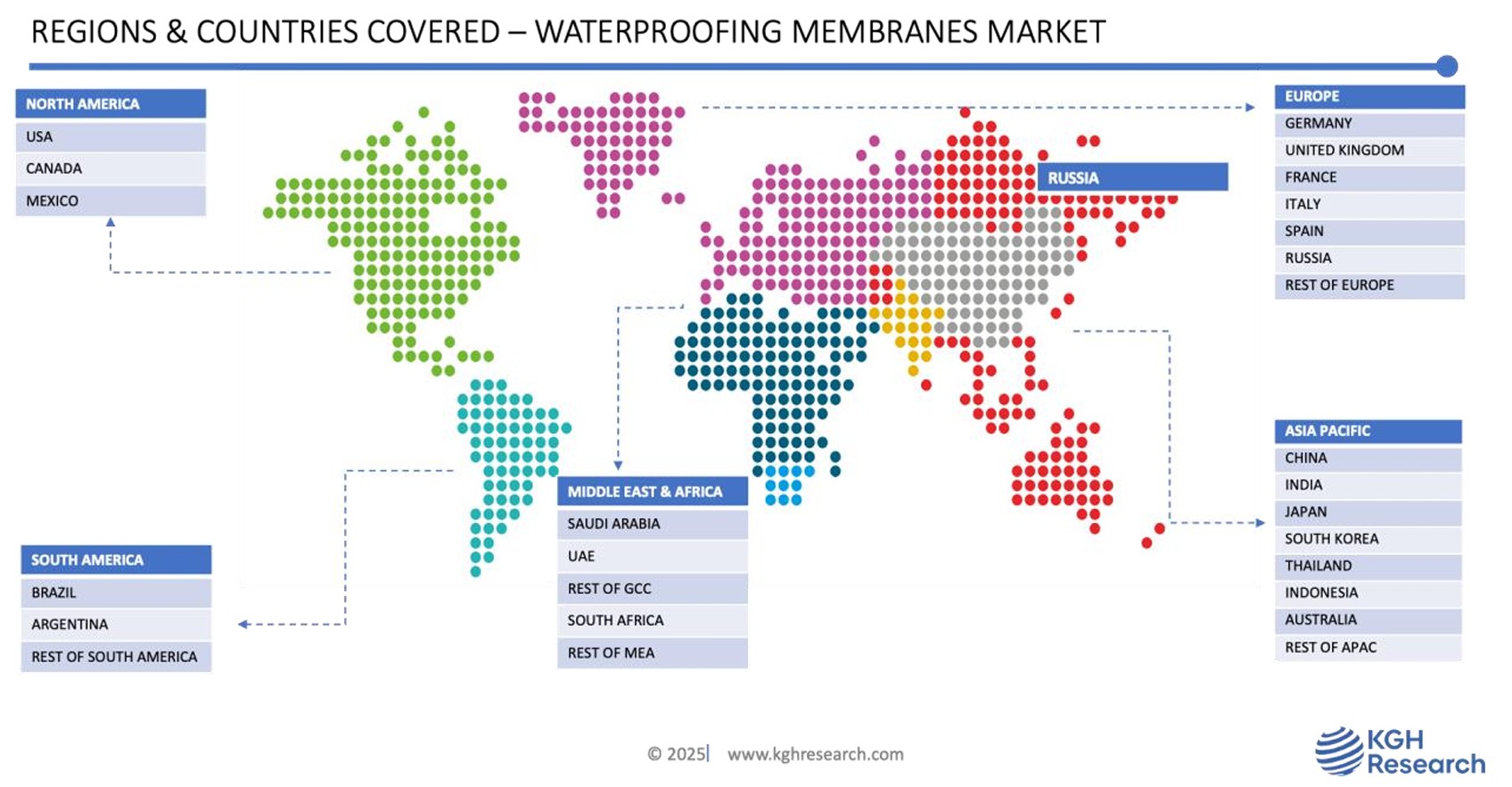

Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

Countries Covered | US, Canada, Mexico, The UK, Germany, Italy, France, Spain, Poland, Russia, Rest of the Europe, China, Thailand, Vietnam, Indonesia, India, Japan, South Korea, Australia, and Rest of APAC, UAE, South Africa, Brazil, Argentina, Saudi Arabia, Turkey, UAE, and Rest of the World |

Companies Profiled (30+) | Oriental Yuhong, Keshun Waterproof Technology, Sika AG, Soprema Group, BMI Group: Standard Industries, Fosroc: Saint Gobain, Mapei, Carlisle Companies, Firestone Building Products: Holcim, GAF Materials: Standard Industries, IKO Industries, Johns Manville, Bautech, Curacreta, IMPAC: Saint-Gobain Protexa,Vedacit, Viapol: RPM International, Saudi Bitumen Industries (SABIT), Alchimica, Awazel, Izomaks, Fatra, and Others |